Editor's note: Below is a brief excerpt from a recent research report written by Hedgeye senior macro analyst Darius Dale. You can read the note in its entirety here. On the house. If you would like to learn more about leaving the vulnerable consensus herd once and for all and become a subscriber to the fastest growing independent research firm in America click here.

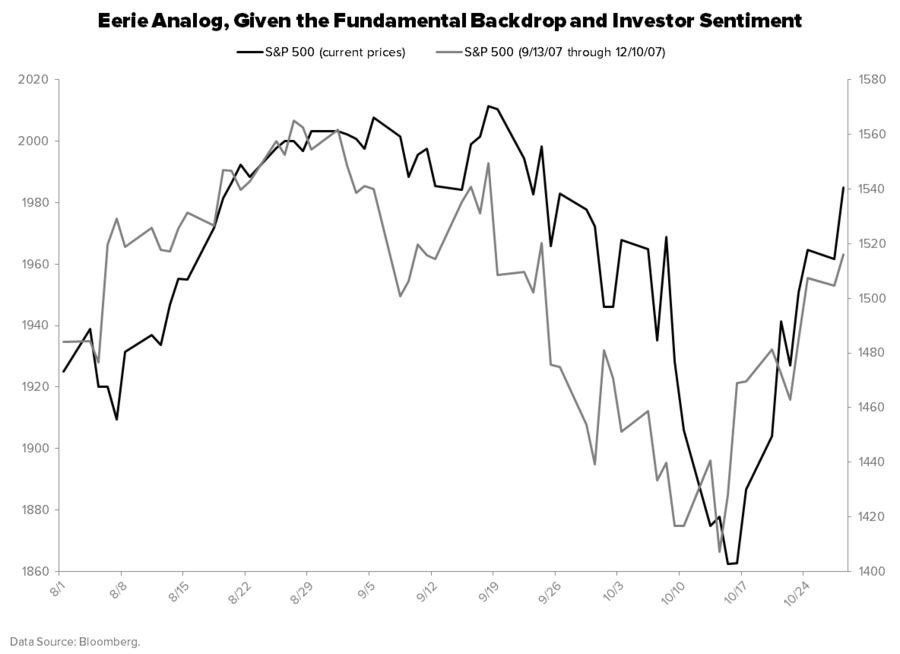

Remember Late-2007?

The current stock market trajectory overlays almost perfectly with its late-2007 analog – which is the last time consensus was as wrong on the outlook for domestic economic growth as they are today.