This note was originally published at 8am on March 23, 2015 for Hedgeye subscribers.

“One would hope that the Fed will be very cautious about tightening.”

-Ray Dalio

That’s what Global Macro man, Ray Dalio, was hoping for in his Bridgewater’s Daily Observations note from March 11, 2015. He believes that it is “best for the Fed to err on the side of being later and more delicate than normal.”

While hope is not a risk management process, I was hoping for the same last week. And my fundamental research call for lower interest rates for longer (as the rate of change in both Global Growth and Inflation slow) remains intact.

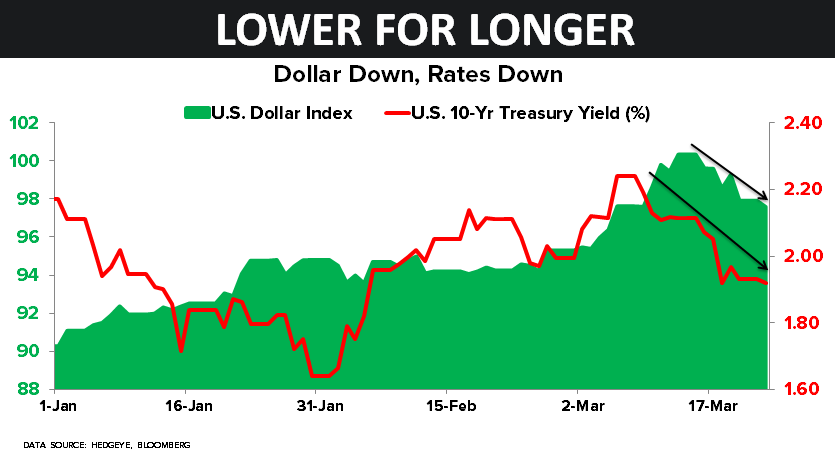

At the same time, I am not hoping for a devalued US Dollar. US companies who are reporting international revenues and earnings are. The only reason why US GDP growth isn’t falling below 2% is because real US consumption growth loves #StrongDollar.

Back to the Global Macro Grind…

The problem, of course, is that when the Dollar is rising and Rates are falling (at the same time), you get #Deflationary forces in asset prices tied to inflation expectations. This is where Wall Street and Main Street are hoping for different things.

Last week, on the dovish Fed “news”, the US Dollar and Interest Rates dropped:

1. US Dollar Index (-2.4% for the week) had one of its biggest down weeks in the last 6 months

2. US Treasury Yields (10yr) dropped 18 basis points on the week to 1.93%

That was the very immediate-term move that Dalio and I were hoping for, as it took out the big bang risk of the Federal Reserve making a policy mistake at the end of multiple cycles.

On Down Dollar:

1. The Euro had one of its biggest up weeks in the last 6 months, +3.1% to -10.6% YTD

2. Gold had a big bounce (Gold loves Down Dollar, Down Rates) of +2.8% to 0.0% YTD

3. Commodities (CRB Index) finally stopped making new weekly lows, +1.6% at -6.9% YTD

4. Emerging Market Stocks (MSCI Index) bounced +3.2% to +1.4% YTD

5. Latin American Stocks (MSCI) had an even bigger bounce +5.4% to -9.6% YTD

Meanwhile, on Down Rates:

1. Biotech Stocks (IBB) ramped another +6.0% to +20.8% YTD

2. REITS (MSCI Index) ripped a +5.6% move to +6.8% YTD

3. NASDAQ tacked on another +3.2% to +6.1% YTD

4. Long Bond (TLT) had a great week, +3.8% to +4.6% YTD

5. SP500 had its 1st up week in the last 3, closing +2.7% putting it back in the black at +2.4% YTD

In other words, most of the #Deflation trades bounced to something less-than-terrible (both absolute and relative) for 2015, whereas the real alpha trending in macro markets continues to play to the lower-rates-for-longer camp’s advantage.

All the while, consensus was setup for a rate-hike. Here’s where futures and options net positioning (CFTC non-commercial positions) are:

1. SP500 (Index + Emini) net SHORT position rose to its highest of 2015 at -76,511 contracts

2. Long-term Treasuries (10yr) net SHORT position came off its YTD highs to -132,900 contracts

3. The Euro’s net SHORT position got pinned at YTD highs of -201,135 contracts

With the SP500, Long-term Treasuries, and Euros all straight up from within six minutes of the FOMC announcement, Consensus Macro getting squeezed provided for a cherry on top of what was an admittedly hoped-for reprieve in policy mistake expectations.

Hence my “buy everything” call on the news. But now what? Do you sell everything? I don’t think so – I’m definitely not selling Long-term bonds and/or anything that looks like a bond. Not if the market is expecting the Fed to deliver on “data dependence.”

While this week’s CPI data should get a small lift from Oil bouncing like it did in FEB, that #deflation data is going to look very dovish when it gets reported for MAR (in April). Friday’s final GDP report for Q414 will also look slower, sequentially.

Fortunately, our rate of change models are not built on hope.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.89-2.03%

SPX 2080-2119

RUT 1238-1275

USD 97.17-100.39

EUR/USD 1.04-1.08

Oil (WTI) 42.04-48.03

Gold 1159-1188

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer