KEY POINTS

- DIRTY, DIRTY, POOL: YELP will be pulling its Active Local Business Account metric in favor of a new one focusing only on businesses contributing to its Local Advertising Revenue. The customer repeat rate and reported account base will now be an apples-to-oranges comparison. There is no other reason to do this other than to mask its rampant attrition issues.

- SHOT ITSELF IN THE FOOT: Management needed to rebase expectations, but chose to guide inline with lofty consensus estimates instead. What’s interesting is that YELP thinks it can somehow hit numbers while scaling down the rate of sales rep hiring...when its sales rep productivity is currently on the decline.

- WHAT HAPPENS FROM HERE: Revenue guidance is back-weighted, and consensus is going to raise the bar further. The first time that YELP doesn’t raise guidance, the stock craters. That likely comes on the 2Q14 release (3Q14 guidance).

DIRTY, DIRTY, POOL

YELP beat 4Q14 top-line estimates by ~1%, but we’re not sure if/how much its two international acquisitions contributed. Net account growth slowed to 44% (ex Qype account transition) from 51% in the prior. The slowdown was largely due to a sharp deceleration in new account growth to 30% from 40% in the prior quarter (also ex Qype). YELP’s attrition rate improved to 18.5% from 19.1% in the prior quarter, but absolute attrition accelerated as it has for every quarter for as long as we can track the data.

The major red flag from the quarter was that YELP will be pulling its Active Local Business Account metric in favor of a new one focusing only on accounts contributing to its Local Advertising Revenue. The customer repeat rate and its reported account base going forward will now be an apples-to-oranges comparison. There is no other reason to do this other than to mask its rampant attrition issues. Management is trying to buy some deniability to our attrition thesis, but skewing the numbers doesn't change anything.

SHOOTING itself IN THE FOOT

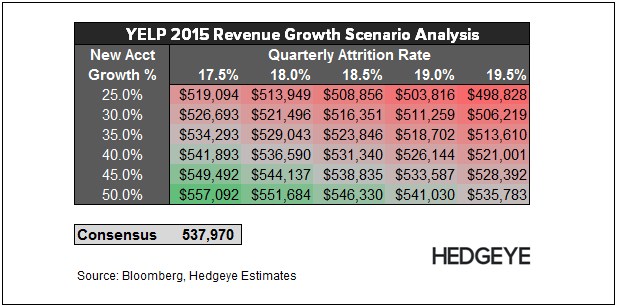

We expected YELP to guide light; our mistake was thinking management would approach guidance rationally. Instead management basically guided inline to estimates that we estimate are well out of reach. We have stated repeatedly that YELP will need to produce both accelerating new account growth and record low attrition to hit consensus estimates. For perspective, YELP averaged 34% new account growth (y/y%) and 18.5% quarterly attrition in 2014.

The risk to our thesis, at least in 2015, was that YELP was going to accelerate its sales rep hiring in 2015 to stuff the channel as much as possible. Instead, YELP plans to slow the pace of sales rep hiring to a rate of 40% y/y in 2014 (vs. an average growth rate of 53% in 2014

Remember, YELP’s business model is predicated on aggressive sales rep hiring to drive enough new account growth to offset its rampant attrition. So by choosing to scale down hiring when it can't produce new account growth in excess of its sales rep hiring is a suspect move.

WHAT HAPPENS FROM HERE?

1Q15 revenue guidance is roughly 20% of its 2015 revenue guidance, which essentially means guidance is back-weighted. Consensus will likely raise the bar further to reflect the marginal upside to guidance, and may do so again following the 1Q print if YELP produces some upside on the heels of its international acquisitions and/or the YP partnership.

But remember that YELP must consistently beat and raise to sustain its multiple. The first time that YELP doesn’t raise guidance, the stock craters. That likely comes on the 2Q14 release (3Q14 guidance).

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet