This note was originally published at 8am on January 14, 2015 for Hedgeye subscribers.

“Creative minds tend to make unusual associations because they engage in divergent thinking.”

-J.P. Guilford

Joy Paul Guilford was one of the first credible American researchers in the field of creative thinking. He was a psychologist (born in Nebraska in 1897, moved to LA – died 1987) “best remembered for his psychometric study of human intelligence, including the distinction between convergent and divergent production.” (Wikipedia)

Is your portfolio converging or diverging from consensus? When you diverge from the crowd, are you typically early – or happy to be late? Irrespective of your answers to those questions, isn’t the idea of a diversified portfolio to have creative ideas that are all of the above? After all, it’s always nice to have something working!

Today is Ratification Day in the USA (Treaty of Paris officially ended the American Revolution vs. European Central Planners). I love ratifying the end of broken ways. And, even if all of European markets (and US markets reacting to them) only trade on the next central planning rumor today, I’ll always love the divergent thinking that’s been embedded in American independence.

Back to the Global Macro Grind…

Yep, it’s all about the love this morning. I said it on the Q1 Macro Themes Call and I’ll say it again this morning – I absolutely love this market. The Global Macro long/short market of non-consensus ideas, that is!

Here’s a not so creative idea. Asset price #bubbles can pop.

The US stock market #bubble has been down for 8 of the last 10 trading days, and plenty of the #bubbles within the bubble (think social media, MLP, energy, TSLA in 2020, etc. stocks) continue to pop.

But, there’s always a bull case to be made somewhere. And, compliments of Hedgeye, asset price #deflation becomes the creative asset of the new buyer, from lower prices. We need to cross the #Quad4 #Deflation bridge before we get to #Quad1.

Are you with us and bullish on #Housing? Yesterday’s macro market action typified the opportunity that is being Creatively #Patient. US equity futures were green in the a.m., then ramped on news from a US homebuilder that they had a good quarter (KBH). Then:

- KB Homes (KBH) told the Old Wall that they still have margin pressure associated with what was a bad trailing 12 months

- Oh, and that they do a lot of business in the state of Texas

- KBH went from being up nicely to -18% on the day (so we #timestamped buy there in Real-Time Alerts, #patience)

Texas? Jobs correlated to asset price #deflation of West Texas Crude? Pardon?

Yeah, really creative thought path there guys. If you didn’t know that #Deflation’s Dominoes go like this: Yens and Euros burned by central planners à Strong USD vs Yens and Euros à Crashing Oil à Shaking High Yield Debt Markets (spread risk breakout) à Levered Energy (MLP) stocks smoked à Job losses in Texas, the Dakotas, etc…

Well, I guess now you know.

So join my boy, Mr. T (as in TLT Long Bond) in commemorating another fresh new 12 month high in the best way to play global #GrowthSlowing + #Deflation. Because lower-bond yields are discounting a peak in late-cycle job adds in a late-cycle economic indicator’s (inflation) Energy states.

What other wild and creative thought path can we come up with in lieu of the aforementioned causal factor embedded in crashing long-term bond yields (10yr started 2015 at 2.17% don’t forget)?

- Down Long-term Treasury Yields

- Compressing Yield Spread (long-end minus short-rates)

- Short the Financials?

Unless you’re still thinking it’s different this time, Financials are cyclicals too. And a core driver of bank earnings is called NIM (net interest margin) which is driven by the spread between the short and long-end of the Treasury curve.

Not to pick on people who got plugged chasing another US equity market top on December 29th, but that was a seminal day for we revolutionaries who refused to buy into the year-end CNBC hype.

At the close of US trading on December 29th:

- SP500 = all time high of 2090 (it has corrected -3.2% from there)

- Big Cap Financials (XLF) = $25.04 close (correction = -4.7% from there)

- Regional Banks (KRE) = $41.18 close (correction = -8.9% from there)

Again, I know. If all you do is talk about the SP500 (which you can’t charge an active manager premium fee for):

A) At -3.2%, it hasn’t corrected that much – and, by the way, there have been great early-cycle and consumption sectors to be long (after they deflate) on oversold signals within the SP500 too

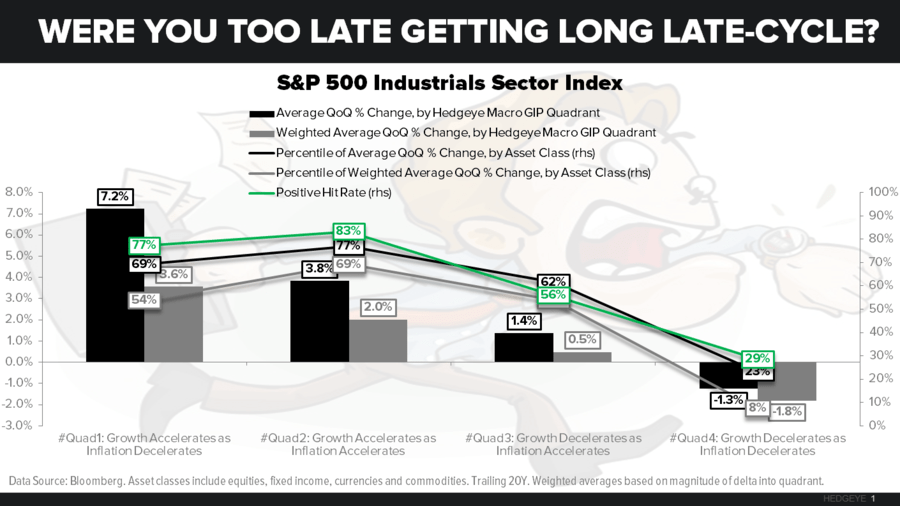

B) But the mistakes associated with buying either late-cycle Industrials (think global demand), #deflation risk sectors (energy), and US Regional Banks have been severe

It’s early in the year, and my job is to help make sure you don’t underperform. The best way to do that is to think a little more creatively than the next fund manager, and be a lot more #patient.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.85-2.01%

SPX 1995-2044

FTSE 6332-6580

VIX 17.45-21.99

WTI Oil 44.01-49.03

Copper 2.43-2.65

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer