TODAY’S S&P 500 SET-UP – November 18, 2014

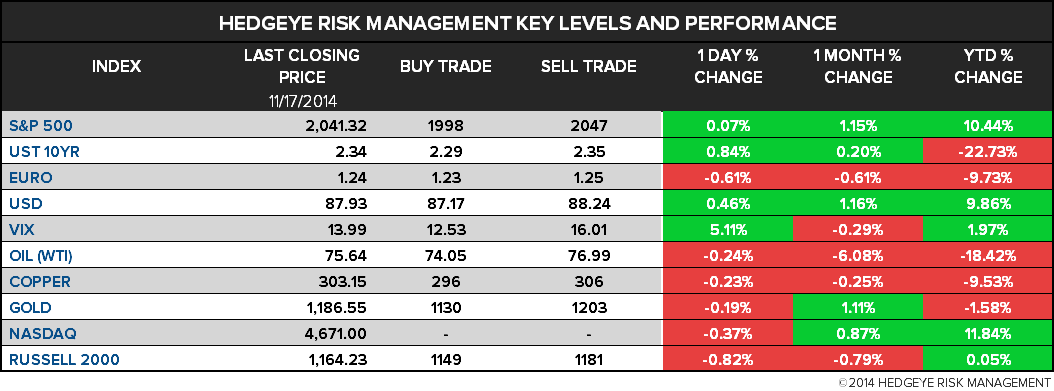

As we look at today's setup for the S&P 500, the range is 49 points or 2.12% downside to 1998 and 0.28% upside to 2047.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.83 from 1.83

- VIX closed at 13.99 1 day percent change of 5.11%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: PPI Final Demand m/m, Oct., est. -0.1% (prior -0.1%)

- 8:55am: Redbook weekly sales

- 10am: NAHB Housing Market Index, Nov., est. 55 (prior 54)

- 11:30am: U.S. to sell 4W bills

- 1:30pm: Fed’s Kocherlakota speaks in St. Paul, Minn.

- 4pm: Net Long-term TIC Flows, Sept. (prior $52.1b)

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- Senate to vote Keystone XL pipeline after House passed bill

- Diplomats from the U.S., U.K., France, Germany, Russia and China convene in Vienna for nuclear talks as they attempt to finalize interim deal with Iran before Nov. 24 deadline

- 10am: Senate Foreign Relations Cmte hearing on countering Islamic State in Iraq and Syria

- 10am: FDIC board holds open meeting to consider final rule on revisions to Deposit Insurance Assessment System

- 10am: House Foreign Affairs subcmte hears from leaders of Doctors Without Borders and Africare on Ebola

- 10am: House Cmte on Transportation and Infrastructure hearing on FAA reauthorization

- 1pm: House Energy and Commerce Cmte hears from CDC Director Tom Frieden on U.S. response to Ebola

- 6:30pm: Sen. Energy and Natural Resources Chairwoman Mary Landrieu holds news conf. on Keystone after Senate votes

WHAT TO WATCH:

- Abe Delays Tax Hike, Calls Vote to Renew Mandate: NHK

- Wall Street to Reap $316m From Actavis, Halliburton Deals

- Sprint CEO Claure Shuffles Top Management in Turnaround Bid

- AT&T Cutting Shared Data Plan by 23% in Pre-Holiday Promotion

- Intel to Merge Loss-Making Mobile Business With PC Division

- Samsung Moves Smartphone Engineers to Internet of Things

- Nokia Rolls Out Android Tablet in Return to Mobile Devices

- Blackstone Said to Sell NYC Tower to Ivanhoe for $2.25b

- SunEdison, TerraForm to Acquire First Wind for $2.4b

- Halliburton Said to Plan $4b in Disposals for Baker Hughes

- Halliburton, Baker Hughes May Be Cut by S&P

- Carnival Enlists Public in Push to Tackle Cruise Image

- China Rejection of HK Stock Icons Evident in Lopsided Link

EARNINGS:

- Dick’s Sporting Goods (DKS) 7:30am, $0.41 - Preview

- George Weston (WN CN) 7:45am, C$1.53

- Home Depot (HD) 6am, $1.13 - Preview

- Jack in the Box (JACK) 4:02pm, $0.53

- La-Z-Boy (LZB) 4:10pm, $0.34

- Ma-Com Technology (MTSI) 4:05pm, $0.33

- Medtronic (MDT) 7:15am, $0.96 - Preview

- PetSmart (PETM) 5:55pm, $0.94

- Sears Canada (SCC CN) 7am, NA

- TJX Cos (TJX) 8:28am, $0.85 - Preview

- Vipshop (VIPS) 4:01pm, $0.07

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Shale Output Unchecked by Rig Cutback as Top Fields Become Focus

- Gold Climbs to Two-Week High on Speculation ECB May Buy Bullion

- Iron Ore Bear Market Deepens as China Home Data Add to Concern

- China’s Ore Supplies Cushioning Nickel Output Amid Disruptions

- Oil Fall Not Mirrored at Pump to Crimp Demand Growth: Julian Lee

- Aluminum Falls to Two-Week Low on Concern Slowdown to Sap Demand

- Goldman Says OPEC in Dilemma as Output Cut Seen Helping U.S.

- Corn Falls for a 3rd Day as Record U.S. Harvest Nears Completion

- MORE: Spot Gold Climbs to Highest Price This Month, Gains 0.8%

- Sugar Rises Amid Prospects for Future Deficits; Cocoa Advances

- Rubber Falls by Most in 2 Weeks in Tokyo Amid Japanese Recession

- Singapore Iron Ore Futures for March Settlement Drop Below $70

- Money Managers Raise Aluminum Bullish Bets on LME in Latest Week

- WTI Rises Before OPEC Meeting as Dollar Weakens; Brent Stable

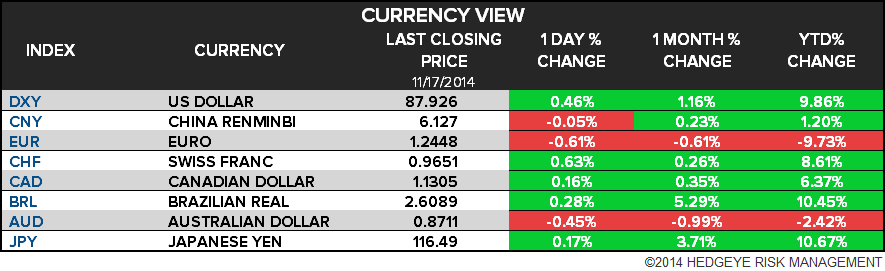

CURRENCIES

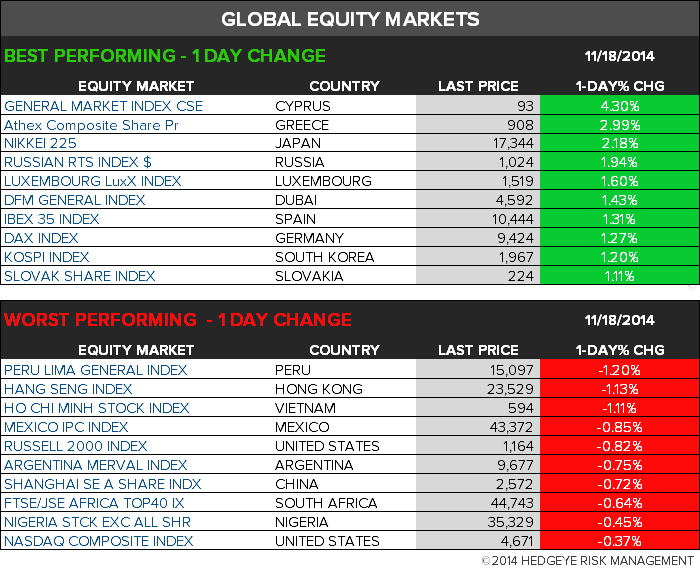

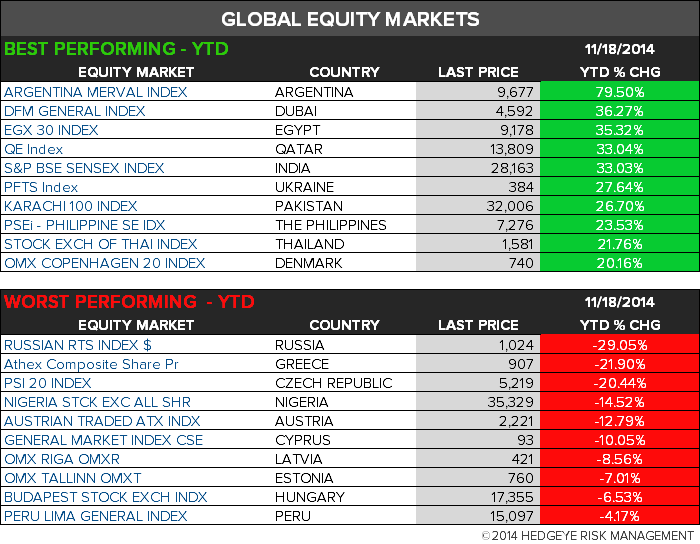

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team