Recent Notes

03/23/15 Monday Mashup

03/23/15 DRI: Room to Breathe

03/27/15 MCD: Putting the Activist Thesis to the Test

Events This Week

- No Events

Recent News Flow

Monday, March 23rd

- DRI upgraded to outperform at Telsey Advisory Group with a $77 PT.

- RT downgraded to neutral at Longbow Research.

- DENN announced the adoption of a pre-arranged stock trading plan for the purpose of repurchasing a limited number of shares of its common stock between April 6, 2015 and May 6, 2015.

Tuesday, March 24th

- DNKN promoted Jack Clare to the newly created position of Chief Information and Strategy Officer. Mr. Clare will be a member of the Dunkin’ Brands Leadership Team and will continue to report directly to the CFO, Paul Carbone.

Wednesday, March 25th

- No material news

Thursday, March 27th

- No material news

Friday, March 28th

- RRGB target was raised at Miller Tabak following recent checks that suggest upside to 2015 same-store sales guidance.

Commodities

Sector Performance

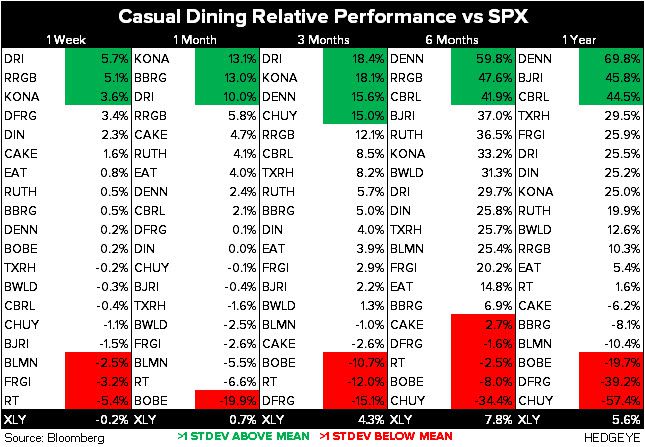

The SPX (-2.2%) outperformed the XLY (-2.4%) last week. Both casual dining and quick service stocks, in aggregate, outperformed the SPX.

Quantitative Setup

From a quantitative perspective, the XLY remains bullish on an intermediate-term TREND duration.

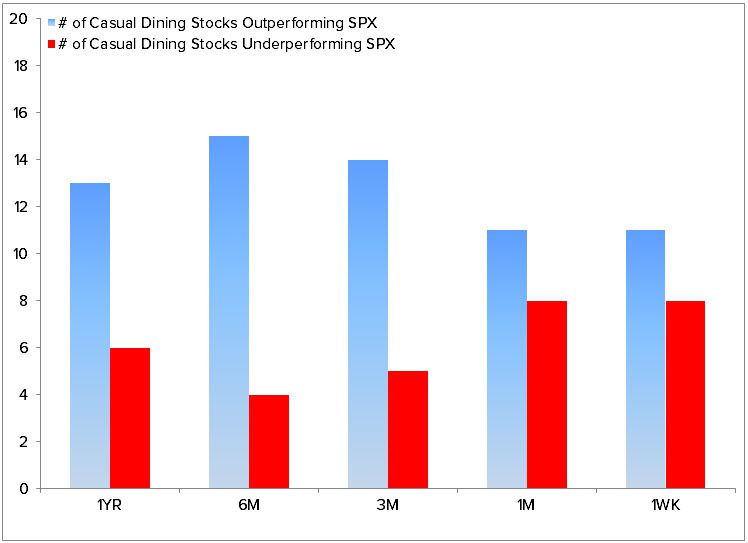

Casual Dining Restaurants

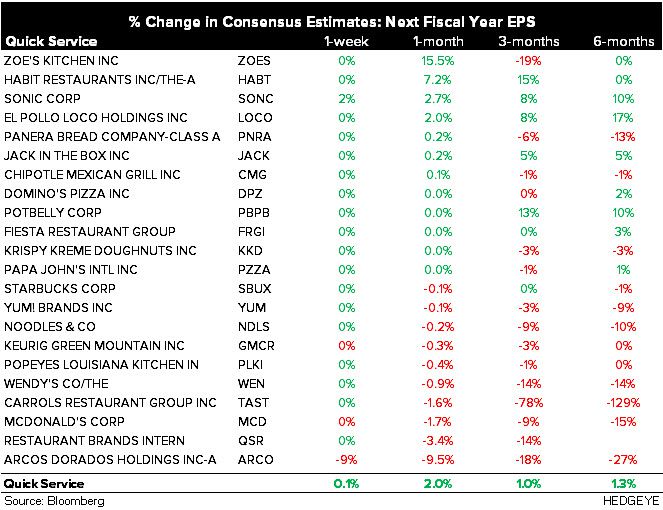

Quick Service Restaurants