Editor's Note: This is a brief excerpt and chart from today's Morning Newsletter written by Hedgeye CEO Keith McCullough. If you'd like to get ahead of consensus, we encourage you to take a look and subscribe today.

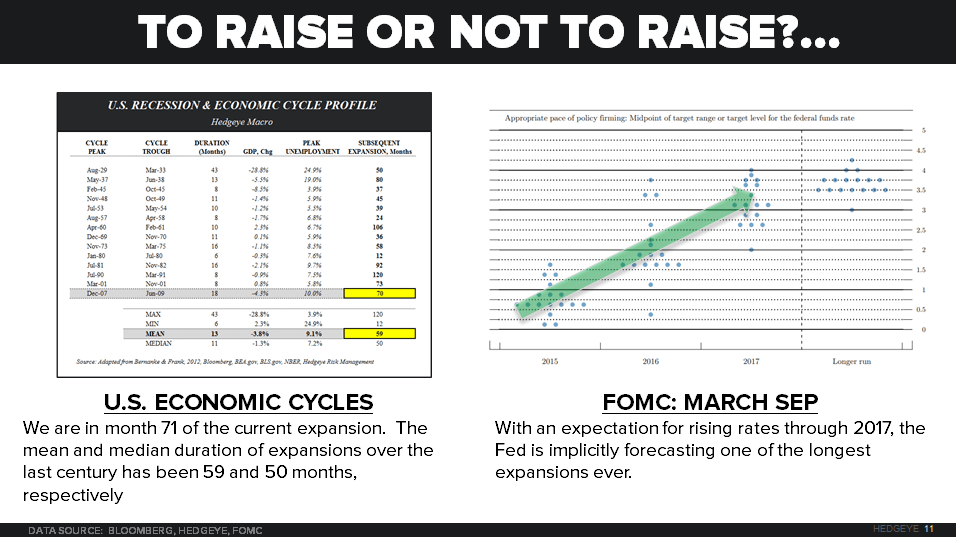

Since the last Fed meeting (March 18th) I’ve been fixated on whether or not the Fed is for real on raising interest rates into both #Late-Cycle (see our Q2 Macro Themes deck) employment gains and Global #GrowthSlowing.

While it may have sounded a little over the top, our “buy everything” call on that March 18th Fed decision to go dovish, since then (from Chinese to Japanese stocks and/or US stocks and bonds), that was the right asset allocation decision to have made...