The argument that OPEC is making a strategic move to put its foot on the gas from a production standpoint to test unconventional production sources ahead of a meeting where it will cut production targets will disappoint as a bullish catalyst in our opinion.

For one, we have no reason to believe OPEC has a good understanding of the technological advancement in production efficiency in North America.

We’ll be hosting a call with analysis on this topic next Tuesday, October 28th. Please email for access.

Real Cost of Producing Tight Oil and Shale Gas: Fact vs. Fiction

Secondly, at no time in recent history has OPEC leveraged itself, banded together without internal conflict, and proven to be a functional organization. All of the countries within the Organization of have played this chess match internally with one another throughout history while continuing to produce at whatever levels they deem necessary to boost the domestic economy. When conflict has reduced capacity between OPEC members, others have stepped in to ramp up production and take market share.

Now most OPEC economies are completely dependent on oil production:

- OPEC holds an estimated 60% of the world’s reserves and 30% of total supplies. Venezuela, Angola, and Iran (all higher cost producers) have all reportedly pushed for collective supply cuts

- Oil and Gas accounts for roughly half of GDP and 3/4ths of export earnings on average among OPEC countries: Each member is constantly seeking an increasing share of the global marketplace

- OPEC’s largest producer, Saudi Arabia, receives 85% of its export earnings from the oil and gas sector

OPEC Losing its Strength

Even if the organization collectively agrees, for the first time since the 70s and 80s they run the risk of losing major market share to those outside of the organization.

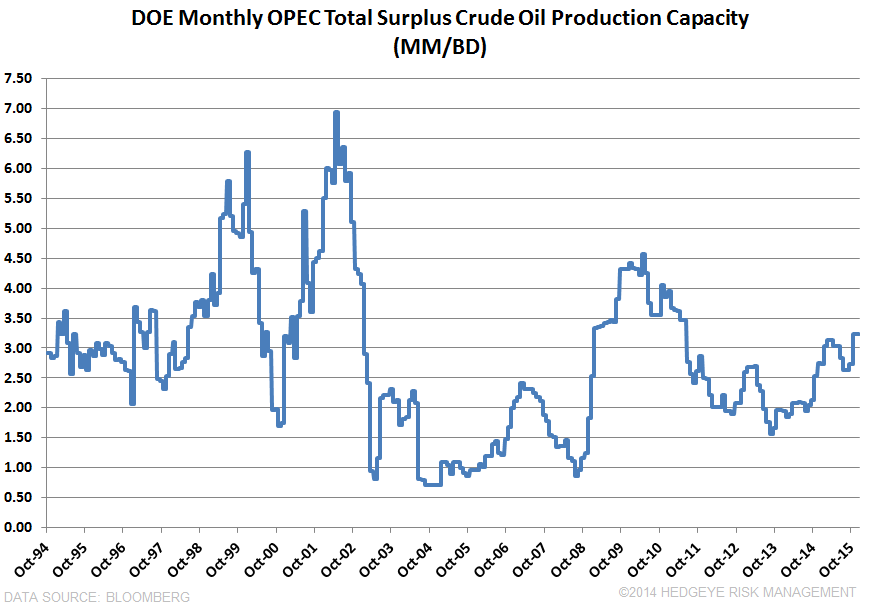

While spare capacity within OPEC countries remains relatively constant…

Of most significance to the expectation of an announcement of FORMAL production cuts, the vote must be unanimous among member countries

In article 11.C of OPEC’s Statute, it says “Each full member country shall have one vote. All decisions of the conference, other than on procedural matters, shall require the unanimous agreement of all full members.”

Member Countries agree by unanimous vote on any such production ceilings and their allocation to the respective member countries. At the same time, each member country retains absolute sovereignty over its oil production.

In just the last ten years, the expectation of a fair oil price has been much lower than current levels:

- In 2002 OPEC agreed that a fair price on crude oil should be set between $22 and $28 a barrel

- By 2006 Qatari Energy Minister Abdullah Attiyah maintained that a fair market price for crude oil should be in the range of $50 to $55 a barrel

- $80/barrel will now spark unanimous collaboration in cutting production levels? Doubtful.

The largest producers can handle oil much lower and they will not agree to production cuts as OPEC’s collective grip on controlling global energy prices is waning.

Assuming we did experience a decline in oil imports from OPEC members, we’re closer to self-sustainability even if we don’t lift the export ban.

However, in a recent note we outlined the current pressure on Washington to lift the export ban which would be even more threatening to OPEC’s influence:

Can the U.S. Shale Boom Be Stopped

The following piece is an excerpt from the note:

“OIL: THE PRESSURE TO LIFT THE EXPORT BAN IS OFFICIALLY HERE

- export ban on oil implemented after the oil embargo in the 1970s

- The Jones Act (1920) requires that oil has to be shipped by Americans in smaller ships:

- It costs around $5-$6 a barrel to ship crude from the Gulf of Mexico to the US east coast on a US-flagged vessel, but only $2 to ship to Canada’s east coast on a foreign-flagged vessel

South Korea and other NATO allies have verbally challenged the U.S. ban on the back of our recent increase in domestic production capacity. Last week the EU’s commissioner for trade, Karel De Gucht, emphasized the need to free up more sources of oil and gas for a wider and more effective free-trade agreement to be instituted.

The Office of the U.S. Trade Representative and the NSC have held internal discussions with the Obama Administration on how to deal with a challenge from the international community. Washington was able to make a national security argument for implementing the ban back when it was importing most of its crude oil, but the added production from the Shale boom is challenging the credibility of that argument.

With added geopolitical tension globally this year, both Asian and European allies are pushing for diversified supply lines. Strengthening their argument, the U.S. just took China to the WTO earlier this year and won a case accusing Beijing of hoarding raw materials and precious metals. Under International Trade rules (General Agreement on Tariffs and Trade), the argument for upholding the restrictions on the exporting of U.S. fossil fuels may be too hypocritical to justify.”

However, Iranian spokesmen came out Tuesday and said that they weren’t concerned about prices at these levels which seemed interesting in crafting the argument that OPEC is testing new and unconventional energy plays. As difficult as it’s been to pin down the per unit production costs associated with U.S. shale plays, public comments from member nations suggest they are still getting to the bottom of production breakeven costs from unconventional sources in other parts of the world.

In summary, there two major factors threatening OPEC’s stance in the global energy trade:

1. The U.S., the world’s largest consumer, is much less reliant on OPEC production and U.S. supply continues to surprise on the upside according to weekly DOE inventory data released yesterday:

Supply (beat to the upside)

- DOE U.S. Crude Inventories 7111K vs. 2800K est. (8923 prior)

- DOE Cushing, OK Crude Inventories 953K vs. 716K prior

- DOE U.S. Gas Inventories -1299K vs. -1560K est. (-3995K prior)

Demand (Less than Expected)

- Crude Oil Implied Demand 15395K vs. 15416K est.

- DOE Gasoline Implied Demand 9283K vs. 9489K est.

2. The U.S. is continuously closer from an infrastructural and regulatory standpoint to becoming an exporter which means we could step in and take share (or at least create the expectation that we’ll take share) if OPEC were to cut production targets.

OPEC is scheduled to meet in Vienna on November 27th for one of two annual meetings, and a few members have called for an emergency meeting beforehand, but current price levels are not a threat to the largest producers making any collaboration among members of the organization highly unlikely.

- OPEC pumped 30.96M B/D on average in September vs. its 30M B/D target (30.15M B/D in August)

- OPEC’s own estimates are for its crude demand to be 29.20M B/D ( verbally attributed to the U.S. shale boom and other unconventional supply elsewhere) on average in 2015, well below what it’s currently pumping.

WE BELIEVE FORMAL PRODUCTION CUTS FROM OPEC ARE HIGHLY UNLIKELY AND WILL DISAPPOINT AS A BULLISH CATALYST IN THE BACK HALF OF Q4.

Please feel free to reach out with any comments or questions.

Have a great evening.

Ben Ryan

Analyst