KEY POINTS

- WORSE THAN WE EXPECTED: While we were expecting light 2Q15 guidance, which missed consensus by $60.5M (11%) at the midpoint, TWTR also missed 1Q revenues, and cut full-year revenue guidance by $100M. There was a lot of noise on the call, but the culprit was ad engagements (see point 2), and tougher comps from non-recurring 1H14 tailwinds.

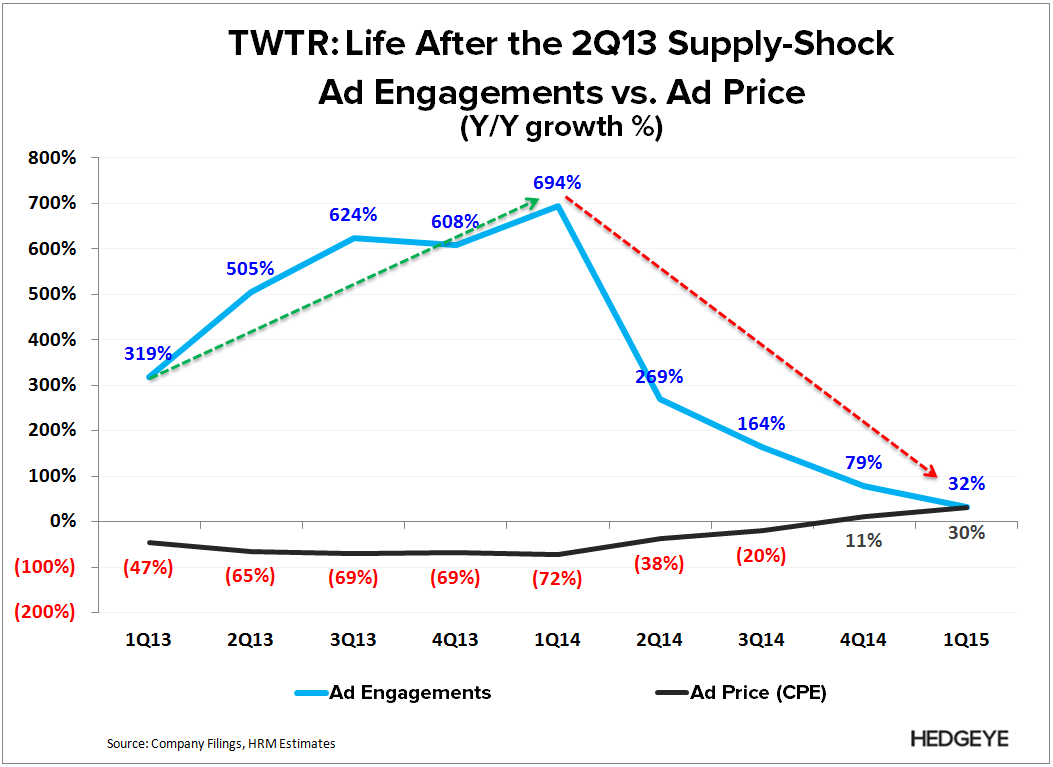

- THE ISSUE WITH THE MODEL: TWTR’s recent strength in monetization had been driven by a rampant increase in ad load starting in 2013 (what we call the 2Q13 Supply Shock). Now that TWTR has fully comped that tailwind, it is struggling to drive the type of growth that the street is expecting since ad engagements are decelerating precipitously on a y/y basis.

- ROCK AND A HARD PLACE: While we were very encouraged by the surge in Ad Pricing (CPE), we don’t believe that can turn the tide on its own. TWTR will need to beat both revenue and MAU expectations in perpetuity to appease the street, yet its reported metrics suggest those two factors are working against each other. In short, limited options with even less breathing room.

WORSE THAN WE EXPECTED

While we were expecting a light 2Q15 guidance, which missed consensus by $61M (11%) at the midpoint, TWTR also missed 1Q revenues by $21M (4%), and cut full-year revenue guidance by $100M. Management highlighted pressure on its direct response ad products in 1Q15, citing more stringent ad engagement requirements and somewhat faltering demand from rising ad prices.

But the real culprit was decelerating ad engagements across its entire business (see point 2), and consensus estimates that weren't adequately considering from non-recurring 1H14 tailwinds (Olympics/World Cup). Collectively, we believe this was the source of the shortfall in 2Q15 guidance.

THE ISSUE WITH THE MODEL

TWTR’s monetization strength had been driven by a rampant increase in ad load starting in 2013 (what we call the 2Q13 Supply Shock), which we believe was a sudden and sustained surge in ad load that drove much of TWTR's revenue growth through 2014 (more detail in our note, and S-1 excerpt below).

TWTR: What the Street is Missing

05/19/14 09:09 AM EDT

TWTR S-1/A MD&A (11/4/2013): “The decreases in cost per ad engagement over these periods [3Q12-3Q13] were primarily due to an increase in supply of advertising inventory available in our auctions, which was partially offset by increased demand for our Promoted Products. Supply of advertising inventory increased as we expanded the distribution of our Promoted Products to our mobile applications and additional markets outside of the United States in 2012. The increase in advertising inventory provided us with additional opportunities to place ads on our platform.”

Now TWTR is seeing a precipitous slowdown in average ad engagements, which means it must find a way to drastically improve its ad targeting ability, or increase ad load at a disproportionately higher rate to achieve comparable ad engagements. That leads to a bigger problem..

ROCK AND A HARD PLACE

We were highly encouraged by the surge in Ad Pricing (CPE) in 1Q15, which not only a budding growth driver, but a testament to advertiser demand and improving products mix. However, we don’t believe that can turn the tide on its own.

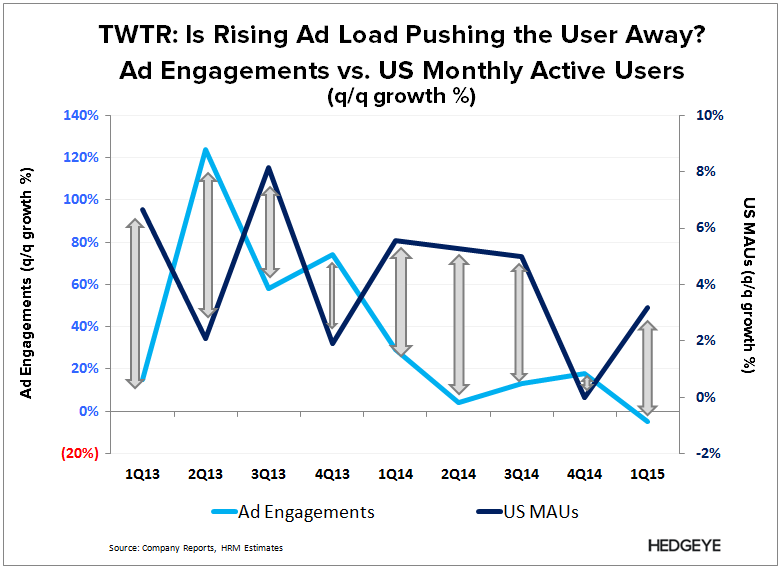

TWTR will need to beat both revenue and MAU expectations in perpetuity to appease the street going forward; yet its reported metrics suggest those two factors are working against each other. So while TWTR could gamble on a muted surge in ad load, with less potential risk of a material drawdown in CPE from the tailwinds mentioned above, there is a chance it would sacrifice MAU growth at the same.

In short, TWTR appears to have limited options, with even less breathing room from consensus.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet