COMPANY HIGHLIGHTS

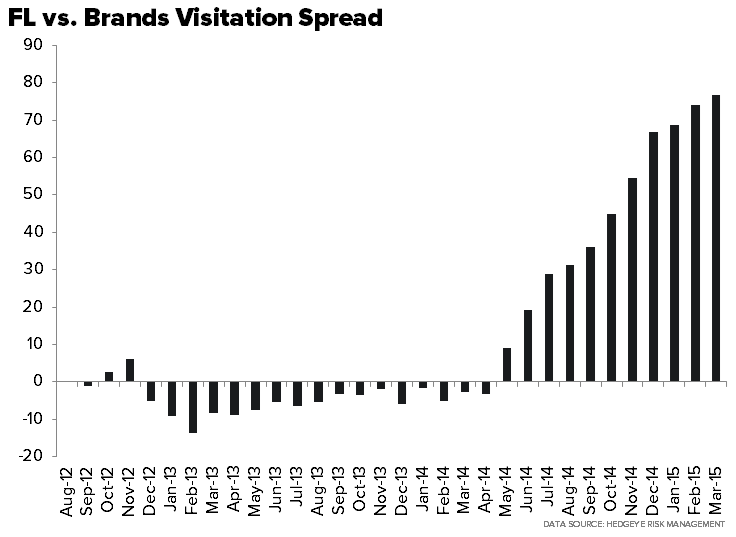

FL vs. Athletic Brands - March E-comm Visitation Stats

Tickers: FL, UA, NKE, Adi

Takeaway: In the most recent update of e-comm visitation stats we saw the brands (Nike, UA, and AdiBok) continue to outpace the growth of FL. The two (brands and FL) moved in tandem through April of 2014, and then right around the World Cup we saw a meaningful divergence. That spread has continued to blow out over the past 12 months and hit a new high again in March. That doesn't bode well for B&M retailers like FL, DKS, HIBB, FINL, etc. who have to compete with brands like NKE and UA who are pushing the direct agenda.

Over the past 3 quarters Nike has grown it's e-comm business at 70%, 66%, and 42% -- outpacing the growth of its wholesale partners. Meaning retailers now have to fight with the brands for incremental dollars from a channel that by our math should account for the majority of the industry's growth over the next 6 years.

March Monthly Comps

Takeaway: March monthly comp numbers benefited from 2 things. 1) The shift of Easter from the end of the month in 2014 to 4/5/15 this year, and 2) a miserably cold and snowy February. ICSC numbers got marginally better sequentially throughout the month on a 2yr and 3yr basis. For companies reporting on a Fiscal calendar the added March benefit should be net neutral as April slows down without the Easter boost and sales shifted from February into March. The stores concentrated in the South and MidWest regions showed the best sequential improvement on a 2yr basis which is what we'd expect after the ugly numbers reported in FEB.

OTHER NEWS

AMZN - EXCLUSIVE: Shoefitr slides into Amazon portfolio

AMZN - FAA approves Amazon drone research again

(http://www.usatoday.com/story/money/2015/04/09/faa-amazon-drone-approval-prime-air/25534485/)

Kit and Ace to Open 15 Canadian Flagships in 10 Months

(http://www.retail-insider.com/retail-insider/2015/4/kitandace)

Chanel Tests Net-a-porter Shop

(http://wwd.com/retail-news/direct-internet-catalogue/chanel-tests-net-a-porter-shop-10109870/)