COMPANY HIGHLIGHTS

NKE - Top Selling Shoes On eBay

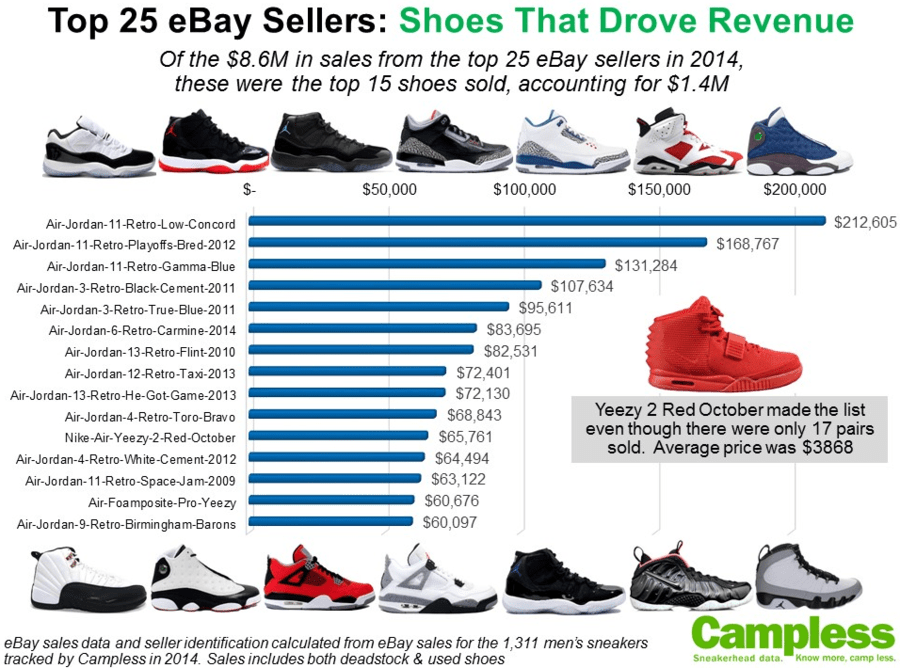

Takeaway: eBay is a better barometer than any other for the aftermarket demand of a sneaker in the 'sneakerhead' collector community. To that end, it is no surprise that Nike absolutely dominated the list of top shoes. Actually, 'dominated' is not the right word. It monopolized the list. Out of the top 15 sneakers, 13 of them are Jordans, and two are Nike (one of which -- the Air Yeezy -- sold at an average price of $3,868. Yes, that's nearly $4k for a pair of kicks.

AdiBok - Reebok's Pump Is Back

(http://www.bloomberg.com/news/articles/2015-03-04/reebok-s-pump-is-back)

Takeaway: As gimmicky as it is, The Pump technology is one of the few innovations that Nike kicks itself for not doing before Reebok. Back in 1991 Reebok sold its basketball pump shoe for $170, which is about $320 in today's dollars. Perhaps a prohibitive price is what caused The Pump to die on the vine. But the new version (which gaudily says The Pump in what appears to be a 200pt font size) sells for $110. If you want to preorder a pair, you can't go to Foot Locker, Finish Line, Hibbett or Dick's -- you have to go to reebok.com. That is, until March 10 when AdiBok will open the spigot to certain retail channels. We suspect they'll give 1 or 2 colorways/styles to each retailer, so everyone can tout it as an exclusive. But all colors, all styles, in all sizes are all available on reebok.com.

COST - 2Q15 Earnings

Takeaway: Everyone knows about the Fx and cheap gas pressures squeezing the top line, but in the face of that COST still leveraged 4% sales growth into 29% earnings growth. It wasn't entirely clean as tax benefits gave them an extra $0.10, but you're still looking at EBIT up 21% in the quarter. That being said, membership income came in lower than expected and margins in the quarter were the best they've been in 4 years. The sales to inventory spread was favorable for the 3rd quarter running, but it was the tightest gap we've seen. In order to offset the considerable top line pressures in the near term, COST will have to tightly manage that line. While we're remiss to short the stock of a great company like COST when it's clearly executing on its business plan, we're certainly not going to rush out and buy it at 27x earnings based on what we see today.

OTHER NEWS

DG - Dollar General: West Coast losses will be lasting

ASNA - Ascena Retail Group Announces Appointment of Randy L. Pearce as Lead Independent Director

(http://phx.corporate-ir.net/phoenix.zhtml?c=81419&p=irol-newsArticle&ID=2022840)

ANN - Report: Bain, Golden Gate both want Ann Inc.

(http://www.chainstoreage.com/article/report-bain-golden-gate-both-want-ann-inc)

PBY - Bob Nardelli joining Pep Boys board

(http://www.retailingtoday.com/article/bob-nardelli-joining-pep-boys-board)

Bealls to launch new specialty store concept, Bunulu

(http://www.chainstoreage.com/article/bealls-launch-new-specialty-store-concept-bunulu)