The VIX was up 9.7% yesterday and moved through and closed above its immediate term TRADE line of 24.13, which implies a break out on a short term duration and signals a heightened volatility environment on the margin.

On Monday, the S&P 500 closed at 1,066, down 1.2% and 3.2% over the past week. Yesterday’s down day for the S&P 500 was on big volume which is bearish and notable since most major down days we have seen in the past three months have been on lower volume.

The tight correlation between the US dollar appeared to be the catalyst behind the reversal in the S&P 500 from the positive open, as the dollar index was down on the day.

The recovery trade was put into question as Financials, Materials and Energy were the worst performing sectors. According to StreetAccount, there were reports that Senate leaders are negotiating to gradually phase out an $8K tax credit for first-time homebuyers; the XHB declined 1.5% on the day.

Today we are waking up to the news that more countries are increasingly pulling back stimulus measures. Specifically, Norway is likely to raise its interest rate by 25 bps tomorrow and India will begin its exit from monetary stimulus measures. U.S. policy makers continue to lag their global brethren in the easing of stimulus, but can they be far behind?

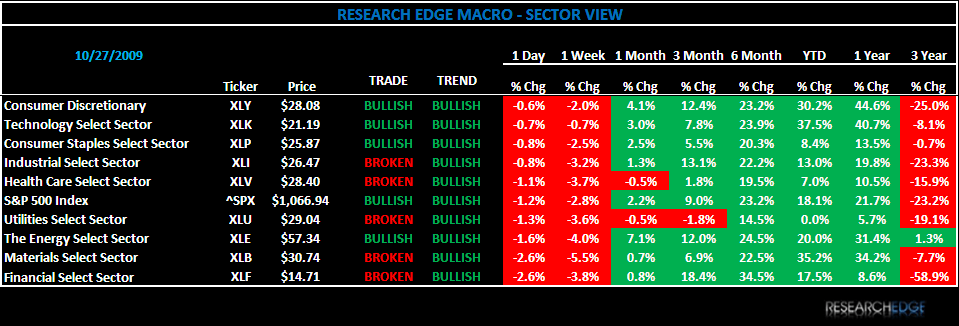

Yesterday, five sectors outperformed the S&P 500 and every sector was down on the day. For the second day in a row, the three best performing sectors were Technology (XLK), Consumer Discretionary (XLY) and Consumer Staples (XLP), while Energy (XLE), Financials (XLF) and Materials (XLB) were the bottom three.

Consumer discretionary was the best performing sector on Friday. Again, the breadth of the outperformance was not particularly impressive, as the bulk of the outperformance was again driven by RSH and AMZN. Media and housing related names were the biggest underperformers in the index.

The Materials and Financials were the two worst performing sectors yesterday. The Materials (XLB) fell more than 2% for a second straight day on Monday, as the dollar rallied for the third straight day. Within the XLF, the decline in the regional banks continued yesterday, and have now fallen four out of five trading days.

Today, the set up for the S&P 500 is: TRADE (1,066) and TREND is positive (1,013). The Research Edge quantitative models have 9 of 9 sectors in the S&P 500 positive on TREND and 4 of 9 sectors are positive from the TRADE duration. The only sectors positive on both durations are Energy, Technology, Consumer Discretionary and Consumer Staples.

The Research Edge Quant models have 2% upside and 0.5% downside in the S&P 500. At the time of writing the major market futures are flat.

The Research Edge MACRO Team.