This note was originally published at 8am on April 15, 2015 for Hedgeye subscribers.

“The avoidance of taxes is the only intellectual pursuit that still carries any reward.”

-John Maynard Keynes

If any of you are like me, you hate paying taxes. Admittedly, I’m just a lowly sell side Director of Research, so I don’t make nearly as much money as many of you Masters of the Universe. That said, paying taxes every year still feels punitive.

Sure, I get the patriotic component of paying your taxes (even though I’m technically Canadian), and certainly we all do have an obligation to help those who are less off in our society. But the fact remains: our tax bill every year is astonishingly high.

In fact, in their most recent projections, the Congressional Budget Office projects that more than $2.6 trillion, or 80%, of the projected revenue for the federal government will come from the combination of individual income taxes and payroll taxes. On the other hand, corporations will contribute a paltry $328 billion to the annual revenue of the Federal government.

The bigger question is how all of this hard earned money is being spent. As a percentage of the projected 2015 Federal government outlays, the largest buckets are:

- Medicare and Medicaid – 26%;

- Social Security – 24%;

- Discretionary defense – 16%; and

- Interest – 6%

Incidentally, the deficit in 2015 is expected to be an additional -$468 billion and projected to grow to - $1.1 trillion by 2025. So if you want a long term reason why interests will be somewhat capped in the United States, it’s simply that the U.S. government can’t afford to pay high rates on the $7.6 trillion in debt it is going to have to borrow over the next decade to fund the federal budget.

Of course there is an alternative. The government could just raise our taxes and not borrow so much . . .

Back to the Global Macro Grind...

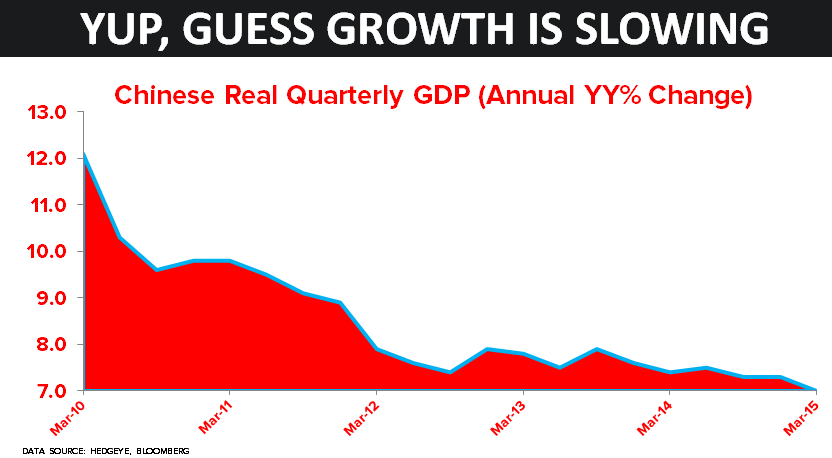

Now, inasmuch as we all wish to pay lower taxes and had more discretionary income, not all alternatives are that compelling. In fact, our system is pretty good. If this were a communist system, the government could just take all of our money! Speaking of which, China reported GDP numbers last night for Q1.

In today's Chart of the Day, we highlight Chinese GDP growth going back five years by quarterly y-o-y growth. As you can see, this is the slowest growth in that time period. The direction is very clearly that of a long term deceleration mode.

This point was reiterated in the post release press conference (yes, even Communists have pressers!) as a National Bureau of Statistics official made the following comments:

- Important to keep property market steady;

- Economy likely to remain under pressure in Q2 as destocking, clearing over capacity could take time; and

- Prioritize stable growth, jobs and profitability.

Actually, it sounds like almost the perfect economy! Although there is no word on whether anyone asked at the press conference how rail traffic in China could be down 9% year-over-year in Q1 and GDP be up 7%. But far be it for us to focus too much on the details.

Over in Europe, there was also some not-so-shocking news... The ECB left rates, gasp, unchanged! Draghi is set to have a presser of his own at 8:30am ET and while he may get tougher questions than the Chinese official did during their GDP press conference, we can be fairly certain his dovish tone is unlikely to change.

If you don’t believe us on the likelihood of a continued dovish tone, then just look at the data. Germany’s March CPI came in at a final number of +0.3% and the EU came in at +0.1%. Clearly, Draghi has a lot of data cover to continue incinerating the Euro and implement his QE program.

The more interesting pin action in Europe relates to the heightened and continued rhetoric over potential for a Greece default. The Germans are leaking that they likely won’t approve an April transfer to Greece and the Greek Prime Minister is apparently headed to Washington where he will, among other things, meet with a sovereign debt / bankruptcy lawyer from Clearly Gottlieb. This is starting to get interesting! But don’t worry, a Greek default will be completely contained . . .

Finally, a recent survey from Bank of America highlighted the strongest case we’ve noticed in a while for the bond and equity bull markets to continue. According to the survey, four in five managers think the bond market is overvalued, which is the highest proportion ever. In addition, a quarter thought equities were overvalued, the highest since 2000.

It reminds of the quote from Sir John Templeton:

“Bull markets are born on pessimism, grown on scepticism, mature on optimism and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

Indeed.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.85-1.96%

SPX 2080-2110

VIX 12.66-16.01

YEN 118.81-120.98

Oil (WTI) 48.65-54.28

Gold 1182-1219

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research