On Monday, the S&P 500 closed at 1,097, up 0.9% on the day. The S&P 500 has now risen nine of the last ten days, albeit on decelerating volume the S&P 500 hit another higher-high, while the USD hit another lower-low.

Driving the market higher is (1) the trend of better-than-expected Q3 earnings and upbeat guidance, (2) M&A generally, but the highlight is in Technology.

Yesterday’s portfolio activity included selling our long position in the XLU and EWT and buying SAFM and MPEL. Todd Jordan has Keith warming up the Macau bus again; we are buying MPEL back on a down day. We also covered our short in NKE.

We continue to be short the XHB and expect that the recent enthusiasm around the home builders to wane in the coming days. The National Association of Home Builders housing market index dipped to 18 from 19 in September, falling below market expectations for a reading of 20. Home builder sentiment is waning for the market for newly built single-family homes, as the November 30 expiration of the government's $8,000 tax credit for first-time buyer’s approaches. The WSJ also notes today that the IRS is examining more than 100,000 suspicious claims for the first-time home-buyer tax break. Not a good sign that the program will be extended.

The momentum behind the “currency creditability crisis” continued to weigh on the dollar index, which fell for five of the last six days, finishing down 0.35%. For the first time in ten days the VIX rose 0.3% on the day. In early trading today Oil traded above $80 as the dollar index fell to its lowest level since August 2008.

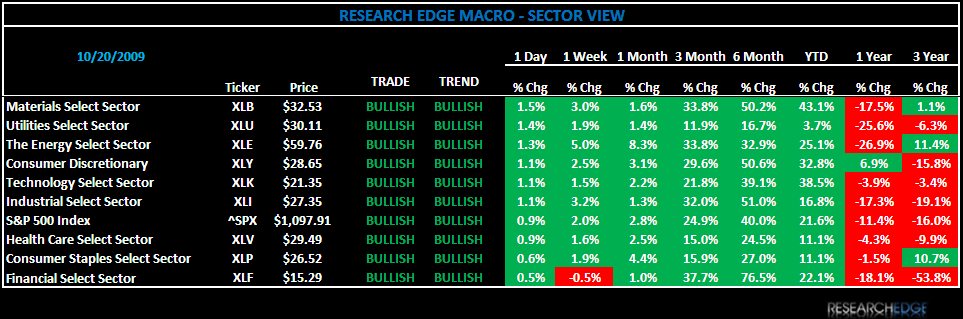

Yesterday, six sectors outperformed the S&P 500 and every sector was up on the day. The three best performing sectors were Energy (XLE), Materials (XLB) and Utilities (XLU), while Financials (XLF), Consumer Staples (XLP) and Healthcare (XLV) were the bottom three.

Yesterday, the Financials were the worst performing sector and it was not the only sector down over the past week. The banks are dragging the group down, with regional banks being hit the hardest. This was highlighted by the results from BBT yesterday, on concerns over credit deterioration. The trend will likely continue as STI, SNV and MI are all scheduled to report on Thursday.

Today, the set up for the S&P 500 is: TRADE (1,079) and TREND is positive (1,003). Day 7 of perfection - the Research Edge quantitative models have 9 of 9 sectors in the S&P 500 positive on TREND and 9 of 9 sectors are positive from the TRADE duration.

The Research Edge Quant models have 1% upside and 1.5% downside in the S&P 500. At the time of writing the major market futures in the U.S. were higher.

The Research Edge MACRO team.