Editor's note: This is a brief excerpt from Hedgeye morning research. For more information on how you can become a subscriber click here.

* * * * * * *

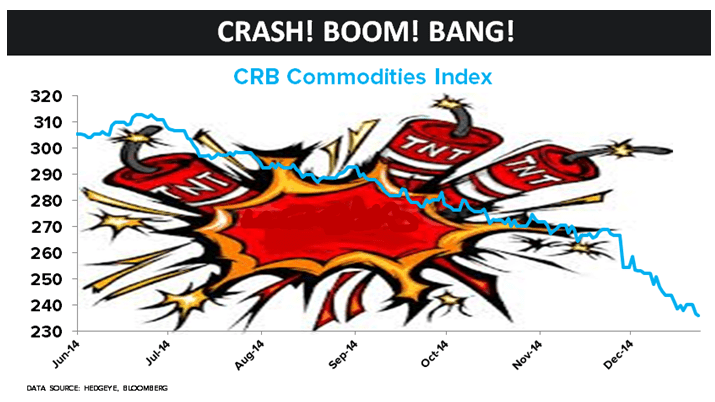

Collapse, crash – use whatever word you want to describe a CRB Index (19 commodities) that dropped another -1.4% to fresh year-to-date lows yesterday.

For those of you keeping score, it’s down -25% since June.

While it’s fascinating to hear a wide range of narratives on why, the reality is that being positioned for #deflation risk (net short Commodities, Junk Bonds, etc.) is paying off big time now.