Brief Analysis: We removed EAT from our Investment Ideas list as a short on October 9th, 2014. We thought this was a prudent move given the current sales momentum we are seeing across the restaurant industry. To be clear, we wanted to get the 1QF15 release out of the way, and were mistaken in doing so. Brinker's comp sales outpaced both Knapp and Black Box by notable margins and surpassed consensus expectations, but weren't strong enough to drive enough leverage through the P&L. In addition, two-year average comps and traffic declined sequentially, suggesting that management is not doing enough to move the needle.

Brinker has prided itself over the past four years on methodically driving operating leverage in their business model, but we believe these days are abruptly coming to an end, even despite management's decision to maintain guidance for a 25-50 bps improvement in restaurant operating margin in FY15. We believe this will be difficult to achieve and think management is (almost solely) relying on cost of sales to moderate for this to happen.

Despite covering our short a couple of weeks ago, our short thesis has not changed. In fact, if anything, our conviction in it has strengthened. Unfortunately, we missed today's move, but we'd be looking to short the name once again into any strength. We think the margin story is played out here and management will be hard pressed to drive leverage moving forward. The street is banking on the FY16 free cash flow story to come through for them as capex begins to wind down. We suspect, however, that this will disappoint as management is forced to allocate additional dollars to reinvest in the business.

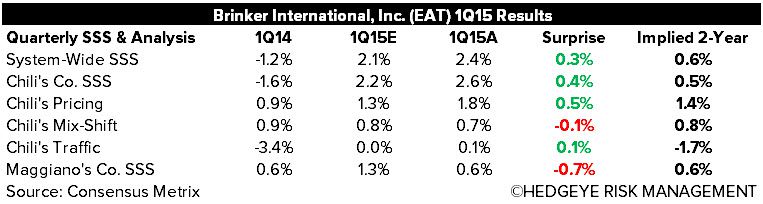

Comps: Brinker delivered system-wide comp growth of +2.4%. Chili's company-owned comps grew +2.6%, comprised of +1.8% of pricing, +0.7% of mix-shift and +0.1% of traffic. Traffic, while positive for the first time in the past seven quarters, saw its two-year average decline 30 bps sequentially to -1.7%. Total revenues of $711.018 million (+3.84% y/y) beat consensus estimates by 25 bps.

Margins: Cost of sales declined 28 bps y/y driven by favorable menu pricing, menu item changes, efficiency gains from new fryers and improved waste control. However, significant pressure from beef, cheese, avocados, and seafood resulted in significantly lower leverage than management had anticipated. Labor costs increased 18 bps y/y driven by higher bonuses and increased wage and payroll taxes, partially offset by lower health insurance expenses. Restaurant expenses increased 30 bps y/y driven by equipment charges associated with tabletop tablets and higher credit card fees. As a result, restaurant margins declined approximately 30 bps in the quarter. Management reaffirmed its guidance for a 25-50 bps improvement in this line in FY15.

Earnings: Adjusted EPS of $0.50 (+16.3% y/y) fell in-line with expectations.

What We Liked:

- Respectable system-wide comp growth of +2.4%

- Chili's comps outpaced Knapp and Black Box by 210 bps and 100 bps, respectively

- Reimage program is about 90% complete

- Installation of Kiosk tablets in all franchise restaurants will be completed next month

- Repurchased 1.1 million shares for $53.3 million in the quarter; repurchased another 712,000 shares for $37 million since then, bringing the outstanding share authorization down to $576 million

- Announced a 17% increase in quarterly dividend from $0.24 to $0.28

What We Didn't Like

- Two-year average traffic declined 30 bps sequentially to -1.7% at Chili's

- International franchise comps were down -0.5% driven by soft sales in Puerto Rico

- Menu innovation hasn't really moved the needle on traffic

- Restaurant level margins down despite a fairly strong comp

- Food costs will likely continue to present a challenge for management given their unpredictable nature

- Seemingly little to no leverage left on labor cost and other restaurant expenses lines

Call or email with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst