Credit Quality Tailwinds

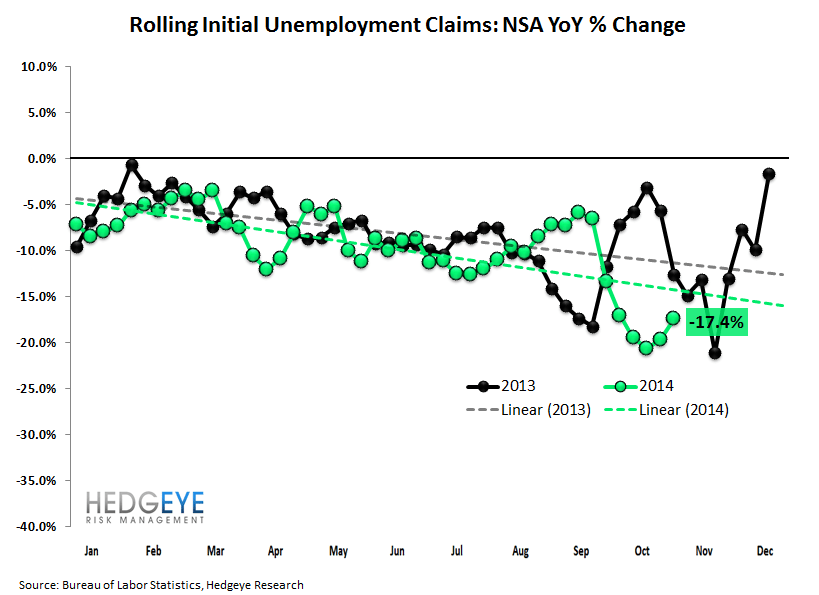

Jobless claims experienced an especially sharp deceleration in recent weeks. The NSA rolling series was better y/y by -20.6% in the October 24 week and by -19.7% the week of Halloween. The most recent November 7 week continued that trend, although at a slightly less extreme -17.4% y/y rate. Rolling SA Claims, meanwhile, came in just above the recent 281k post-crisis low at 285k. Overall, the labor market continues to hum along steadily.

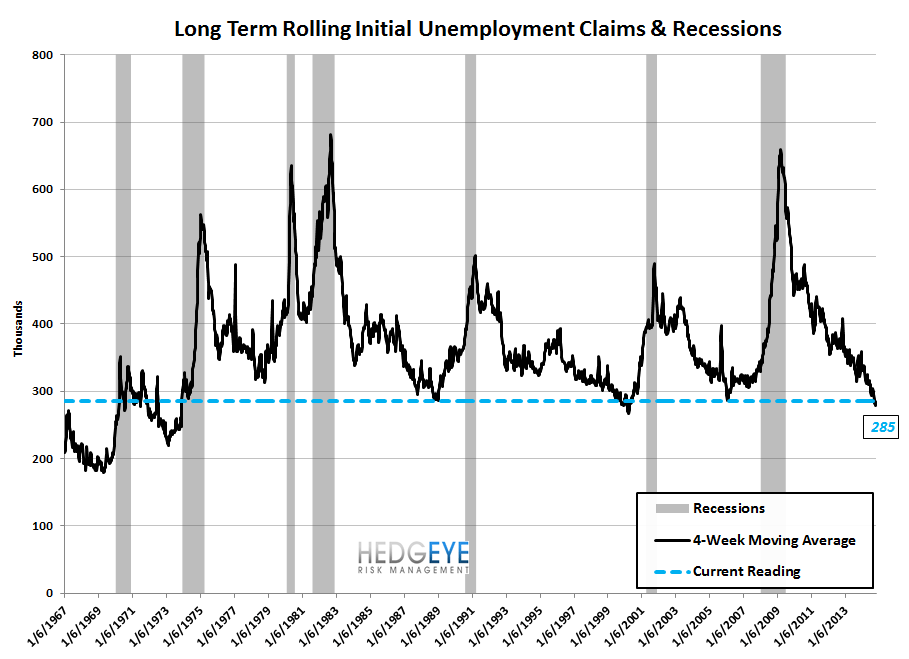

As we've been flagging in recent weeks claims currently sit at the all-time low of the last three economic cycles (2006, 2000 and 1988). Following each of those lows, claims rose dramatically. While these are in some ways the best of times, they are also the most dangerous.

The Data

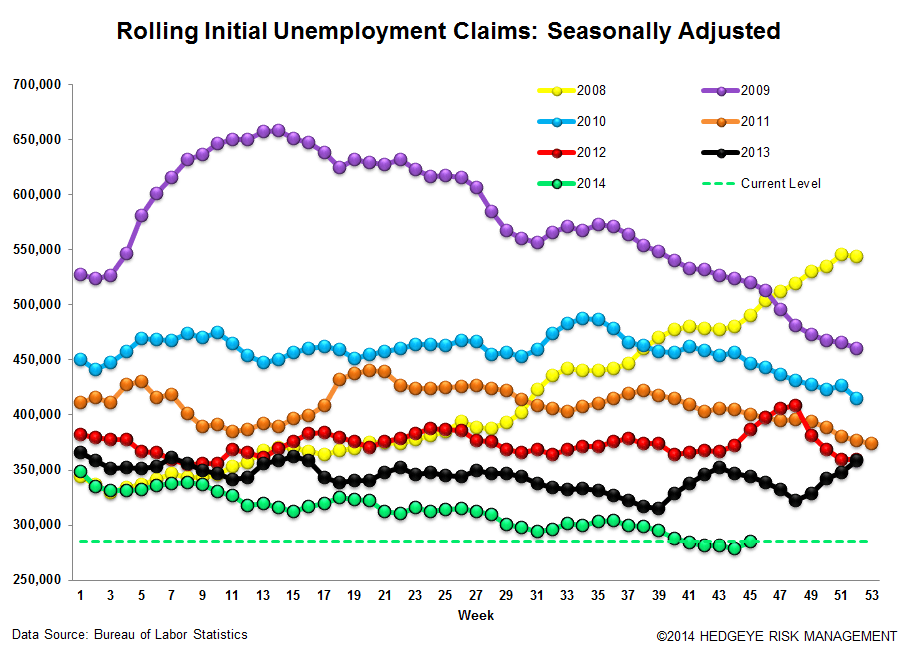

Initial jobless claims rose 12k to 290k from 278k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 6k WoW to 285k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -17.4% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -19.7%

Yield Spreads

The 2-10 spread rose 2 basis points WoW to 183 bps. 4Q14TD, the 2-10 spread is averaging 185 bps, which is lower by -14 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT