Panera delivered a sub-par print after the close yesterday and held a mediocre earnings call this morning. Management commentary wasn’t quite what we were looking for, but that’s okay. If anything, this strengthens the case for further change within the company. We continue to recommend buying the stock on down days.

Soft Headline Numbers

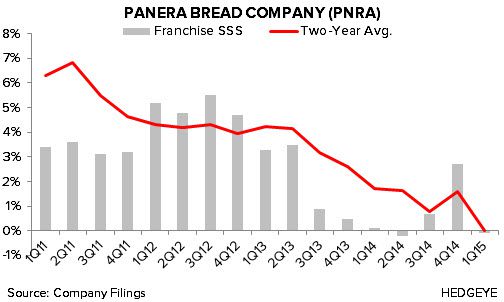

System-wide, company, and franchise same-store sales of +0.7%, +1.5%, and -0.1% fell well short of consensus estimates of +2.4%, +2.6%, and +2.0%, respectively. The lack of flow through was significant, as operating margin declined 180 bps (exclusive of the one-time refranchising charge). Labor was the most significant driver of the decline, as structurally higher wage rates and the investment of additional labor hours associated with the startup of Panera 2.0 across select locations weighed down margins. Food and paper inflation added notable pressure in the quarter as well. As a result, 1Q15 EPS of $1.41 fell short of the $1.43 consensus estimate. Despite the miss, management maintained full-year EPS guidance of flat to down mid-to-high single digits versus the prior year.

Management Could’ve Done More

We believe management could have said more on the call to convince investors that the strategic initiatives they are taking are the right ones. The general tone of the call was rather unconvincing as management delivered a trust us story as opposed to laying out a clear, concise strategic roadmap. While we do believe the investments the company is making will benefit the brand over the longer-term, we question to what extent they are prudently allocating their capital. We also believe there are a number of initiatives that management can undertake in order to create shareholder value. To review, Panera could:

- Sell off non-core assets

- Slowdown the rollout of Panera 2.0 and begin molding a concept of the future

- Slow unit growth and cut capital spending

- Cut excessive G&A spending

- Aggressively refranchise stores

Management offered up very little on these fronts, but we are in the early innings of the story here. So while they could’ve said more on the call, it is plausible to consider that they are just beginning to vet these potential value enhancing initiatives.

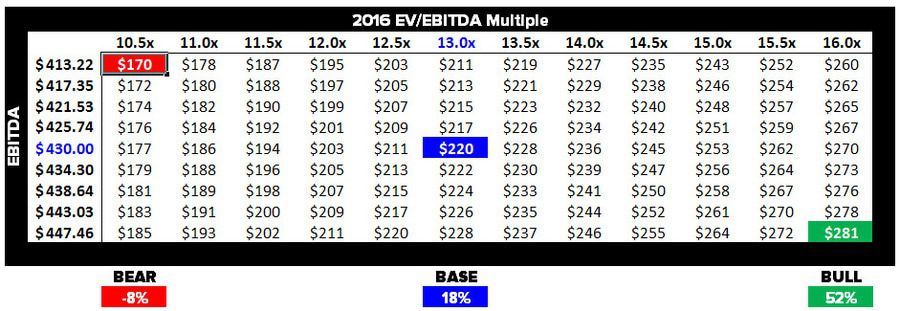

Asymmetric Risk/Reward Setup

We continue to believe PNRA represents an asymmetric risk/reward setup, with our conservative base case scenario calling for 18% upside over the next 1-2 years. To contrast, our bear case calls for -8% downside. On a relative basis, the stock is among the cheapest in the quick service/fast casual category trading at 12.2x EV/EBITDA. With only 37% buy ratings, the sell-side is not sold on the name which makes this one of our favorite contrarian plays in the entire restaurant space.