* * * * * * *

Editor's note: This is a brief excerpt from Hedgeye CEO Keith McCullough's Morning Newsletter.

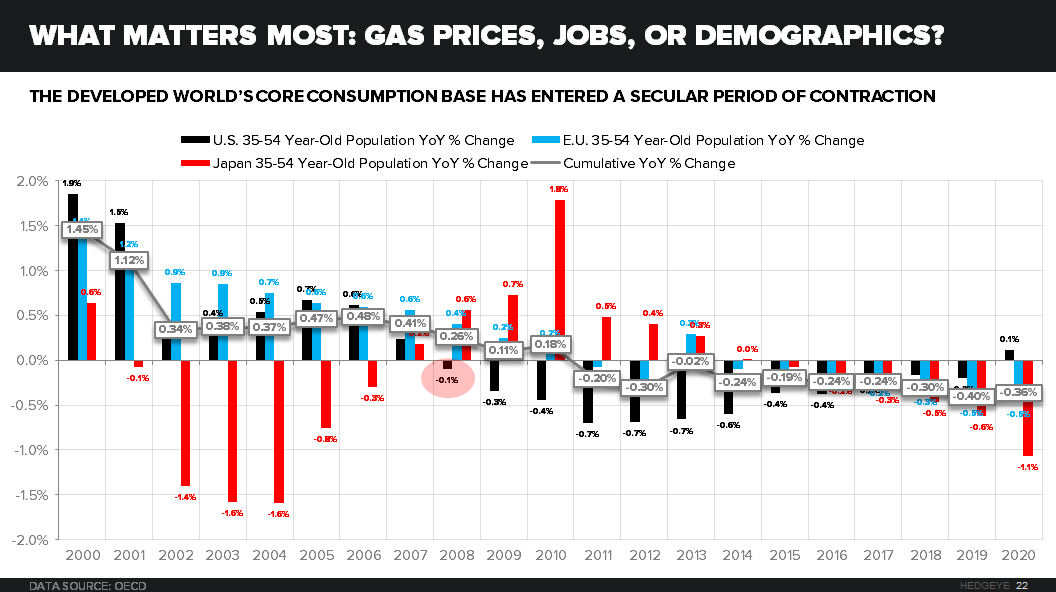

Interestingly, but not surprisingly, Life-Cycle Economics was one of the most talked about macro topics when Darius Dale and I were on the road seeing Institutional Investors in NYC last week where I’d ask everyone the question we have on slide 22 of our Q1 Macro Themes Deck: “What Matters Most: Gas Prices, Jobs, or Demographics?”

While many like to call themselves “long-term investors”, when it comes to answering the question in our Chart of The Day thoroughly, I think you should call yourselves multi-duration, multi-factor, risk managers. That’s my new marketing pitch!

Here’s one way to think about all 3 factors, across durations:

- GAS PRICES – immediate-to-intermediate-term (bullish TRADE and TREND duration impact to consumers)

- JOBS – intermediate-term (making a bearish turn? The cycle tends to be less lumpy and cyclical, or TRENDING)

- DEMOGRAPHICS – long-term (what was a long-term tailwind in the USA, Japan, and Europe is now a headwind)