Summary

We had expected CAT’s 2014 10-K to be interesting, and we were not disappointed. Our review of CAT and CAT Financial’s 10-Ks leaves us feeling as though we missed as much as we saw, with the subpoenas/investigations sticking out most clearly. CAT seems to be experiencing ‘investigation creep’ from the SEC, and a pretty unhappy IRS, too. For starters, CAT should probably impair the BUCY goodwill just to get it over with. Warranty challenges, material weakness in controls at CAT Financial, and the impact of completing distributorship divestitures also seem noteworthy.

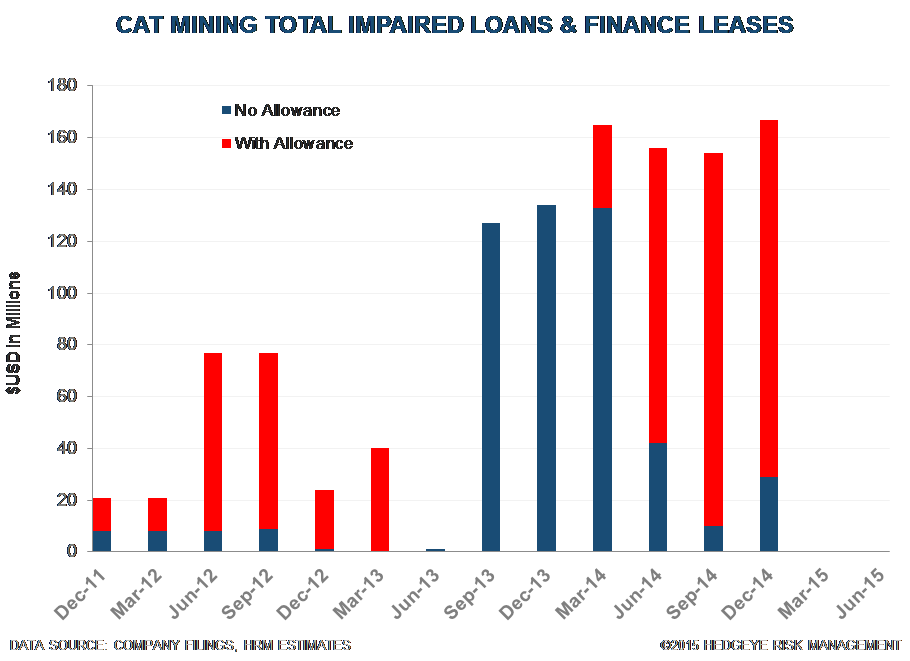

In next year’s 10-K, we would look for Caterpillar Financial to take the stage with mining and oil & gas exposures as sources of possible losses, since, “receivables from customers in construction-related industries made up approximately one-third of [their] total portfolio.” Mining, as a category, is generally only top-tier miners, with smaller mining operations categorized in their respective regions. While we took Short CAT off of the Best Ideas list, we would look to add it back if the shares continue to bounce.

Key Items

Grand Jury Subpoena on U.S./Non-U.S. Subsidiary Profits, Cash: This can’t really be a positive. There has been significant speculation by shorts in CAT on the role of advance purchase transactions, tax reduction strategies, and earnings/inventory management. We will be interested to see how it turns out. The SEC correspondences linked below provide clues, but the lack of clear disclosure seems troubling. What, exactly, is the allegation here?

“On January 8, 2015, the Company received a grand jury subpoena from the U.S. District Court for the Central District of Illinois. The subpoena requests documents and information from the Company relating to, among other things, financial information concerning U.S. and non-U.S. Caterpillar subsidiaries (including undistributed profits of non-U.S. subsidiaries and the movement of cash among U.S. and non-U.S. subsidiaries). The Company is cooperating with this investigation. The Company is unable to predict the outcome or reasonably estimate any potential loss; however, we currently believe that this matter will not have a material adverse effect on the Company’s consolidated results of operations, financial position or liquidity.”

SEC Investigations: It seems that the SEC investigation has expanded beyond BUCY goodwill, which we previously discussed in 2013 here, to include the SARL (a non-U.S. subsidiary discussed in earlier SEC correspondences, such as here: http://www.sec.gov/Archives/edgar/data/18230/000001823014000193/filename1.htm)

“On September 12, 2014, the SEC notified the Company that it was conducting an informal investigation relating to Caterpillar SARL and related structures. The SEC asked the Company to preserve relevant documents and, on a voluntary basis, the Company made a presentation to the staff of the SEC on these topics. The Company is cooperating with the SEC regarding this investigation. The Company is unable to predict the outcome or reasonably estimate any potential loss; however, we currently believe that this matter will not have a material adverse effect on the Company’s consolidated results of operations, financial position or liquidity.”

“On September 10, 2014, the SEC issued to Caterpillar a subpoena seeking information concerning the Company’s accounting for the goodwill relating to its acquisition of Bucyrus International Inc. in 2011 and related matters. The Company is cooperating with the SEC regarding this subpoena and its ongoing investigation. The Company is unable to predict the outcome or reasonably estimate any potential loss; however, we currently believe that this matter will not have a material adverse effect on the Company's consolidated results of operations, financial position or liquidity.”

IRS Tax Issue, SARL A ~$1 Billion Ask: There is new tax language in many places in the 10-K. After not much disclosure on the SARL issues in the 10-Q, the 10-K expands on prior disclosure and an earlier correspondence with the S.E.C. here: http://www.sec.gov/Archives/edgar/data/18230/000001823014000193/filename1.htm. It would also seem that there would be substantially more exposure for the period after 2009 if CAT fails in its challenge. This seems likely to linger, since these processes are typically slow.

“On January 30, 2015, we received a Revenue Agent's Report (RAR) from the Internal Revenue Service (IRS) indicating the end of the field examination of our U.S. tax returns for 2007 to 2009 including the impact of a loss carryback to 2005. The RAR proposed tax increases and penalties for these years of approximately $1 billion primarily related to two significant areas that we intend to vigorously contest through the IRS Appeals process. In the first area, the IRS has proposed to tax in the United States profits earned from certain parts transactions by one of our non-U.S. subsidiaries, Caterpillar SARL (CSARL), based on the IRS examination team’s application of the “substance-over-form” or “assignment-of-income” judicial doctrines. We believe that the relevant transactions complied with applicable tax laws and did not violate judicial doctrines. We have filed U.S. tax returns on this same basis for years after 2009. In the second area, the IRS disallowed approximately $125 million of foreign tax credits that arose as a result of certain financings unrelated to CSARL. Based on the information currently available, we do not anticipate a significant increase or decrease to our recognized tax benefits for these matters within the next 12 months. We currently believe the ultimate disposition of these matters will not have a material adverse effect on our consolidated financial position, liquidity or results of operations. We expect the IRS field examination of our U.S. tax returns for 2010 to 2012 to begin in 2015. In our major non-U.S. jurisdictions, tax years are typically subject to examination for three to eight years.”

Progress Rail: Update on that subpoena. It sounds like they are planning to pay their way out.

“On October 24, 2013, Progress Rail received a grand jury subpoena from the U.S. District Court for the Central District of California. The subpoena requests documents and information from Progress Rail, United Industries Corporation, a wholly-owned subsidiary of Progress Rail, and Caterpillar Inc. relating to allegations that Progress Rail conducted improper or unnecessary railcar inspections and repairs and improperly disposed of parts, equipment, tools and other items. In connection with this subpoena, Progress Rail was informed by the U.S. Attorney for the Central District of California that it is a target of a criminal investigation into potential violations of environmental laws and alleged improper business practices. The Company is cooperating with the authorities and is currently in discussions regarding a potential resolution of the matter. Although the Company believes a loss is probable, we currently believe that this matter will not have a material adverse effect on the Company's consolidated results of operations, financial position or liquidity.”

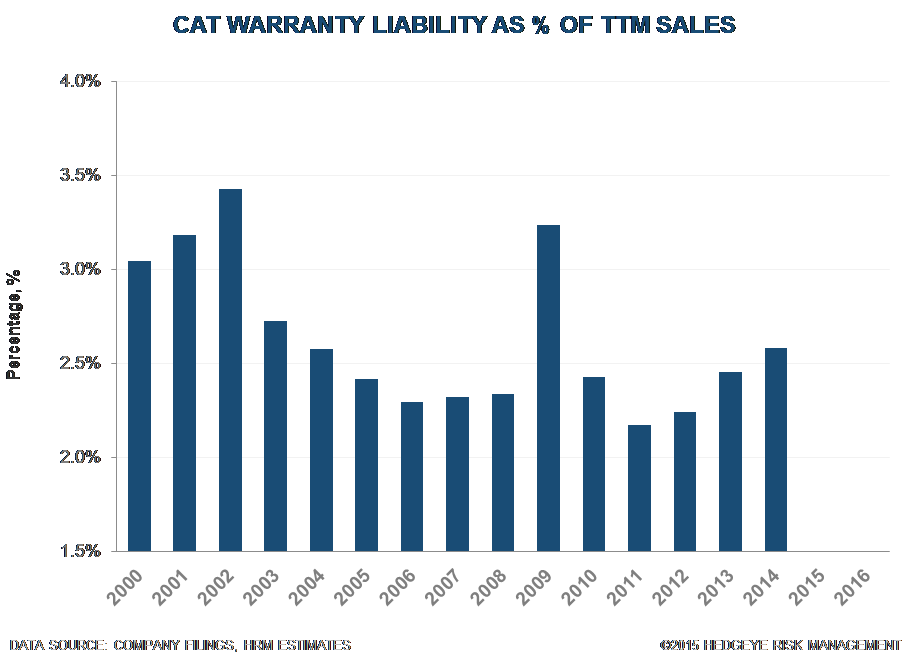

Pre-Existing Warranty Adjustment: Warranty reserve increased despite lower sales. It was apparently due to issues with prior period warranties, which is not usually a positive disclosure, as we see it. In such situations, prior earnings were likely too high because of artificially low accruals, and it is difficult to tell if the further adjustments will be needed.

“The increase in liability includes approximately $170 million for changes in estimates for pre-existing warranties due to higher than expected actual warranty claim experience.”

Change In Residual Value Definition? This looks like a change in definition for the calculation of residual values. The elimination of the word ‘careful’ seems odd, too. If so, it might point to possible issues at CAT Financial. For instance, have used mining equipment values deteriorated? Of course, CAT Financial has already stated that “we have also concluded that our disclosure controls and procedures were not effective as of December 31, 2013” in its revised 10-K after 3Q 2014.

CAT Financial Controls Still Not Effective: Of course, CAT Financial has already stated that “we have also concluded that our disclosure controls and procedures were not effective as of December 31, 2013” in its revised 10-K after 3Q 2014. Its only half of the balance sheet.

“…we are still in the process of implementing and testing these processes and procedures and additional time is required to complete implementation and to assess and ensure the sustainability of these procedures and we have therefore concluded that our internal controls over financial reporting and our disclosure controls and procedures were not effective as of December 31, 2014.” And: “the material weakness relating to our Allowance for credit losses still exists as of December 31, 2014”

Allowances Still Low? While they may lack effective controls, as well as some interesting counterparties in mining/oil & gas, he allowance for losses remains low by historical standards.

Other Notable Items:

Japan Dealer: “While the large majority of our worldwide dealers are independently owned and operated, we own and operate a dealership in Japan: that covers approximately 85% of the Japanese market: Nippon Caterpillar Division. We are currently operating this Japanese dealer directly and its results are reported in the All Other operating segments. There are also three independent dealers in the Southern Region of Japan.”

Odd to Delete This Language: “We build and maintain a productive, motivated workforce by striving to treat all employees fairly and equitably” appears in last year’s 10-K, but was removed for 2014.

Restructuring Costs Identification Helped Construction Industries? We wonder if some of the improved performance at CI was related to ‘aggressive’ restructuring cost identification? $227 of CI’s costs were in 1H, when the segment posted the strongest adjusted margins.

Finished with BUCY Distributorships Divestitures: The BUCY distributorship divestitures are somewhat unusual since dealers are closely tied to CAT, and CAT has often provided deal financing to dealers. Apparently, they are largely complete.

Upshot: As though CAT didn't have enough business challenges, regulatory, financial, and legal issues should provide significant additional distraction. Management has dug themselves a hole, getting paid quite well for the shoveling...