This note was originally published at 8am on May 01, 2015 for Hedgeye subscribers.

“What I do have are a very particular set of skills.”

-Liam Neeson, Taken

Officially, the Taken film franchise is a trilogy. The 1st installment was a deservedly acclaimed action-suspense juggernaut with Liam Neeson launching what has been affectionately dubbed the “geri-action” star genre.

Unofficially, there are probably more like 6-10 Taken movies. The high concept mystery-action airplane drama, Non-Stop, was essentially Taken on a plane. The survival thriller The Grey was basically Taken in the woods, and the 2011 psycho-drama Unknown was more or less Taken with amnesia. I’m sure there are others.

The industry, I suppose, is simply supplying to the emergent demand and Neeson, after decades in the business, is simply capitalizing on an unlikely late career renaissance.

Back to the Global Macro Grind...

- Fed is overoptimistic on growth forecast à dots get pushed out

- Domestic and global growth (& inflation) disappoint à yields = lower for longer

- 1st qtr GDP shows residual seasonality à balance of year is better but full year shows we’re a 2% +/- economy.

- The U.S. decouples à ….until it doesn’t

If you feel like you've seen this Macro movie before, you’re not mis-Taken.

A fascinating and sometimes confounding aspect of being a living participant in a Keynesian Eco Carnivale is that, at times, it’s difficult to tell which way is up.

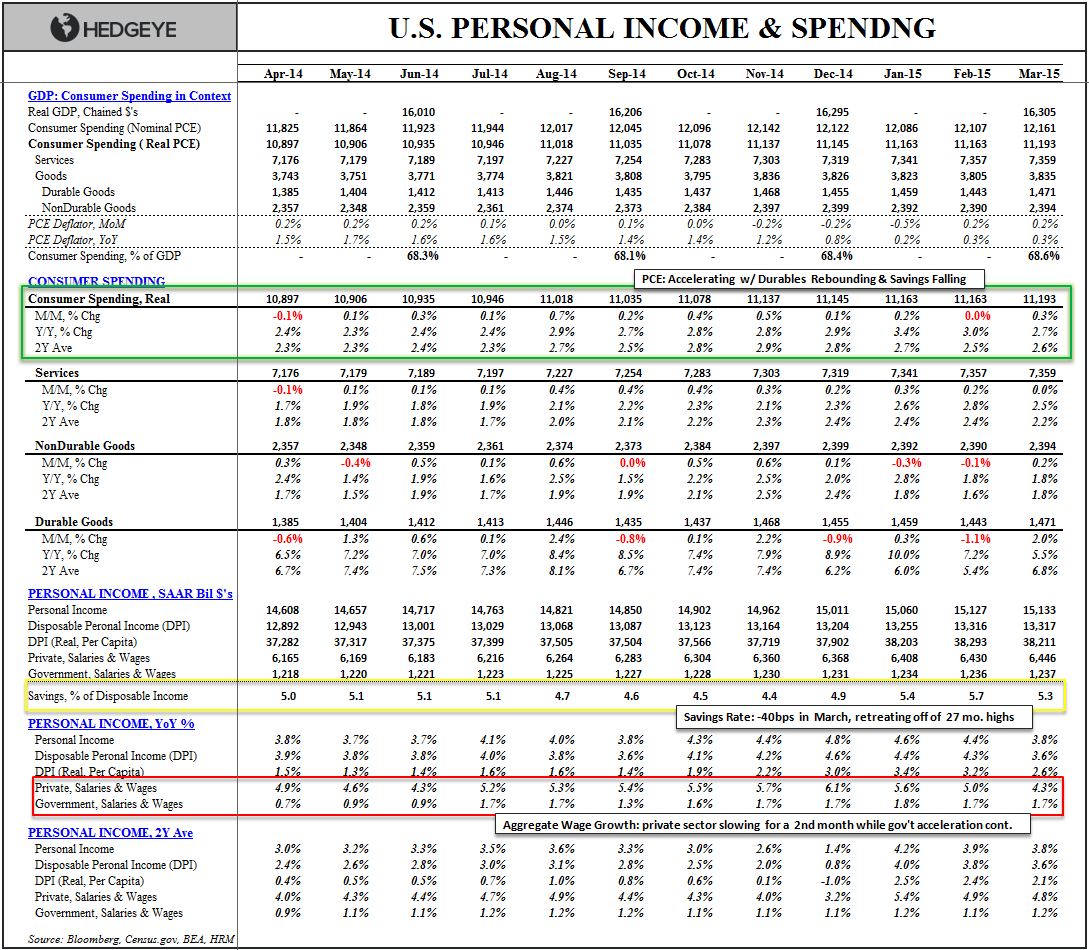

In the Chart of the Day below, we annotate the latest household Income and Spending numbers for March released yesterday.

Generally, our Macro-for-Dummies/Lazy’s color-coding protocol follows a green = good, red = bad convention. Over the last couple quarters, however, I’ve struggled with what colors to use to characterize the existent income and spending dynamics.

Income ↑, Savings ↑, Spending ↓: In recent months, aggregate wage and disposable income growth has been accelerating alongside a commensurate rise in the savings rate to multi-year highs. The net of those dynamics has been further middling in aggregate consumption. In other words, while the capacity for consumption growth has improved alongside accelerating income, the ongoing rise in the savings rate has muted the translation to actual household spending growth.

Is this good or bad?

In a Keynesian framework, total spending is paramount and the dearth of demand should be construed as a negative immediate-term development. At the same time, however, it’s difficult to characterize accelerating income growth, a rising savings rate and moderate credit growth alongside increased investment as a fundamentally negative development for the populous balance sheet or the prospective durability of the expansion.

How did spending and Income close out 1Q?

Income ↓, Savings ↓, Spending ↑: The savings rate saw its largest sequential drop in a year in March and spending grew at a premium to income for the first time in 8-months while aggregate disposable and salary and wage income growth moderated for a 2nd month. Inflation-adjusted disposable income actually declined -0.2% on the month while, on the spending side, a strong rebound in durables consumption growth buttressed headline spending against sequential softness in Services consumption and a modest gain in non-durables.

There a few takeaways from the March numbers:

- Income: the sequential deceleration in aggregate income growth wasn’t particularly surprising given the soft NFP number for March and the large contribution to personal income from dividends recorded in February.

- The Thaw: the increase in spending and decline in savings lends (some) support to the view that the pace of domestic consumerism was stymied by unusually severe weather. The re-acceleration in auto sales in March and marked rebound in housing activity in March/April are also supportive of the deferred consumption narrative.

- Inflation: Core PCE inflation – the Fed’s preferred measure – accelerated modestly for a second month to +1.34% YoY in March. The core PCE and CPI figures along with similar readings out of the billion prices index, a moderation in the $USD’s ascent, the counter-trend move in oil prices and the ramp in breakevens/inflation expectations, should buoy the Fed’s rhetorical expectation for stable to improving price trends. Also, the ECI data (note: the ECI data is a more comprehensive measure of employee compensation as it includes both wage income and benefits) for 1Q released yesterday showed employing compensation rising +0.7% in 1Q and growing at the fastest pace in the current cycle. This is a mixed bag. For the Fed it augers (eventual) upside for consumer prices. For many businesses, the prospect of accelerating inflation in the largest input cost in the face of a flat to decelerating topline probably does not augur upside in capex or profitability.

- The Bounce: Residual seasonality, weather, port-shutdowns, strong dollar, flagging export demand, and the cratering in energy sector investment have all been trotted out – with some justification – as a conspiratory cocktail of collective drag on economic activity in 1Q. The traversing or moderation in each of those factors – and the now easy comp – should support a rebound in reported growth in 2Q. Will the rebound be similar in magnitude to that observed in 2014? Perhaps, but the early evidence isn’t particularly inspiring.

What do you do with these divergent macro vectors from an investment standpoint? Probably not a whole lot until we get the employment river card next Friday.

While we like to think we have a “particular set of skills”, the expectation for 20-20 macro forecasting vision is quixotic. As Keith highlighted yesterday, sometimes the cacophony of macro crosscurrents breeds confusion more than high probability opportunity….and “going to cash beats confusion.”

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.86-2.08%

SPX 2075-2106

VIX 13.03-14.99

USD 94.32-97.46

Oil (WTI) 53.38-59.93

Gold 1169-1204

Sunny & 70’s on tap for the Northeast. Enjoy the weekend.

Christian B. Drake

U.S. Macro Analyst

Click image to enlarge.