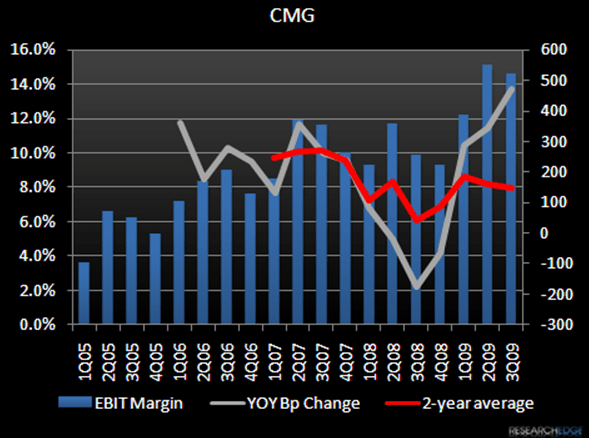

CMG reported 3Q09 earnings of $1.08, easily beating the street’s $0.86 per share estimate. The company’s same-store sales growth of 2.7% came in better than analysts’ estimates as well. Both restaurant-level and EBIT margins grew in excess of 400 bps YOY. It was a strong quarter. Unfortunately, I just don’t see any upside from here.

Margins should continue to grow in the fourth quarter, though to a lesser degree than what we saw in 3Q09, and will likely turn negative in 2010 as early as the first quarter. CMG’s same-store sales growth has held up this year relative to its peers, posting positive numbers on top of the 6% growth in the prior year, but results have been buoyed by the 6% menu price increase the company implemented in 4Q08.

In 3Q09, the 2.7% comp was driven by the 6% price increase, -1% mix and a 2.5% decline in traffic. So although CMG’s comps have remained stronger than some of its peers, the 6% menu increase has helped to cushion the traffic declines. CMG is losing guests and market share. That being said, it is impressive that traffic has not fallen off more in light of the huge menu price increase in this environment.

In the fourth quarter, more than half of this 6.0% price increase is rolling off (leaving 2.5% of price in 4Q and flat pricing come Q1). Management is not currently planning to implement any additional pricing in 2010 so overall comparable sales growth will begin to move more with traffic growth. And, as management stated on the earnings call, there is no evidence yet that consumer discretionary spending has returned. Management guided to flat transactions and sales comp trends in 2010.

This lack of pricing combined with management’s expectation for low single digit food cost inflation and 2%-3% wage inflation next year does not bode well for margins. Like I said before, I just don’t see how things get better from here unless, of course, we see a real improvement in consumer spending.

In 2010, CMG currently plans to open 120-130 new restaurants, even with the expected level of openings in 2009. However, due to the “recent pressure on developers and the corresponding reduction in number of new developments currently available for [CMG] to buy or lease” (as cited by the company), CMG is now pursuing a new real estate strategy. In the past, the company only opened restaurants in what it deemed “tier 1” trade areas. Going forward, management plans to still open about two-thirds of its new units in these “tier 1” areas, but due to the limited number of opportunities, it will also pursue what it is calling “A model sites,” which it says are “tier two trade areas which still have attractive demographics typically characterized by lower occupancy costs and develop for a substantially lower investment cost.”

Tier 2 sites are still expected to achieve cash on cash returns in the mid 30% range because the lower development, occupancy and operating costs will offset the lower expected sales volumes. These new “A model sites” will not pose a problem should they generate the expected returns, but it always concerns me when a restaurant operator appears to be compromising its real estate decisions in order to maintain growth. The fact that the company said it will pursue as many tier 1 locations as it can implies that they are still the preferred sites so these tier 2 locations signal less discipline on the part of the company for the sake of maintaining growth. These types of compromised real estate decisions often lead to declining returns. And, it is typically a bad sign when management teams start getting asked questions about possible sales cannibalization…

We have seen how that plays out and it is not good.