“I have long understood that losing always comes with the territory when you wander into the gambling business, just as getting crippled for life is an acceptable risk in the line backer business. They both are extremely violent sports, and pain is part of the bargain. Buy the ticket, take the ride.”

-Hunter S. Thompson

The stock market business isn’t nearly as risky as being a NFL linebacker or, at least in some jurisdictions, being involved in the gambling business. Nonetheless, being a stock market operator does not come without its risks. Ironically, the most significant risk to being invested in the stock market currently is likely mismanaging the actions of central banks.

The most recent and significant action of course comes from the People’s Bank of China (PBOC) which cut the 1-year deposit rate by 25 basis points and 1-year lending rate by 40 basis points. This was China’s first interest rate cut since June 2012. For those that were long Chinese equities, this is a short term positive, but for those that were caught offside, not so much.

Recent history shows rallies related to Chinese rate cuts have been very, very short lived. In fact, six of the past seven cuts to interest rates and reserve requirements have been followed by declines in stock prices over the next two months. Perhaps this is why according to Reuters this morning, “the Chinese leadership and PBoC are ready to cut interest rates again and also loosen lending restriction.”

The longer term challenge with seemingly arbitrary moves in central banking policy is the creation of excesses. As Professor John Taylor from Stanford wrote in a recent paper, the biggest issue with abnormally dovish policy specifically (read: low rates) is the increased appetite for risk. According to Taylor:

“Anther effect of extra low policy rates is on risk aversion. Using time series techniques Bekaert, Hoerova, and Duca (2012) found that this effect is empirically significant. They decompose the VIX into a risk aversion component and an uncertainty component. They then look at the cross autocorrelations between policy rates and these two components. Their empirical results show that “Lax monetary policy [below policy rule rates] increases risk appetite (decreases risk aversion) in the future, with the effect lasting for about two years and starting to be significant after five months.” These results provide a reason why a change in monetary policy might actually shift the tradeoff curve in Figure 2 back up—a channel to poor economic performance which is quite different than the risk aversion channel of Elliot and Baily (2009) or King (2012) and with much different policy implications.”

Net-net, non-rules based and extra low policy rate rates may actually have the unintended consequence of increasing risk and eventual economic underperformance.

Back to the Global Macro Grind…

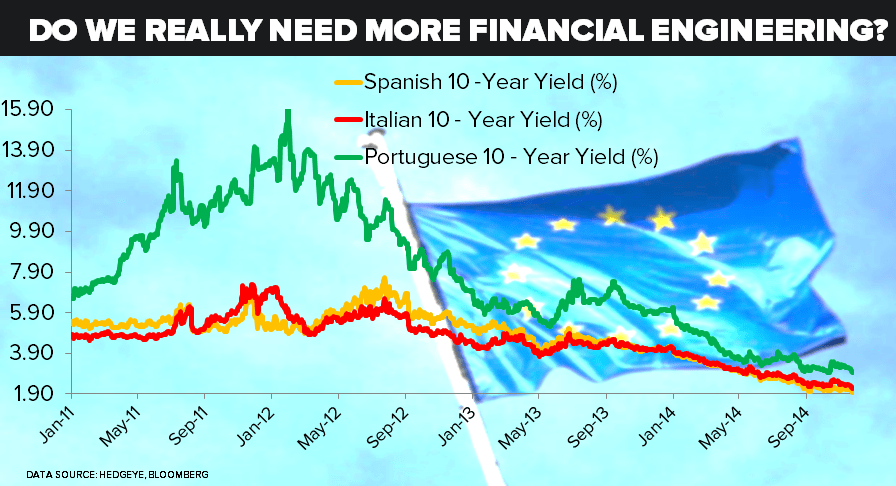

This morning’s monetary policy rumor of the day is that the EU is set to announce a new fund this week that will use “financial engineering” in an effort to create at least €300B of additional investment. The question, of course, is what is the point of more “financial engineering”? In the chart of the day, we take a look at the yields on 10-year sovereign debt for Spain, Italy and Portugal, that highlights that cost of sovereign capital of all three are down meaningfully year-to-date and over the last three years.

Interestingly, at 2.04% and 2.25% for Spain and Italy respectively, their 10-year yields are both lower than the United States. Clearly, then, the government lending market is not the issue, so perhaps a magical €300B in incremental investment in the private sector will be what it takes to lift Europe out of its economic malaise? Perhaps, and maybe Santa Claus does actually exist!

Speaking of unlikely global macro scenarios, how about the scenario that OPEC finally agrees on production targets and sticks to them? Currently, according to reports, OPEC is over producing by about 500 – 600K barrels per day over its 30 million barrel per day target. Already, Libya, Iran, Ecuador, and Venezuela have called on the cartel to cut production, but Saudi Arabia, the key swing producer, has little ability to measure whether other members of the cartel have cut production and the four aforementioned countries are hardly the most transparent.

While OPEC in theory can control supply (although in practice we aren’t so sure), the reality remains that the biggest issue is demand from the world’s largest consumer – the United States. Currently, the U.S.’s oil imports from OPEC are the lowest they have been in 30 years. Specifically, in August, OPEC’s share of U.S. oil imports dropped to 40% versus the 1976 peak of 88%.

With Brent Crude down over -27% in the YTD and WTI down over -22%, it is no surprise that OPEC is a bit rattled. In the long run, this has the potential to be a decent tail wind for the U.S. economy, although in the short run, this quick and decisive move in oil may have some negative derivative impacts.

Currently, the gap between U.S. corporate bonds and Treasuries is at 124 basis points, near the widest level of the year. Conversely, European corporate spreads are near their tightest levels. Not surprisingly, the likely culprit is the price of oil as energy bonds are the largest industry grouping in the high yield market domestically. Speaking of which, if you want any over levered short ideas in the Energy and MLP sector, definitely email us at , because we have a plethora.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.28-2.38%

SPX 2011-2066

RUT 1153-1188

USD 87.45-88.51

EUR/USD 1.23-1.25

WTI Oil 73.90-78.11

Keep our head up and stick on the ice,

Daryl G. Jones

Director of Research