This note was originally published at 8am on April 23, 2015 for Hedgeye subscribers.

“The fact is our starting point.”

-Aristotle

I’m not a big Aristotle fan, but I like some of his simpler quotes. In Global Macro risk management (and in life), I like to boil things down as simply as I can, or I don’t feel like I understand them well enough.

The aforementioned quote is one that Ed Hess used to introduce Chapter 7 of Learn or Die, “Critical Thinking Tools.” In both the chapter and the book, Hess leans on Dr. Gary Klein’s RPD (Recognition-Primed Decision) Model.

“Klein has developed three tools that can increase the probability that we’ll be able to “see” and process new or disconfirming data and mitigate our cognitive blindness and dissonance (pg 75).” Being a data driven #process guy, I’m all for trying that.

Back to the Global Macro Grind…

Our starting point is last price. I know that sounds simple. It should. Our best starting point for evaluating new, confirming, and/or disconfirming “data” is to get Mr. Macro Market’s cumulative opinion on whatever that data is perceived to be.

“Klein found that people in high-velocity environments, where speed of decision making is important, generally don’t take the time to generate alternatives and then weigh the pros and cons of each (or engage in a probability evaluation). Instead, they engage in fast pattern matching.” (pg 76)

Sound familiar? We’ve all done this at some point in our careers. Some people in this profession probably still do it in trying to process every macro headline, every day!

“So”, try not to do that.

Let’s start this morning with some fast pattern matching (and see if any of it matches):

- Both US Existing Home Sales and weekly US mortgage demand data surprise to the upside (again)

- SP500 reverses its early morning losses to close within 0.5% of her all-time highs

- Bond Bears claim Housing data is “too good”, so the Fed needs to raise rates (rates rise, bonds fall)

Throw a little extra headline sauce in there like “Bill Gross Says Short Of A Lifetime” (yesterday he was talking his book to all mainstream media outlets who would listen) on German Bunds, and you saw the worst down day for the G-10 Bonds, in a month.

But, if you’re not flash crashing your P&L with every tick of the New Tape (Twitter)… and you take a step back (breathe)… does that sequence of pattern matching with very immediate-term price action make sense?

Do people who shorted Bunds and Bonds on the lows yesterday actually think that:

A) The Fed is going to change their statement on April 29th due to the Existing Home Sales print and/or

B) Thwart one of the few things they can currently take political credit for (#HousingAccelerating) by raising rates?

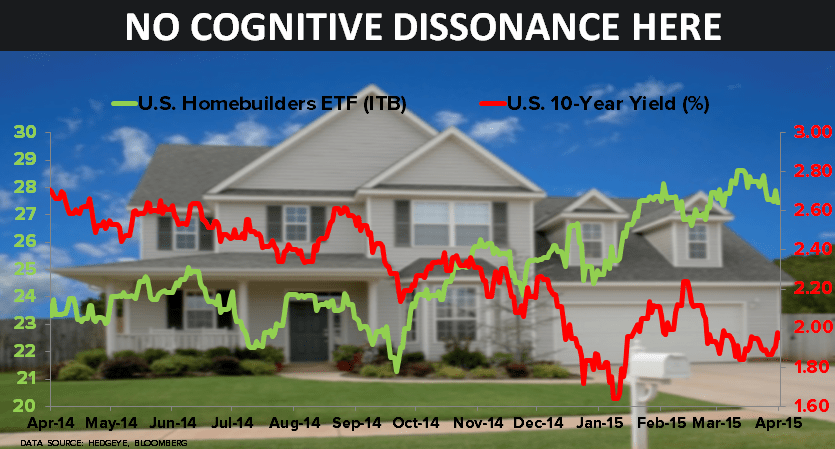

I remain bullish on both Long-Duration Bonds (TLT, EDV, MUB, etc.) and Housing (ITB, DHI, MTG, etc.), so you can argue that I am dead wrong on this due to my own cognitive blindness. But that’s what makes a market.

Another thread of short-term pattern-matching that was bearish for sovereign bonds yesterday goes something like this:

- “The European economy is booming”

- German economic growth will force Draghi to back off QE

- European Bond Yields can only rise now, as a result

Oh, then there’s this stuff called the global (not local) economic data this morning:

- Chinese and Japanese PMIs for APR slow (again) to 49.2 and 49.7, respecitvely

- Germany’s PMI slowed (for the 1st time in months) to 51.9 APR vs. 52.8 last

- France’s PMI (which never accelerated to begin with) slowed, again, to 48.4 in APR vs. 48.8 last

In other words, the Italian (Draghi) needs to provide the French with moarrr cowbell!

“In psychology, Cognitive Dissonance is the mental stress or discomfort experienced by an individual who holds two or more contradictory beliefs, ideas, or values, at the same time…” –Wikipedia

The fact is that Bond Bears need one very simple thing to be as right as we were on US #RatesRising in 2013 – and that’s real economic #GrowthAccelerating. Meanwhile (not to be confused with centrally planned stock market ramps), Global Growth continues to slow.

We believe that, with neither growth nor inflation accelerating (intermediate-term TREND), the Long Bond Bears will continue to lose money. Our starting point on that Macro Theme is what Mr. Macro Market has been discounting now, for 15 months.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.84-1.99%

SPX 2090-2117

RUT 1252-1275

EUR/USD 1.05-1.08

Oil (WTI) 50.04-57.78

Gold 1181-1208

Best of luck out there today – Go Rangers!

KM

Keith R. McCullough

Chief Executive Officer