This note was originally published at 8am on February 26, 2015 for Hedgeye subscribers.

“They haven’t repealed the laws of arithmetic, yet, anyway.”

-John Malone

Malone wasn’t talking about economic-central-planning authorities, but he could have been. The American grandmaster of debt leverage, EBITDA, and equity value creation would probably be the best overlord of our markets, ever. It’s too bad he’s a libertarian.

Yep, the largest land owner in America (2.2M acres) not only founded Liberty Media – but he’s a libertarian. That makes some of the Yale alumni in the economic-gravity-smoothing department cringe. And I like it.

Born, raised, and educated in Connecticut, Malone is a Yale man. He’s rightly featured as one of the best CEOs in US history in the book I’ve been citing as of late, The Outsiders, by William Thorndike. If you want to be a hard core capitalist, you have to study John Malone.

Back to the Global Macro Grind…

Hard core capitalists who believe in things like arithmetic and second derivative math, meet your makers – these central planning “folks” are going to go to hell’s end until they get reported “inflation” – and guess what? For now they aren’t going to get it!

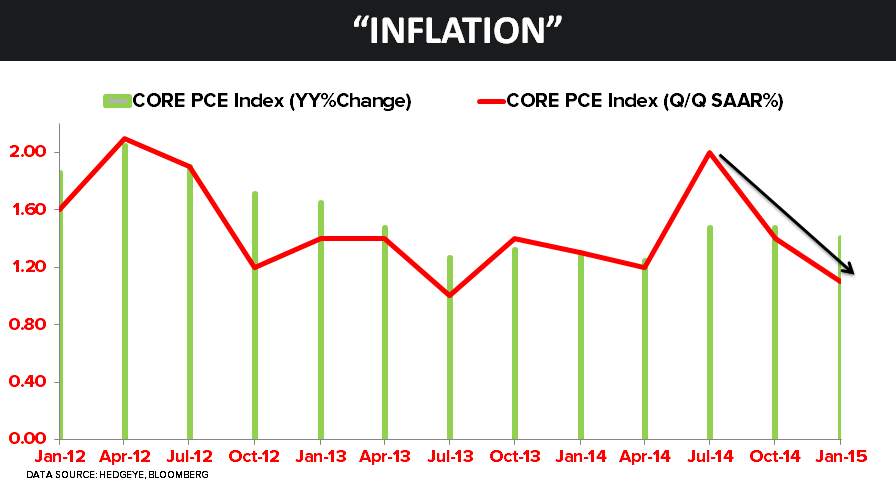

In today’s Chart of The Day we show what the Federal Reserve currently uses as its definition of “inflation” – something academic wonks call “Core PCE”, or the US Personal Consumption Expenditure Core Price Index.

Other than this chart going straight down for the foreseeable future (until at least Q3), here’s what this time-series means to me:

- Instead of using real-world inflation, Bernanke deferred to a made-up calculation that fit his policy narrative

- In 2011, the US Dollar hit its lowest-level since 1978 - that’s what perpetuated the highs in this chart

- But since, at $1900 Gold, “there was no inflation” (per the Fed); it said it was just about right at 2%

I can guarantee you that everyone Paul Krugman influences in the Yale and Princeton econ departments completely disagrees with the context I just provided you. So that means I’m probably onto something…

Taking this to a higher-level of an investor’s real-time education, why does this chart matter now?

- Both the 1 and 3 year “compares” (comps) for reported CPI are very difficult

- When the comps are hard, the central tendency of the current data is to the downside

- Janet is going to be waiting for Godot if she’s looking for this sucker to hit her +2% “target” again

As importantly, the European definition of “inflation” continues to be, well, #deflationary. This morning Belgium reported at -0.4% year-over-year Consumer Price Index (CPI). That’s both in line with other countries in the Eurozone and nowhere near the +2% “target.”

If you buy into our Global #Deflation Theme, you have been buying the living daylights out of Long-term Bonds on all pullbacks for the last year, and you’ve been getting paid. Here’s where Big Macro 10yr yields are falling to this morning:

- Germany Bund 10yr = 0.29% (record low)

- Japanese Government Bond (10yr) = 0.33%

- Dutch 10yr = 0.37%

- French 10yr = 0.60%

- US Treasury 10yr = 1.94%

Never mind that the Swiss have a 10yr yield of 0.01% for a minute and tell me how, on God’s good earth, that the US 10yr Yield isn’t going to mean revert lower… if I’m right on both Global growth and “inflation” slowing, that is…

As many of you who have followed me for a long-time know, I haven’t been a perma bull on the Long Bond. In fact, I was a raging Long Bond bear in 2013 when our modeling was signaling US #GrowthAccelerating.

But, newsflash: US growth didn’t accelerate in Q4 of 2014 – alongside Global growth, on both a sequential and year-over-year basis, it slowed. Unless they repeal the laws of arithmetic and change the “growth” definition too, that will be headline news on Friday morning.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.81-2.05%

SPX 2087-2121

DAX 11008-11302

VIX 13.39-16.71

USD 93.73-94.81

EUR/USD 1.12-1.14

YEN 118.16-120.46

Oil (WTI) 48.09-53.66

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer