EVENTS TO WATCH

Wednesday (10/29)

- KSS - Investor Day: 9:00am

- RL - Earnings Call: 9:00am

- HBI - Earnings Call: 4:30pm

Thursday (10/30)

- SHOO - Earnings Call: 8:30am

- COLM - Earnings Call: 5:00pm

ECONOMIC DATA

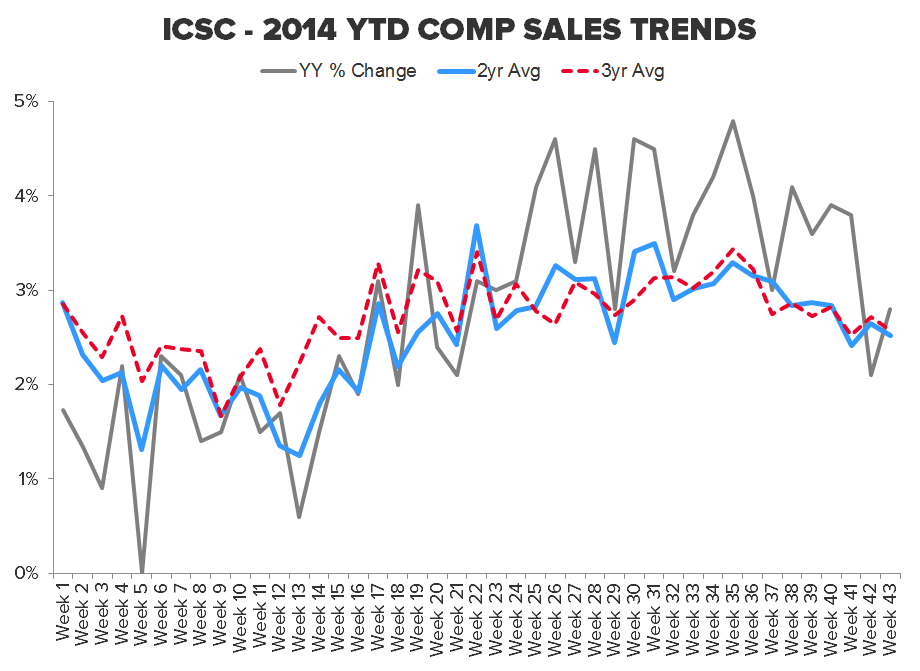

Takeaway: We can't help but callout the bifurcation we've seen over the past few weeks between the numbers reported by ICSC and the retail comp numbers we've seen out of those accountable to the public markets. The relative strength we've seen out of the ICSC (which we would note has been slowing on the 2 year trend line since early August) has not been reflected in the sales numbers we've seen coming out of the 3rd quarter. We'd point to WMT, GPS, URBN, KSS, and to a lesser extent JCP as levered names to the US consumer that we would expect to benefit. That certainly hasn’t been the case.

COMPANY HIGHLIGHTS

COH - 1Q15 Earnings

Takeaway: This was the first time in over three years that we weren't bearish headed into a COH print. To be clear, the fundamental story is absolutely broken and this change in direction has nothing to do with any near term upside we see in the business model. In fact our numbers 2-3 years out are 25% below consensus. We think the absolute best-case downside is about $5, which is hardly enough with the stock trading at $36. The truth is that we'd need to see the company face-plant on its recently announced Brand repositioning, and there are no expectations for any meaningful results for another 1-2 years. Until then, the company has a hall pass to be subpar.

CROX - 3Q14 Earnings

KSS - Kohl’s Corporation to Host 2014 Investor Conference and Updates Guidance

(http://phx.corporate-ir.net/phoenix.zhtml?c=60706&p=irol-newsArticle&ID=1981971)

- "Kohl’s Corporation expects comparable sales to decrease 1.4% in the third quarter. October sales have been softer than the balance of the quarter. Geographically, the Company expects sales to be consistent across all regions. E-Commerce sales are expected to increase over 30%."

- "By line of business, the Company expects Children’s to report comparable sales increases for the quarter. Accessories, Footwear and Men’s are expected to report lower sales, but to outperform the company average. Home and Women’s are expected to underperform the company average."

- "Based on actual sales to date, the Company expects its 2014 diluted earnings per share to be at the low end of its prior guidance, which was previously $4.05 - $4.45 per diluted share."

Takeaway: For the full text of our note, 'KSS-It'll Miss Again', from this morning click here: LINK

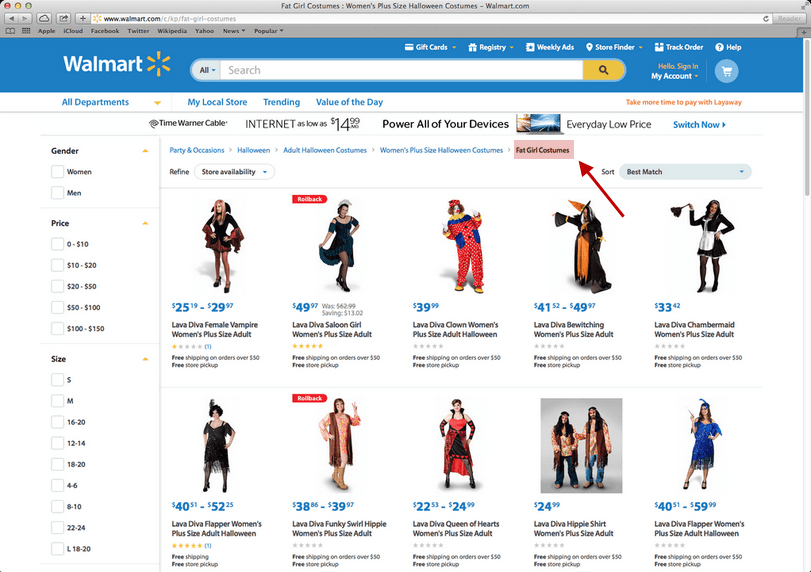

WMT - Walmart Apologizes for Advertising ‘Fat Girl Costumes’ on Its Website

(http://time.com/3542693/wal-mart-apologizes-fat-girl-costumes/)

- "Retail giant Walmart caused a stir on Monday, after a listing for plus-size Halloween outfits appeared on their website under the heading 'Fat Girl Costumes.'"

- "The retail chain quickly backtracked, issuing an apology before changing the heading to 'Women’s Plus-Size Halloween Costumes.'"

Takeaway: How does this make it past quality control?

OTHER NEWS

M - Macy's to Open in Abu Dhabi

- "Macy’s will open a 205,000-square-foot, four-level store at Al Maryah Central, described as a 'super-regional shopping destination' under development on Al Maryah Island in Abu Dhabi."

- "A 230,000-square-foot Bloomingdale’s will also open in Al Maryah Central, marking that retailer’s second overseas store. The first opened in Dubai in 2010."

- "Bloomingdale’s and Macy’s, both divisions of the $28 billion Macy’s Inc., plan to open their Abu Dhabi locations in 2018. They will be operated under license by Al Tayer Group, which already operates the licensed Bloomingdale’s store in Dubai."

WMT, JCP, KSS, M - Traffic At Los Angeles Ports Backed Up For 2 Weeks, Threatens Holiday Season

- "'This is really a perfect storm,' Port of Los Angeles Executive Director Gene Seroka told the Los Angeles Times.

- "The pre-holiday surge of cargo for retailers like Wal-Mart, JC Penney, Macy’s, and Kohl’s has always been a busy time of year, but it’s made worse this year by the use of massive container ships. These larger vessels can be up to one-third larger than Los Angeles and Long Beach ports have the capacity to handle. The root of the problem, though, is likely due to a shortage of trucking equipment."

- "'We have a meltdown on the harbor,' said Robert Curry, president of California Cartage Co., a trucking firm serving both ports. 'Every day it gets worse.'"

LOW - Lowe’s to enter Manhattan with smaller-store format

(http://www.chainstoreage.com/article/lowe%E2%80%99s-enter-manhattan-smaller-store-format)

- "Lowe's announced that it will enter its first two stores in Manhattan. The home improvement giant has two locations slated to open in the second half of 2015, one at 2008 Broadway at West 68th Street, and a second at 635 6th Avenue at West 19th Street."

AMZN - Amazon to buy first Indian start-up QwikCilver Solutions, a gift card tech firm

- "Amazon India is in advanced talks to buy a minority stake in gift card technology and retail firm QwikCilver Solutions, according to three people aware of the development. The deal, if successful, will mark the first investment in an Indian startup by the Seattle-based firm which is battling rivals Flipkart and Snapdeal for primacy in India's online retail industry."