Recent Notes

04/27/15 Monday Mashup

04/27/15 PNRA: Thoughts into the Print (1Q15)

04/28/15 DFRG: Short on Strength

04/29/15 PNRA: Unconvincing, But That’s Okay

04/30/15 Casual Dining Shorts?

05/01/15 YUM: Attracting the Attention it Deserves

Events This Week

Monday, May 4

- MCD Turnaround Plan 11:00am EST

- BBRG earnings call 4:30pm EST

- CHUY earnings call 4:30pm EST

- DENN earnings call 4:30pm EST

- IRG earnings call 4:30pm EST

- TXRH earnings call 5:00pm EST

Tuesday, May 5

- TAST earnings call 8:30am EST

- BLMN earnings call 9:00am EST

- NDLS earnings call 4:30pm EST

- KONA earnings call 5:00pm EST

- PBPB earnings call 5:00pm EST

- BBRG annual general meeting

- DAVE annual general meeting

- Robert W. Baird Growth Stock Conference: HABT, ZOES, CMG, BWLD, DNKN, IRG, KKD

Wednesday, May 6

- DAVE earnings call 8:00am EST

- WEN earnings call 9:00am EST

- PZZA earnings call 10:00am EST

- FRSH earnings call 5:00pm EST

- NDLS annual general meeting

- Robert W. Bair Growth Stock Conference: CHUY, PBPB

Thursday, May 7

- BAGR earnings call 4:30pm EST

- JMBA earnings call 5:00pm EST

- BWLD annual general meeting

Recent News Flow

Monday, April 27

- CMG became the first national restaurant company to use only non-GMO ingredients.

- WEN appointed Kurt Kane to the newly created position of Chief Concept Officer. Mr. Kane, who most recently served as Global Chief Marketing and Food Innovation Officer at Pizza Hut, will be responsible for all of North America marketing and innovation efforts.

Tuesday, April 28

- JMBA announced the sale of 21 stores to existing franchise partners as its refranchising effort continues to accelerate well ahead of schedule. JMBA is on track to close Phase II of its refranchising efforts by the end of the calendar year, with the ultimate goal of moving the franchise to company model to 90/10%.

Wednesday, April 29

- BOBE announced the pending closure of 20 underperforming restaurants over the next 12 months. The company estimates net proceeds will range between $15-17 million and estimate the sale will result in a $2.5-3.5 million annual improvement in operating income. It will incur $4.7-5.2 million of pre-tax charges related to the sale primarily during 4QF15, approximately $2.1 million of which is expected to be non-cash.

- PZZA announced a quarterly dividend of $0.14 payable on May 22, 2015 to shareholders of record on May 11, 2015.

Thursday, April 30

- DIN appointed Darren Rebelez as president of IHOP. Mr. Rebelez most recently served as COO of 7-Eleven.

- WEN is teaming up with Honest Tea to bring certified organic green tea to its restaurants nationwide.

Friday, May 1

- CMG upgraded to outperform at BMO Capital with a $760 PT.

- YUM Third Point announces a significant stake in YUM.

- PBPB promoted Julie Younglove-Webb to Senior VP of Operations. Ms. Younglove-Webb joined Potbelly back in 2008 as a General Manager and most recently served as Central Zone Vice President, a role in which she oversaw 250 shops.

- PZZA announced that Mr. Philip Guariscio did not stand for re-election to the Company’s Board of Directors at the 2015 Annual Meeting given he had reached the age of retirement.

Commodities

Sector Performance

The SPX (-0.44%) outperformed the XLY (-1.65%) last week. Casual dining stocks, in aggregate, underperformed the XLY, while quick service stocks outperformed.

Quantitative Setup

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

Casual Dining Restaurants

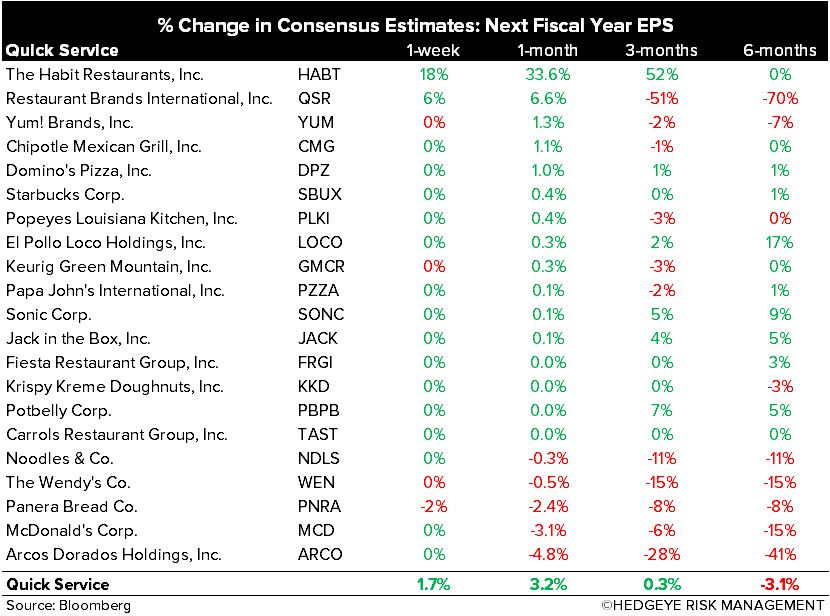

Quick Service Restaurants