Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email

------

Key Takeaway:

The ECB’s asset purchase high was short-lived as global markets resumed their decline shortly after the news. The collapse in energy prices continues to destabilize select economies raising the specter of a financial crisis. We watch closely both TED Spread and Euribor-OIS for indications of rising global systemic risk in the banking system both at home and in Europe. TED Spread has quietly crept up to 25 bps from 21 bps a month ago, but that magnitude of change is not especially noteworthy. Meanwhile, Euribor-OIS is essentially unchanged.

Belgium cut rates, Russia cut rates, and the ECB is buying bonds. Global central banks are trying to stimulate growth, but markets are falling. Perhaps investors have built up a tolerance to central bank drugs. As that seemed to be the case last week, short-term risk measures in our heat map below came out mostly in the red.

European Financial CDS- Swaps widened across the board in Europe last week. Greek spreads blew out following Syriza’s election victory. Syriza’s win again raises concerns around austerity/Grexit. Concerns that Spain could follow a similar electoral path pushed out spreads for most Spanish banks. Russia's Sberbank saw its spreads widen by a further 67 bps after the Bank of Russia unexpectedly cut interest rates on fears of an impending recession. This conflicts with six rate increases over the past year as the central bank is stuck between a rock and a hard place. This past week, Russia’s rate policy shifted from fighting inflation and supporting the Ruble to stimulating economic activity.

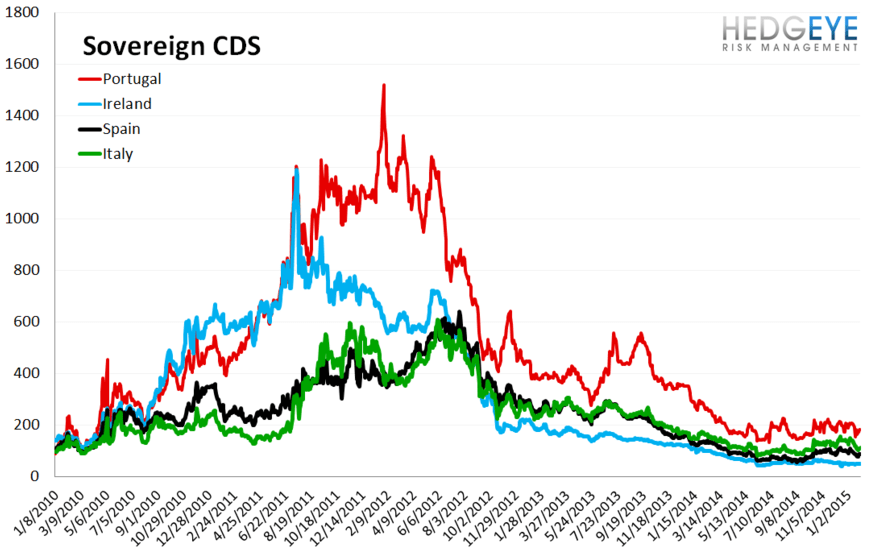

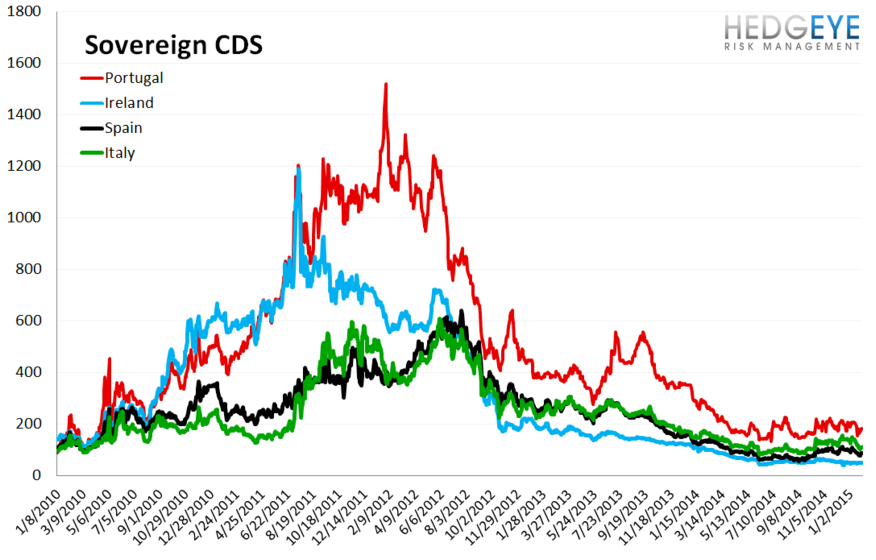

Sovereign CDS – Sovereign swaps were mostly wider last week as global markets fell amid waning enthusiasm over ECB asset purchases. French sovereign swaps tightened by -6.9% (-4 bps to 47 ) while Spanish sovereign swaps widened by 13.1% (10 bps to 87).

Euribor-OIS Spread– The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 9 bps.

Matthew Hedrick

Associate

Ben Ryan

Analyst