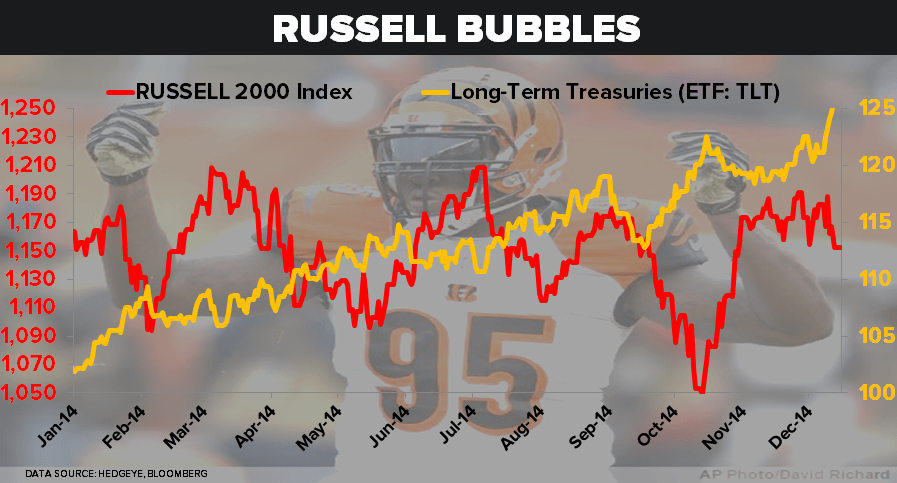

"After doing absolutely nothing for the 6 weeks prior, our least preferred 2014 player on the US Equity market field (Russell 2000), dropped -2.5% last week to -1.0% YTD ... [Meanwhile] UST 10yr Yield -22 basis points on the week to 2.08% (that’s a -31.3% crash in bond yields for 2014 YTD) ... Our favorite player, TLT (20yr Treasury Bond ETF) was up another +2.9% last week to +24% YTD."

This is an excerpt from today's Morning Newsletter by Hedgeye CEO Keith McCullough.