Today we are waking up to another round in the “dollar credibility crisis.” Pressuring the dollar overnight were comments from Federal Reserve Vice Chairman Donald Kohn, who said yesterday the U.S. economy would not snap back quickly from its deep recession, fueling expectations for continued low interest rates for an “extended period” of time. Extended is, obviously, a duration with no defined end point, so no surprise that the dollar bears are licking their lips this morning

On Tuesday, the S&P 500 closed at 1,073, down 0.3% on the day. The six day winning streak for the S&P 500 comes to an end on accelerating volume. The streak came to an end due to (1) a more cautious view on the banks and brokers from Meredith Whitney, (2) the passage of healthcare reform and the pressure in managed care stocks and (3) disappointing earnings from JNJ, DPZ and JCI.

Yesterday’s portfolio activity included buying the Utilities (XLU). Yesterday, we bought the low beta XLU with a reasonable dividend yield into lower prices associated with the morning's market correction. We also covered our short in DRI.

The Technology (XLK) sector was the second best performing sector yesterday. The XLK is the center of M&A activity as CSCO announced its second multi-billion dollar acquisition this month. CSCO agreed to purchase STAR for $2.9B. After the close last night INTC reported good numbers and is the primary driver of the early indication of a higher open for the S&P 500. As Rebecca Runkle noted in her earnings review note last night, INTC has over $14BN in cash on its balance sheet. Given the high cash levels on balance sheets of technology companies, we should expect sustained and accelerating M&A levels in the technology sector.

In addition to INTC, the other earning report of note is from J.P. Morgan, which printed a monster EPS number, at least versus expectations. EPS came in at $0.82, which is up dramatically from the year ago quarter of $0.09, and well above consensus estimates of $0.51. The top line was almost $3BN ahead of expectations as well, primarily driven by fixed income. The bulls, of course, will probably look past the fact this morning that J.P. Morgan added almost $2BN to consumer credit reserves, which brings the company wide total to $31.5BN, or 5.3% of total loans. Loan reserves accelerating is not a good thing, even if irrelevant this morning.

Yesterday, the dollar index was down 0.2% on the day. In early trading overseas, the dollar index is hitting a 14 month low; trading as low as 75.49. The dollar fell after Federal Reserve Vice Chairman Donald Kohn said interest rates will remain low for an “extended period” of time. The VIX declined slightly on the day (0.1%) and is now down 10% over the past week.

Five of the nine sectors in the S&P 500 were up on the day, despite the S&P 500 declining 0.3%. The three best performing sectors were Materials (XLB), Technology (XLK) and Consumer Discretionary (XLY), while Utilities (XLU), Healthcare (XLV) and Financials (XLF) were the bottom three. We are currently long the XLV.

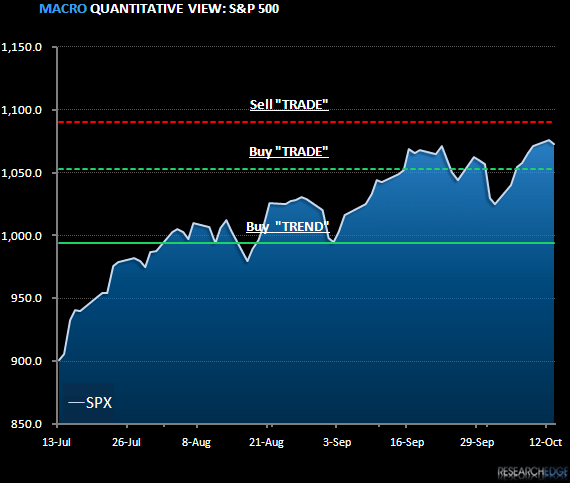

Today, the set up for the S&P 500 is: TRADE (1,053) and TREND is positive (994). Day 3 of perfection - the Research Edge quantitative models have 9 of 9 sectors in the S&P500 positive on TREND and 9 of 9 sectors are positive from the TRADE duration.

The Research Edge Quant models have 1.5% upside and 2% downside in the S&P 500. At the time of writing the S&P 500 is trading +13.00 to fair value; the NASDAQ is trading +22.50 and the Dow Jones is trading +108.00 to fair value. The futures have been accelerating post the J.P. Morgan earnings report.

Howard Penney

Managing Director