This note was originally published March 04, 2015 at 21:32 by Hedgeye Industrials Sector Head Jay Van Sciver.

Overview

Outside of housing/construction, much of the recent industrial data point to weakening activity. Some of the deceleration may relate to broader deflationary trends, such as weaker resource-related capital spending.

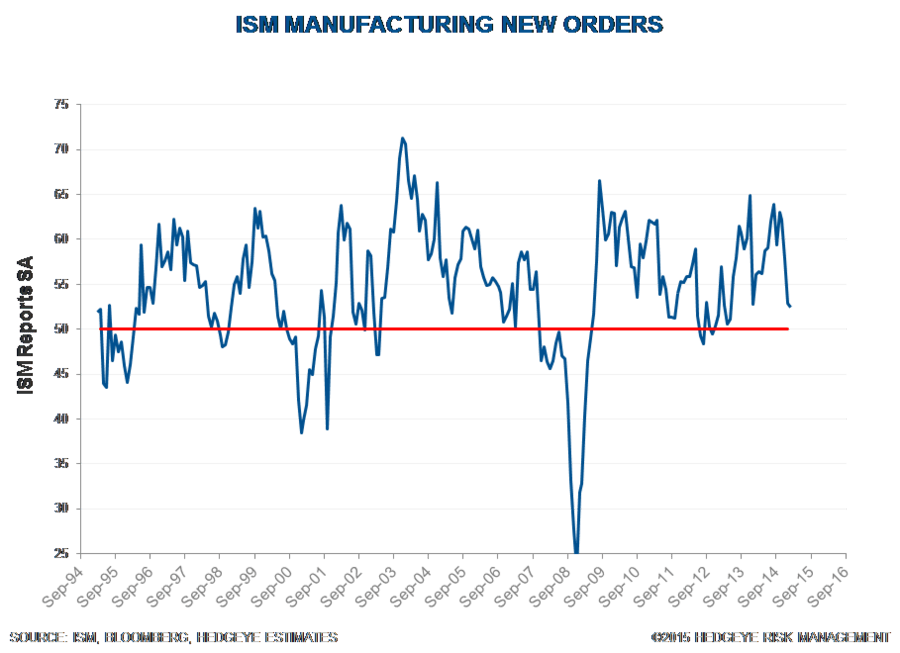

ISM New Orders

While still in expansion territory, both the Manufacturing and Nonmanufacturing New Orders readings weakened.

Intermodal Rail Traffic

While weather and port disruptions play a part, the recent meaningful declines in intermodal rail traffic are the first since the great recession.

U.S. Manufacturers New Orders

While we typically track the more timely ISM Manufacturing New Orders readings, other measures also point to a deceleration in orders. Ex-Defense also shows YoY declines.

U.S. Crude-By-Rail

Crude-by-rail volume showing slight year-on-year declines in recent weeks.

Single Family Building Permits

Residential construction/housing appears to be positioned well into 2015.

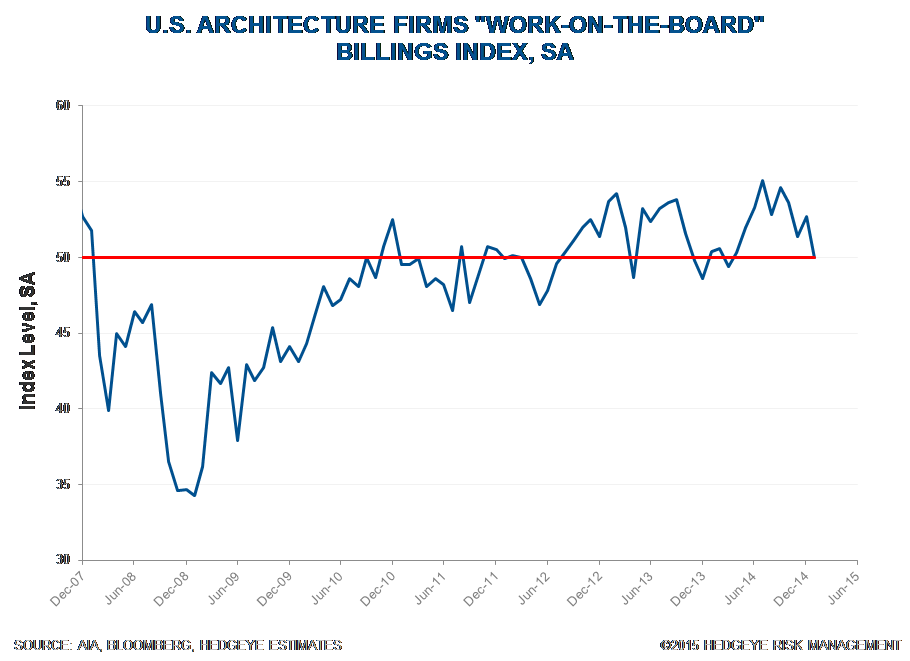

Architectural Billings Index

While the ABI points to strengthening activity through much of 2015, the recent 49.9 reading points to a deceleration into 2016. Of course, by then no one will remember where ABI was 11 months prior.

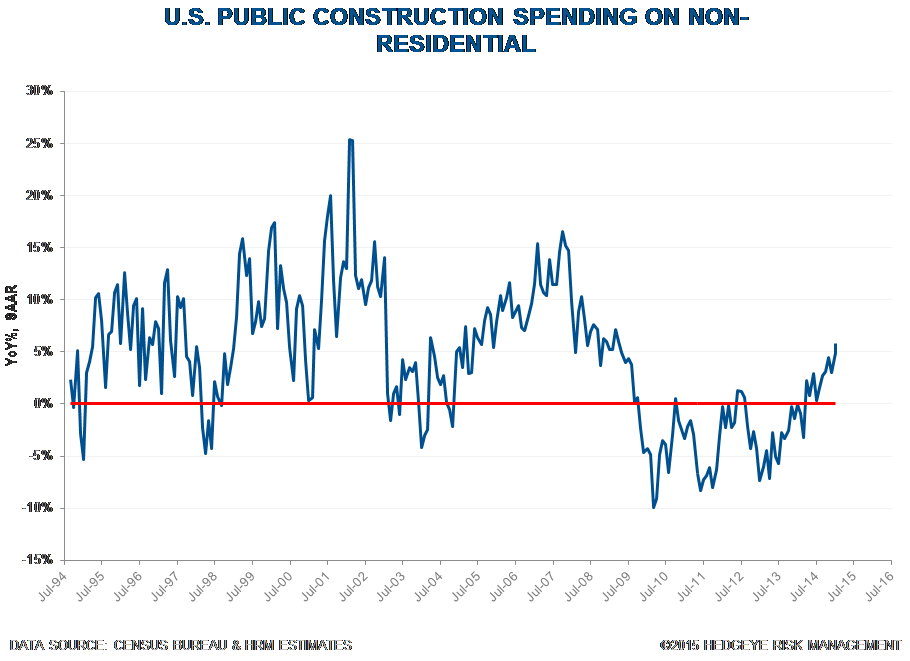

Public Nonresidential Construction Spending

After several years of being a drag on nonresidential construction, public sector spending is showing solid signs of growth.

Inventory to Shipments Ratio

Inventory is building relative to shipments, which is typically a negative indicator for higher cost transportation spending. It is also typically associated with weaker economic activity.

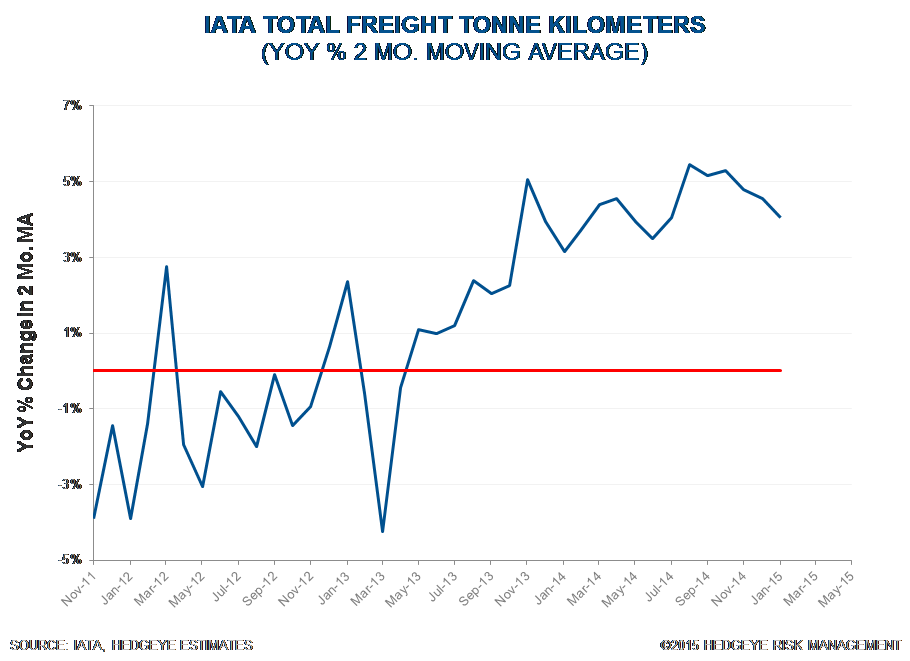

IATA International Airfreight FTK Growth

Even airfreight growth seems to be slowing, which is surprising given recent declines in fuel costs. (Freight Ton Kilometers = FTK)

Truck Demand Index

While some of this may be weather/port related, it is not a positive indicator for heavy trucks.

US Truck Backlog to Build

From a trading perspective, we look to enter truck OEMs when this reading is low. Recent slowing may portend an entry opportunity for that group.

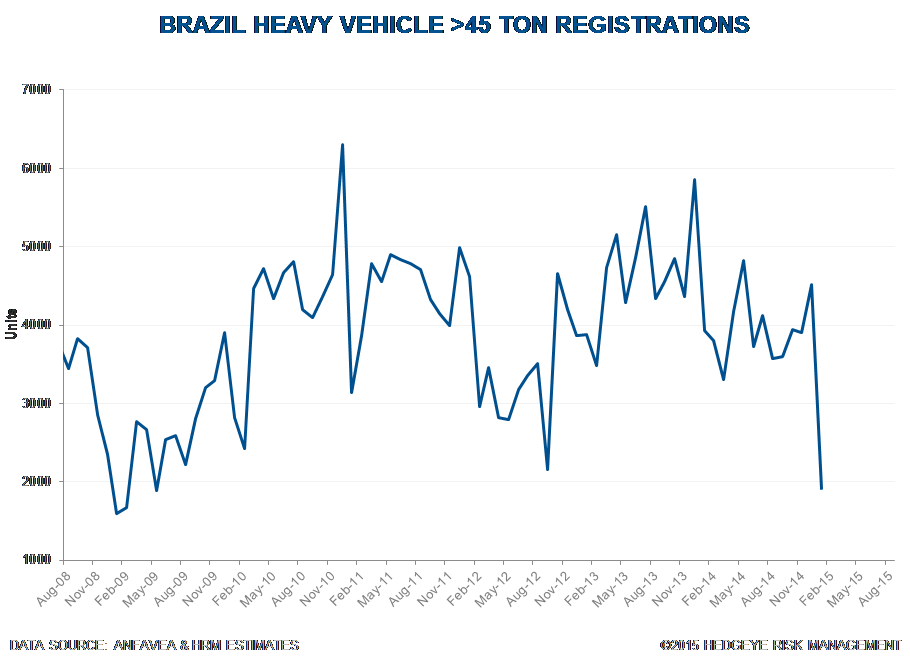

Brazil Heavy Truck Registrations

CRB Index

A stronger dollar and deflationary trends are not typically favorable for Industrial top-lines.

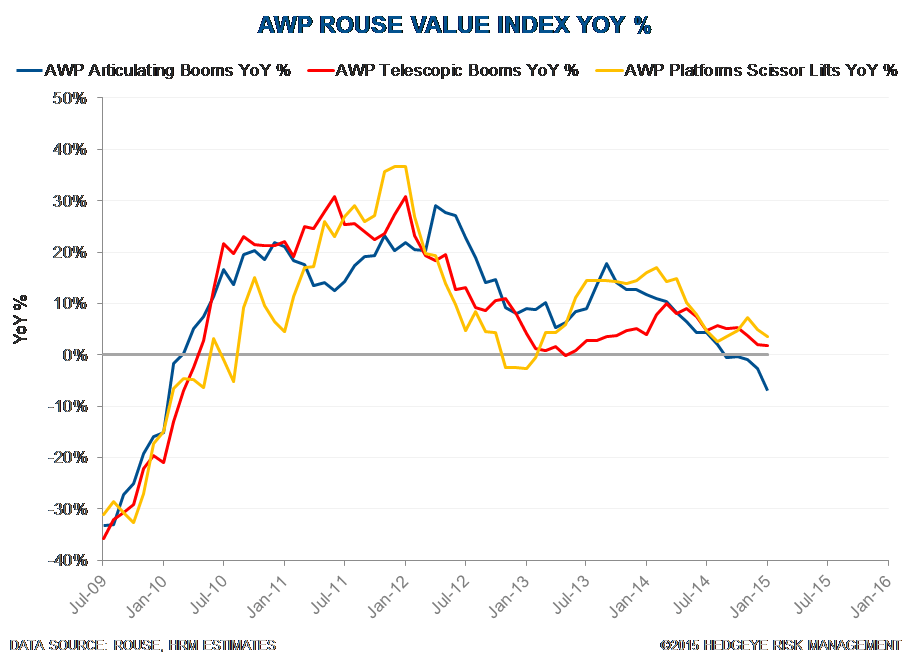

AWP Value Index

This series seems to be decelerating. (AWP = Aerial Work Platforms)

Business Jet Flights YoY%

Growth appears to be slowing in recent months, although the January decline may be partly weather related.

China HSBC PMI

Ending on a more positive note, the HSBC China Manufacturing PMI has moved into positive territory.