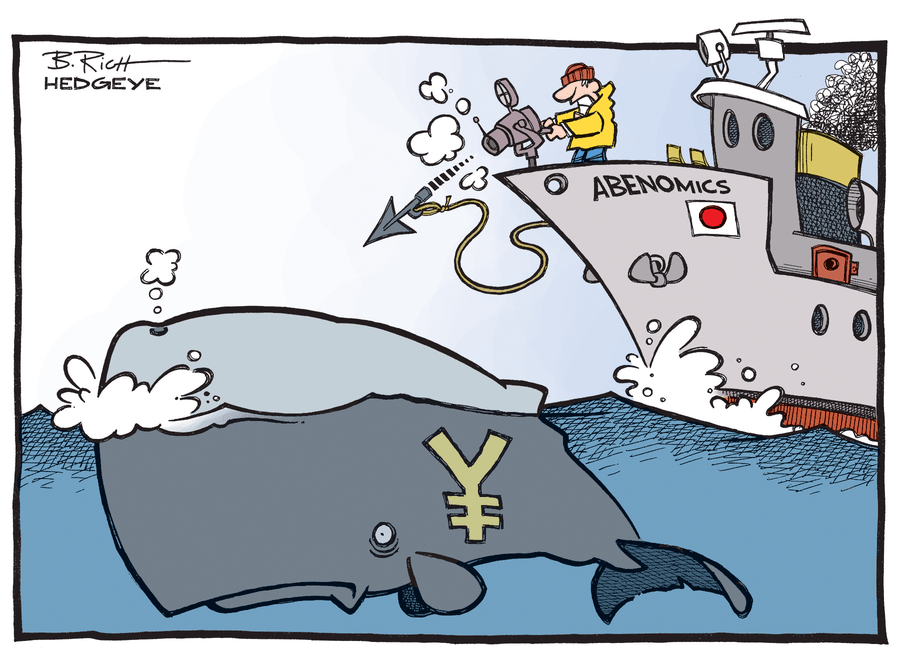

Japan’s equivalent of Janet Yellen (his name is Haruhiko Kuroda) essentially said that Hedgeye Macro nailed it on our #GrowthSlowing call and that the Bank of Japan is at a “critical point to overcome deflation.” There’s that word again, #deflation.

Forget what 80 TRILLION is in the context of what the Germans did in the 1920s for a second (99% of people in this world don’t get the econ #history lesson anyway) and think about what this Panic Policy in Japan is going to do to the rest of the world’s economics in 2015