Conclusion. We’re all-in on KATE at current levels. All along, we’ve pointed to a $70-$80 value. The stock is off 26% over the past month, due to sentiment concerns around 'the space' (KORS is off 27%), but our fundamental outlook has not changed one bit. The business remains very strong, we think that comps are accelerating into the double digits in 2Q, and we think that KATE’s margin guidance for this year will prove conservative. Ultimately we think that numbers this year are 15% too low – a delta that widens to 35% next year, and to 50%+ by 2018 when we think KATE has $3.00 in earnings power. Using decelerating multiples as growth accelerates and the P&L matures gets us 55% upside in a year and a 2-3-bagger by 2018. If we see the typical 'peak multiple on peak earnings' that retail knows so well, then a $100+ stock by year 3 is not out of the question.

To put this stock move in context, KORS – due to its recent implosion – is down 27% for the past month. While we think KORS is beyond cheap and has meaningful downside support here, the fact of the matter is that whether you’re bullish or bearish on KORS – the stock move can at least be explained away by the headlines. But with KATE – that’s simply not the case. As a sidenote, we turned positive on KORS on this week's implosion, but that was not a typical call for us. We think that KATE offers far better upside, has greater margin of error, and is a much more defendable growth story, by far.

Quick Sentiment Check

Our strong sense on the sentiment is that if you were concerned about ‘the handbag space’ (a definition that we still think is ridiculous) and wanted to short it, you had the following options…

a) 2012-14: There was pretty much one name you had for the past 3-years – Coach. The brand was beyond full market saturation, and had 30% margins that had nowhere to go but down without significant risk to the top line. But that name largely became tough to short by the fall of 2014, after it dropped by 55% at the same time the market went up by 45% (yes, 100% relative underperformance).

b) 2014-2015: About the same time Coach stopped going down, KORS became the go-to name to short. It has a fully penetrated business in the US, and Coach-like margins of 29%. Since that time (roughly a year ago) the stock traded off by 50% and underperformed the market by 60%. Then – even before this week’s blow up – the general sense we got from the investment community was that it was getting tougher to short.

c) 2015: With Coach and Kors serving as the poster twins for saturation and underperformance, people naturally look add a triplet to the group. The only other public company in this ‘space’ is KATE, which admittedly looks wildly expensive on current year earnings. As such – for better or worse -- it has turned into the go-to ‘high multiple in a troubled space’ short and source of funds in retail. The unfavorable tape might help the short case for the time being, but the supporting fundamental premises simply make no sense. Here are some considerations…

Why KATE ≠ KORS ≠ COH

Let’s get COH out of the way. This company is good at one thing. Creating handbags for one consumer – a 30-60 (really 40-60) year-old US consumer that shops in department stores and outlet malls. That’s all, nothing else. It has 13% share of the US handbag market. No apparel, no meaningful accessories, little presence with men (manpurses are rarely a good investment hook anyway) and consistent failure in bridging to an International audience. This coach is being drawn by a one-trick pony.

KORS is a different animal. KORS has an $8bn retail footprint versus COH at $5.2bn despite having 300bp lower share of the handbag market than COH (10% share vs COH at 13%). That’s due to its presence in accessories, men, and overseas (it has nearly a $1bn business alone in Europe, and that should at least double from here). Given its diversity, we’d argue that KORS has more in common with a brand like Ralph Lauren than COH. The only thing the two have in common is an EBIT margin that recently peaked at 30%, and is now trending in the high 20s.

KATE is also a different animal (but much smaller, and not on the endangered species list). Did anyone ever consider that one of the reasons why the incumbents are stalling out is because KATE spade is eating their lunch? Think about it this way… COH is at 13% share, KORS is 10%, and KATE is less than 3%. KATE’s (annual) brand footprint is sitting just under $1.5bn – that’s 25% less than KORS ($8bn) generates in a single quarter. Kate is even 20% smaller than Tory Burch, which isn’t (yet) public. Like KORS, KATE sells in multiple categories, with handbags accounting for about 60% of sales, apparel at 15%, footwear at 10%, accessories/other at 15%. The company also has several licenses kicking in this year, including watches (Fossil) that should boost its high-margin accessories business. KATE, unlike COH, has been accepted by consumers in Europe and across Asia – which remains a key part of the growth story.

Aside from licenses, which will help KATE meaningfully effective 2H, don’t underestimate the importance of the maturation curve for its stores. So many people think that KATE’s store base is as old as the brand is. Not so. The brand hit the mainstream over a decade ago, but it really did not start to grow at retail in earnest until about 3-years ago. That’s pretty critical from where we sit because from a profitability standpoint, these stores tend to hit their stride in years 3-4. Looked at a different way, 80% of KATE’s stores are 4-years old or younger, and a whopping 44% are less than 2 years old. This is seriously bullish for the company’s margin equation.

The point here is that KATE is absolutely NOT either of its perceived competitors. Financially, the closest comp is probably Tory Burch. The same reason why Tory will likely go public is that same reason why KATE should be bought today – it is just hitting its stride on the top line, which will accrue disproportionately to margins.

Let’s be clear about something, our estimate of $3.00 in EPS in 2018 is NOT assuming KORS or COH-like margins. It’s fair to say that both of those companies have shown us the perils of over-earning in this (or any) segment of retail. We’re simply assuming that margins at KATE get to 19% -- a good healthy level that should allow the company to continually invest to drive top line growth.

So What’s It Worth?

Today, 41x earnings and 15x EBITDA might seem very aggressive. But consider the earnings ramp. We’re looking at a CAGR over the next three years of about 70% for both earnings and cash flow. If we hold the cash flow multiple at 15x for the next year, which we think is fair as margins head higher and KATE catches estimate revisions and upgrades, then we’re looking at a $38 stock, or a 55% return in 12 months. Then we’ll reduce the multiple by 2 points per year, as the brand gets more mature, which gets us to $50 and then $65 in year 2 and 3 (vs $25 today). All that said, we’ve almost never seen a smooth multiple transition like that in retail. A typical pattern would be a higher/peak multiple on accelerating cash flow. That’s when we start pushing a $100 stock. That’s not our call today, but it’s not out of the realm of possibility.

Flash Sales:

- On the flash sale front (meaningful bc the company is trying to wean off of them, but the absence negatively impacts comps), the company ran 2 flash sales and one semi-annual sales event during 2Q14. 2Q15 to date, KATE has run one Friends and Family event (that fell in 1Q14 last year due to the late April Easter in 2014) and one flash sale. The company already indicated that it would repeat the semi-annual event at the tail end of the quarter, so there is a chance we see the elimination of one Flash Sale during the quarter. That should be more than offset by the addition of Friends in Family in the quarter.

e-commerce

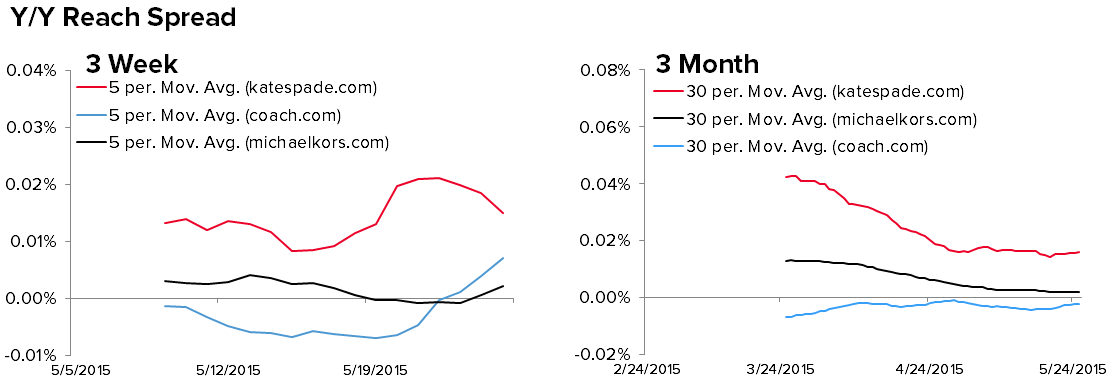

- Trends here matter a lot for KATE. Consider this…KORS generates 5% of its revenue online. Coach is sitting at 11%. KATE is just north of 20% -- one of the highest ratios out there for any retailer. #healthy balance

- When we look at recent trends for each of the brands in question (the charts measure each brand versus a year ago), KATE’s numbers are unquestionably higher than KORS and COH. The growth is lower than we saw earlier this year – but that is expected given reduced promotional activity. Overall, the trends look very healthy to us.

Margins:

- On the Gross Margin line, Kate Spade Saturday alone accounted for 240bps of the 315bps of dilution on the Gross Margin line (about $6.5mm) in 2Q14. The company hasn’t addressed this benefit in its guidance, either for the fiscal year or the upcoming quarter and it is not reflected in current consensus numbers. For the quarter we assume that the company gets back 200bps of the dilution which is offset by Fx pressure and the shift of the Friends and family sale into the quarter.

- We’re modeling 250bps of SG&A deleverage as the company continues to leverage sales growth on the fixed G&A costs and international profitability improves.