“Now it is necessary to get to the grindstone again.”

-Ernest Hemingway

For those of you who are Hemingway fans, you’ll remember that classic one-liner.

He penned it at the end of his preface to “The First Forty Nine” in 1938. He was preparing for the next stage of his life, writing from Finca Vigia (his home in Cuba). That’s where he’d spend the last 22 years of his life, before dying in 1961.

For those of you who didn’t know, that one-liner inspired “Back To the Global Macro Grind…” While my English Lit professor @Yale was very close to failing me in 1995, thank God she saved me with Hemingway’s short-form writing examples.

Back to the Global Macro Grind…

With the Federal Reserve having not made a monetary policy (rate hike) mistake last week, Fed Vice Chair, Stanley Fischer, reiterated lower-rates-for-longer at his rock-star-status meeting of the mainstream minds yesterday.

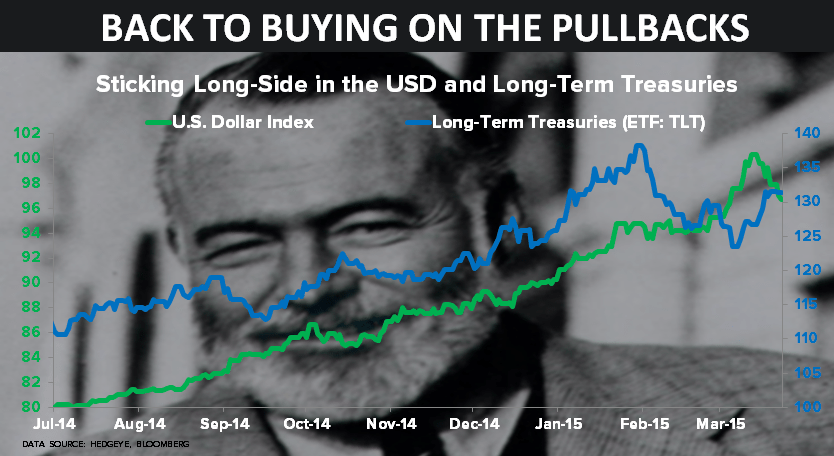

No matter where you’ve been positioned, here we are. If I were you, with both interest rates and the US Dollar grinding lower this morning, this is what I’d be doing next:

- Buying US Dollars on red; Shorting Euros on green

- Shorting Commodities and their related stocks/bonds on green

- Buying Long-term Bonds (and stocks that look like bonds) on red

In other words, from a Foreign Currency market perspective, I’ll be fading (doing the opposite of) the counter-TREND move. But from a Fixed Income standpoint, I’ll stay with what’s been a very bullish intermediate-term TREND.

The main reasons for that are twofold:

- The best way to be positioned for Global #Deflation and #GrowthSlowing remains being long Long-term Treasuries

- The best way to stay with the Europeans, Japanese, and Chinese devaluing their currencies, is to be long US Dollars

On Global #Deflation, If you grind through all of the recent Global Macro data, it’s not that hard to see:

- Germany’s producer prices (PPI) for FEB were -2.1% year-over-year (vs. -2.2% in the prior month)

- Finland’s producer prices (PPI) for FEB were -1.8% year-over-year (vs. -1.9% in the prior month)

- United Kingdom’s PPI for FEB was -1.8% year-over-year (vs. -1.9% in the prior month)

And while some of these year-over-year #deflations slowed month-over-month, don’t forget that this all happened in FEB when most things commodities had a Down Dollar bounce. In March, all of the #deflation data should accelerate to the downside again.

On Global #GrowthSlowing (key word there is Global), here’s your data update:

- Eurozone PMI for March 51.9 (vs. 51.0 in FEB)

- Chinese PMI for March 49.2 (vs. 50.7 in FEB)

- Japanese PMI for March 50.4 (vs. 51.6 in FEB)

Chinese and Japanese stocks are running right at YTD highs of +13-14% on those sequential slowdowns. Why? #GrowthSlowing begets more currency burning expectations, which begets higher stock prices in those currencies.

Meanwhile everyone who is long Europe who thinks the German PMI data (which was good, not great, sequentially at 52.4 MAR vs. 51.1 in FEB) is going to carry all of Europe for the rest of the year (France’s PMI sucked at 48.2), has a simple question to answer:

Is the European “growth story” (going from recession to something hoped-for that is less than recessionary) intact with Draghi allowing all of his Burning Euro accomplishments to get unwound?

From a research perspective, the answer to that question is an unequivocal no. Yesterday Draghi was thumping his Italian chest hairs celebrating the “benefits of a weaker Euro.” The immediate-term risk range for the EUR/USD also blew out to $1.03-1.10.

Not to be confused with my English Lit professor, my calculus guy in New Haven never threatened to fail me. The math of the matter is that as risk ranges “blow-out” like the Euro’s just did, variance rises, and so does my expected volatility for the FX market.

As you just witnessed with the Fed’s latest move, in reaction to unexpected currency strength, the only play in the central planner’s playbook is to get easier, not tighter. So, now it’s your turn Super Mario and Mr. Kuroda – prepare your respective FX grindstones.

Our immediate-term Global Macro Risk Ranges are now (with intermediate-term TREND research views in brackets):

UST 10yr Yield 1.85-2.02% (bearish)

SPX 2080-2117 (bullish)

RUT 1 (bullish)

Nikkei 192 (bullish)

VIX 12.79-15.94 (bullish)

USD 97.01-99.24 (bullish)

EUR/USD 1.03-1.10 (bearish)

Yen 119.39-1.21.90 (bearish)

Oil (WTI) 42.42-48.28 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer