“If you tell the truth, you don’t have to remember anything.”

-Mark Twain

Let’s call a spade a spade - it’s hard to be 100% honest. I mean we all stretch the truth a little at times. Maybe it is small things like saying you are 6’2" when really you are 6’1", or saying your fund was up double digits when really it was up 8.5% for the year. On some level, it is just human nature to tell a tall tale.

In a paper published in Human Communications Research in 2010, Professor Kim Serota and colleagues attempted to determine exactly how often people lie in their everyday lives. She conducted an online survey of 1,000 people that asked how many times the participant lied in the last 24 hours, the conclusions were as follows:

- The average number of lies told per day was 1.65

- Only 40.1% reported telling a lie in the last 24 hours

- 22.7% of all lies were told by one percent of the sample, and half of all lies were told by 5.3% of the sample

- No statistically significant sex differences were found in the propensity to lie

So undoubtedly you get the ironic point of the survey, the most honest people in the survey were the ones that actually lied the most.

Back to the Global Macro Grind...

As it relates to central bankers, we haven’t exactly called them liars, but certainly they have misled the investing masses at times. The one exception to that may be the honest Canadian at the head of the Bank of England, Governor Mark Carney.

Yesterday, Carney said what a lot of central bankers aren’t allowed to say, or are afraid to say, which is that the Bank of England would be “foolish” to fight current low inflation. Specifically, Carney said that:

“That’s one of the key judgments the MPC has to make . . . the one thing we can’t do and the thing that would be extremely foolish would be to try and lean against this oil price fall today and try to provide extra stimulus up at this point in time.”

Carney’s point was that to add stimulus now would only lead to undue volatility in the English economy - a lesson certainly the Japanese and ECB should be learning in spades, only they are not.

Back in American central banking land, the WSJ’s Jon Hilsenrath, among other Fed watchers, is suggesting the next move by the Fed will be rhetorical in nature. That is, the Fed is purportedly strongly considering removing the word “patient” from its policy statement. The implication of this move would be that the door would then be left open for rate increases. Well, that is assuming Fed insiders aren’t lying to Hilsenrath and his cadre.

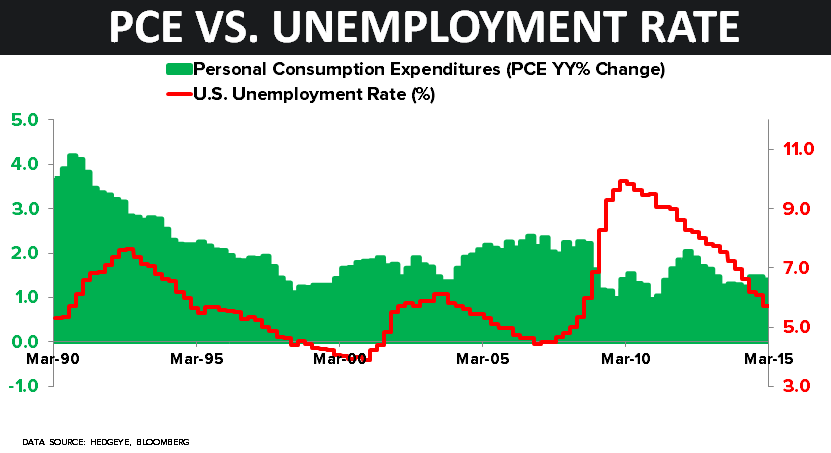

In the Chart of the Day below, we look at employment versus PCE going back some 25 years. As usual, stats don’t lie and what the chart shows us is that the Fed is going to face a real conundrum as it relates to reported inflation and its mandate. Either they can find the truth, like Governor Carney, or yet again the Fed might surprise us all on the dovish side because as the chart clearly shows, at least based on PCE, we are in a deflationary environment.

Now the caveat to that is that employment, at least on the headline metric of the unemployment rate, is indicative of an economy that is operating at tight capacity. Employment is also the foundation of the thesis for most equity bulls. Historically, of course, the employment rate has been much more of a lagging indicator than a leading one. On this topic, we are actually going to do a deep dive on employment on Tuesday March 17th at 11am on a conference call titled: “Employment: The Good, The Bad and The Ugly”. Ping sales@hedgeye if you’d like dial in information.

Switching to Hedgeye stock calls, our Internet guru Hesham Shaaban, has been loudly calling out the management of Yelp. If @HedgeyeInternet is correct in his analysis, Yelp management is likely in the category of the one percent of the sample that tells more than 22% of the lies every day. In a note earlier this week on Yelp titled, “Hiding the Bodies”, Shaaban wrote:

“We originally believed revenues from SeatMe (reservation service) would be reclassified from YELP's Other Services segment into its core Local Advertising segment starting in 1Q15. However, that likely happened in 1Q14. We just didn't realize it because the reclassification wasn't explicitly disclosed in any of YELP's filings until its 2014 10-K filed two weeks ago. Given that its previously-reported 2014 quarterly segment revenues haven't changed within its recently-filed 10-K, we have to assume that the change already occurred in 1Q14.”

So the moral of the Yelp story is, it seems, that if the revenue doesn’t fit your tall tale then just reclassify, but just don’t tell anyone.

The larger issues with Yelp, though, is customer attrition. By Shaaban’s analysis, Yelp loses roughly 80% of customer every year, so the attrition rate is very high. Therefore unless Yelp’s TAM (total addressable market) is unlimited, which it is not, eventually growth will slow and dramatically slow for Yelp. And in a story stock like Yelp, trust me you don’t want to be there when the growth music stops.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.96-2.26%

SPX 2034-2080

DAX 110

VIX 14.27-17.13

EUR/USD 1.05-1.08

Oil (WTI) 48.04-50.44

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research