We first laid out our bearish thesis on a conference call back in September 2014. Let us know if you’d like a copy of the slide deck.

This note is accompanied by an updated, condensed slide deck that visually runs through the bear case. CLICK HERE for access. We encourage you to read the note prior to running through the deck.

Point #1: ‘Big Bets’ Carry Risk

As we see it, the “biggest bet” the company is making is on its food strategy and the implications for overall performance of breakfast and lunch. SBUX is investing a substantial amount of time and effort into building food sales, without the benefit of having equipment or a process that allows them to produce the food fresh. Food is the biggest risk to the DNA of the company because, in our view, it will never be on-par with the quality of beverages consumers have come to expect from Starbucks. Handcrafted beverages and food served wrapped in plastic are not complimentary. It’s also difficult to imagine that other QSRs and fast casual restaurants will idly sit by and let SBUX scoop up incremental market share.

Point #2: Signs of Domestic Maturation

There’s no two ways about it. The business is steadily decelerating in the U.S. Two-year average same-store sales have decelerated 250 bps from the recent highs of 4Q11. Even more concerning, two-year average traffic has decelerated 300 bps from the recent highs of 3Q13 and, last quarter, was up a measly +1%. The recent composition of comps has been weak, yet the street expects the company to produce 5%+ comps throughout 2015. If comps come in below cheery estimates, Starbucks will not hit its earnings numbers.

Point #3: Menu Proliferation Rearing Its Ugly Head

Our short call argues that the proliferation of new menu items is in fact slowing service times and traffic trends. Management was hard pressed on this issue on the 4Q14 earnings call and was in complete denial about the possibility of a throughput issue. In fact, they attributed the entire slowdown to the macro environment and a shift in consumer shopping patterns.

Point #4: CAP & EMEA Are Irrelevant

We often hear pushback from bulls that Starbucks has an enormous growth opportunity in CAP and that EMEA has turned the corner. Look, we get it – the company has plenty of international expansion ahead. But, the fact of the matter is, this is irrelevant to the business today. EMEA only contributed ~3% to operating profits in Fiscal 2014. CAP, where same-store sales and traffic trends have been in freefall, only contributed ~10%. This business, for now, is about the U.S. – a market which is undoubtedly showing signs of maturation.

Point #5: Japan Acquisition Reeked Of Desperation

Shortly following our bearish conference call back in September 2014, Starbucks announced its intentions to acquire the remaining 60.5% share of Starbucks Japan in a two-step tender offer process that should be fully completed in the first half of this year. To be frank, this acquisition makes strategic sense over the long-term as it will allow the company to capture the significant growth opportunity left in that region. It’s a large market for Starbucks ($1.2 billion in revenues), boasts high store-level profit margins (20-25%), and should be immediately accretive to EPS.

The timing of the deal, however, is what really raised some eyebrows. In our view, this transaction was completed, at this specific point in time, in attempt to mask a slowing core business. The company could've done this deal at any time in the past three years, but did not need to given strong sales trends and a significant commodity tailwind. With these trends reversing, expectations for 17% EPS growth in FY15 still look aggressive, despite the transaction.

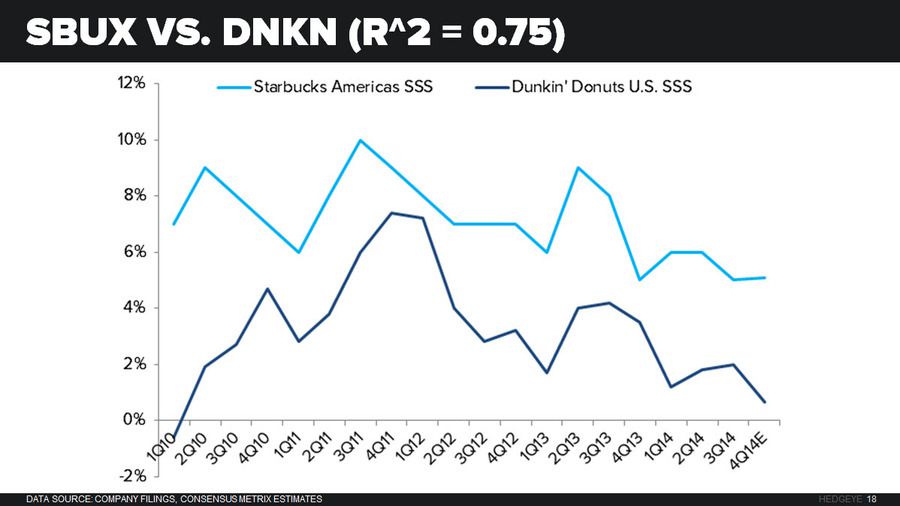

Point #6: DNKN Debacle & Parallels

Mid-December, Dunkin’ guided to disappointing full-year 2014 comps of +1.4%, below the +1.8% consensus estimate. The read-through was quite discouraging, as it implied 4Q comps in the range of +0.5-0.8%, well below the +2.2% consensus estimate. The company also guided down full-year 2015 EPS by $0.11-0.14 to $1.88-1.91. This made us consider whether or not Starbucks is seeing similar pressure in their business.

While it pains many people to compare Starbucks to Dunkin’ Donuts, the reality is that the correlation between the two company’s same-store sales is an alarming 0.75 since the beginning of calendar 2011. It’s difficult for us to sit here and pretend Starbucks is fully immune to the softness Dunkin’ is facing.

Point #7: Hyped Up Holiday Season

Let’s face it – Starbucks 4Q14 print was not a pretty one, resulting in multiple downward revisions in 2015 EPS estimates. Despite this, it’s been clear to us that the street has given management “a pass,” for now, opting instead to wager that holiday promotions and “Starbucks for Life” will drive accelerated traffic in 1Q15. If there’s one thing we’ve learned over the years, it’s that the holiday season is almost always overhyped – and, this year, we’re not buying it.

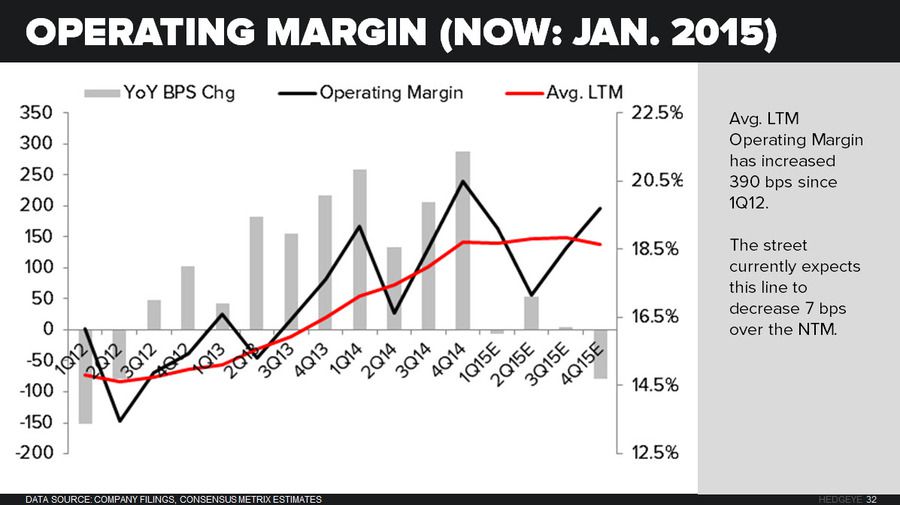

Point #8: Operating Leverage Is Gone

The core of our thesis is playing out exactly as expected. This is a business model that is completely lacking incremental leverage. If sales and traffic continue to surprise to the downside, Starbucks will continue to miss its numbers. Management is currently struggling to find additional leverage in the model in order to offset a reversing sales trends and a commodity headwind. Efforts to pull labor from stores come with the massive risk of exacerbating recent comp and traffic deceleration. With the cadence of comps already weak (fueled by unsustainable average check growth), management has suddenly found itself between a rock and a hard place.

Point #9: Sentiment Is Shifting

We’ve been the lone bear on Starbucks since our initial call back in September. Even with the overwhelmingly majority of the street bullish (80.6% Buys; 1.62% Short Interest), we feel the tide is slowly turning. In fact, last week a competitor downgraded the stock to Neutral in a note which cited multiple factors, including concerns about near-term comp trends. Analysts are hesitant to take on an unfavorable view of the restaurant industry’s darling, and we get that, but the good news is sentiment can only get worse from here.

Point #10: Fundamental Disconnect

While our thesis is playing out to a tee, the stock has yet to move in our favor. Consider this: since the end of October, FY15 EPS estimates have been revised down by $0.04 while the stock has traded up nearly 7% to $81.18 per share. While these aren’t substantial moves on either account, they are notable – and they certainly shouldn’t be ignored. If comps come in below the street’s estimates at all in 2015, there will almost certainly be another leg down in the red line below.