"I can't hear you. There's too much money in my hand."

-Johnny Manziel

Whether former Texas A&M superstar Johnny Manziel said it that way (or with more expletives!) isn’t the point. If you’re a rookie and you’re going to give an entire profession the money signal like that, you better deliver on game day!

In what was an embarrassing professional start, Manziel did not deliver the moneys for Cleveland yesterday – and the Cincinnati Bengals veteran defense proceeded to spend the afternoon giving little Johnny some signals of their own.

Sort of like what the US Treasury Bond market did to the momentum chasing US equity bulls last week…

Back to the Global Macro Grind …

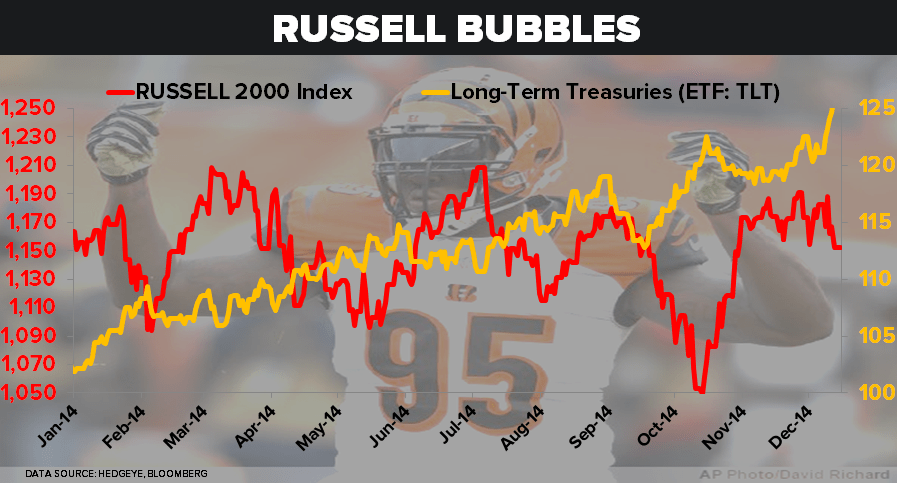

After doing absolutely nothing for the 6 weeks prior, our least preferred 2014 player on the US Equity market field (Russell 2000), dropped -2.5% last week to -1.0% YTD. With only 2.5 weeks left in the season, that is not a Money Man bull market!

What was interesting about the Russell #Bubble’s drop (topped 5% higher on July 7th, 2014) was that it actually outperformed the almighty navel gazer on the week. The Dow Jones Industrial Index lost 50% of its 2014 gains, closing -3.8% to +4.2% YTD.

All the while, Global Equities continued to look like Manziel:

1. European Equities (EuroStoxx600) dropped -5.8% on the week to +0.7% YTD

2. Emerging Market Equities (MSCI) #deflated another -4.0% wk-over-wk to -5.6%

3. Latin American Equities moved closer to #crash mode, -6% on the week to -16.1% YTD

I know, cheery picking more than a few interceptions to make the game replay tapes look bad isn’t such a nice thing to do during the holiday season – but, to be clear, unless you are long bonds, there hasn’t been much to celebrate in December.

Bonds?

Yep. As the Barron’s Top Strategist 2015 Outlook reiterates its consensus 2014 outlook (GDP accelerating and #RatesRising, which btw was our 2013 outlook), we reiterate both growth and inflation slowing (and lower bond yields).

As US Equity Volatility (front month VIX) rocketed +78.3% last week, the low-volatility ramp in the Long Bond continued:

1. UST 10yr Yield -22 basis points on the week to 2.08% (that’s a -31.3% crash in bond yields for 2014 YTD)

2. UST Yield Spreads compressed to YTD lows (-12bps wk-over-wk and -111bps YTD for the 10s/2s Spread)

For those of you who do Moneyball (or Moneypuck) stats, you’ll respect the reality that A) higher absolute and relative returns + B) lower-volatility in those returns, is where the real money in this game is at...

If you want to think about that in Dow, Russell, or SPY terms vs the Long Bond (TLT and EDV):

1. TLT (20yr Treasury Bond ETF) was up another +2.9% last week to +24% YTD

2. Vanguard’s Extended Duration ETF (EDV) was +3.9% week-over-week to +40.8% YTD

What’s driving this?

1. Falling growth expectations

2. Falling inflation expectations

And while there was a time (earlier this year) where the Old Wall said “bond yields are falling in Europe, not because growth and inflation are slowing, because its different this time”… it’s not.

In rate of change (Hedgeye) terms, when both growth and inflation are slowing, at the same time, the Long Bond investor gets paid.

No, this wasn’t a sexy call. And you won’t see me or my teammates living large on bottle service drinking the chartreuse (Zervos?) or hanging with Roubini either… but it remains the call Consensus Macro still isn’t willing to make.

On that sentiment score, check-out where CFTC (non-commercial) futures and options bets went last week:

1. SP500 (Index + Emini) = +48,911 net LONG position (vs. its 6mth avg of a -21,000 net short)

2. TREASURIES (10yr) = net SHORT position at its YTD high of -214,778 contracts (vs. its 6 mth avg of -38,000 net short)

Yep, I can hear you loud and clear. There’s too much consensus in that hand!

UST 10yr Yield 2.08-2.22%

SPX 1

RUT 1146-1165

VIX 15.47-22.71

YEN 117.06-121.68

WTI Oil 56.48-63.21

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer