Black Box Sales, Traffic Discouraging in March

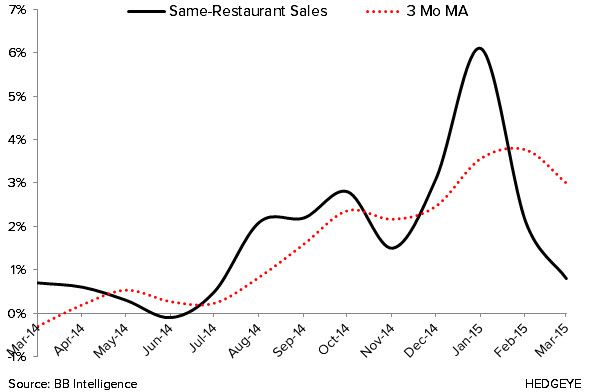

Despite the industry registering its 9th consecutive month of same-store sales growth, Black Box results for March were relatively disappointing. This comes following a soft February, during which same-store sales and traffic decelerated 400 bps and 340 bps sequentially.

Restaurant same-store sales increased +0.8%, while same-restaurant traffic decreased -2.4% during the March month. These numbers were down 130 bps and 140 bps, respectively, on a sequential basis. Importantly, 1Q15 overall was a strong quarter from a sales perspective – the strongest in at least three years – with same-restaurant sales up +3.0%. Traffic during the quarter was less inspiring, slipping down 30 bps sequentially to -0.3% from a flat 4Q14.

The widening gap between sales (or average check) and traffic suggests that the industry does not have pricing flexibility. This could become a bigger issue down the road in 2015 as companies begin facing significant labor cost pressure.

Black Box noted that the New England region was the best performing in the month, while the Southwest was the worst performing.

Employment Growth Remains Solid

All age cohorts, save the 20-24 group, had positive employment growth during the month – continuing an impressive run. Although the 20-24 YOA cohort saw employment growth decline -0.84% in the month, it is not significant enough to give us cause for concern given the strength in the other categories. However, given the extent of the sequential drop in employment growth for this category, we must monitor it closely moving forward as a continuation in this trend could have negative implications on the fast food industry.

March Employment Growth Data:

- 20-24 YOA -0.84% YoY; -374.9 bps sequentially

- 25-34 YOA +2.64% YoY; +4.4 bps sequentially

- 35-44 YOA +0.46%; +23.9 bps sequentially

- 45-54 YOA +0.50%; -83 bps sequentially

- 55-64 YOA +2.63%; +66.9 bps sequentially