EVENTS TO WATCH

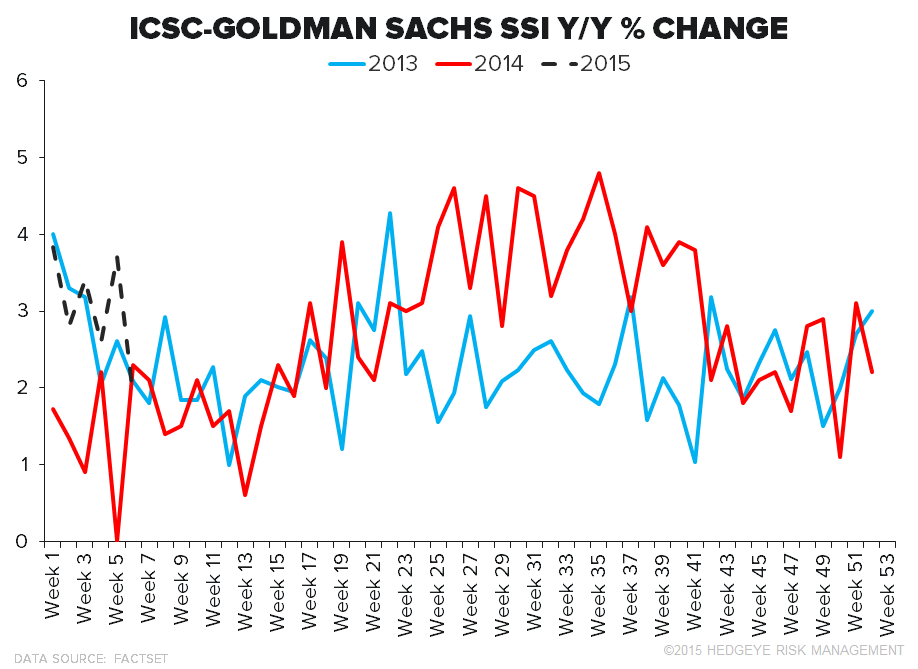

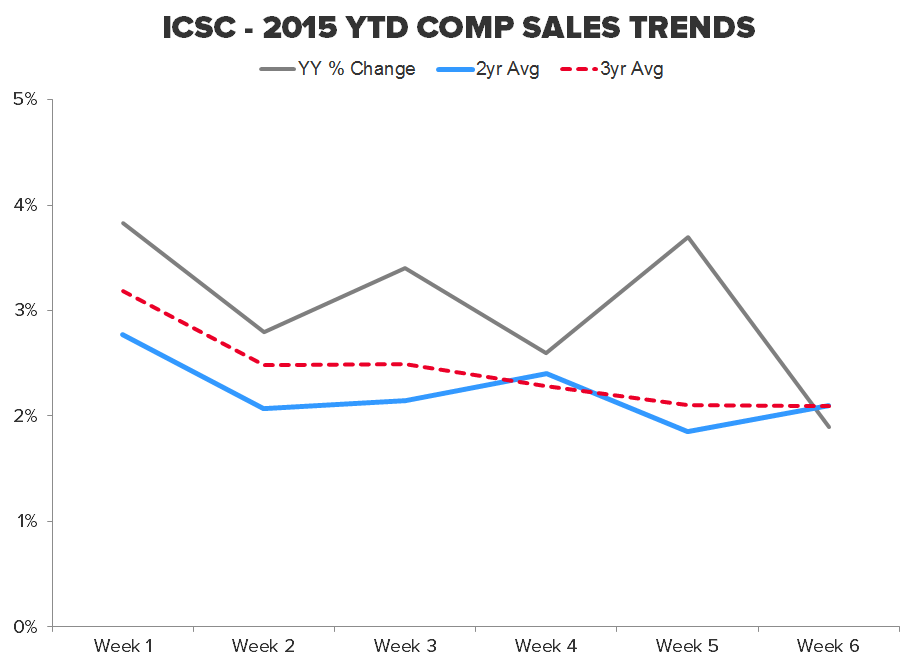

ICSC RETAIL SALES (80 General Merchandise Stores)

Takeaway: Going against the toughest comp in calendar Q1 the 1 year decelerated 180bps sequentially, with a 25bp pop in the 2yr. Not spectacular, but respectable. The trend we're most focused on here is 3yr trend which eliminates all noise. It's decelerated in all but one week this year.

COMPANY HIGHLIGHTS

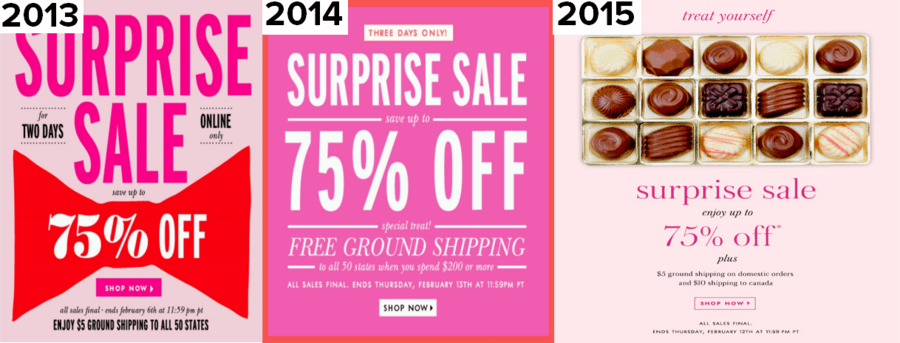

KATE - Flash Sale Promotions

Takeaway: We track the promotional cadence for about 100 retailers by keeping account of the promotional emails. There are a few variables that we will admit are hard to account for, specifically the volume and depth behind each campaign. But, comparing the YY change in the direct business we think is the most efficient way.

There was a lot of noise surrounding the promotional posture of the handbag industry to start the year -- it eroded $710mm in market cap for KATE over a 15 day period. We dug into KATE's promotional cadence and came back extremely positive, which was proven true when the company pre-announced on 1/29. Opening the inbox this morning, we were hit with KATE's first 'Flash Sale' of the year, so we went back to the archives to see if the sales matched the prior years' offerings. And the results were exact down the to the calendar days and % off (pictures and details below). KATE is slowly pulling back the 'Flash Sale' concept to promote full price sales in its direct channel. It's held true to its stance to date - we'd point to the exclusion of a 'Flash Sale' in December of 2014, which Management discussed in August, as proof. Though we question the effect it will have on comps. In year one of this new posture, the company just reported a 26% comp.

- 2013 - 2 day sale 2/5 - 2/6, 75% off

- 2014 - 3 day sale 2/11 - 2/13, 75% off

- 2015 - 3 day sale 2/10 - 2/12, 75% off

OTHER NEWS

TGT - Target and landlords in court battle over sale of leases

FINL - Imran Jooma Joins Finish Line as Chief Omnichannel Officer, Executive Vice President

(http://phx.corporate-ir.net/phoenix.zhtml?c=81647&p=irol-newsArticle&ID=2014905)

West Coast port congestion could cost retailers $7 billion this year

(http://www.chainstoreage.com/article/west-coast-port-congestion-could-cost-retailers-7-billion-year)

EXPR, UA - Express Signs NBA All-Star Stephen Curry

New Look chief says retailer ready for IPO

(http://www.ft.com/intl/cms/s/0/2134845c-b0f6-11e4-94feab7de.html?siteedition=intl#axzz3RLNwI3nj)

BOSS - Permira Pares Hugo Boss Stake

ARO - Aeropostale, Inc. Announces Executive Appointments

(http://phx.corporate-ir.net/phoenix.zhtml?c=131103&p=irol-newsArticle&ID=2014924)

BABA - Alibaba Urged to Step Up Action on Fakes

Pam & Gela to Launch E-Commerce