Takeaway: We put together a 40-page deck outlining our bearish long-term view on BABA. But we don't have a near-term catalyst, so we're staying on the sidelines for now. High level themes below. More detail to follow.

KEY THEMES

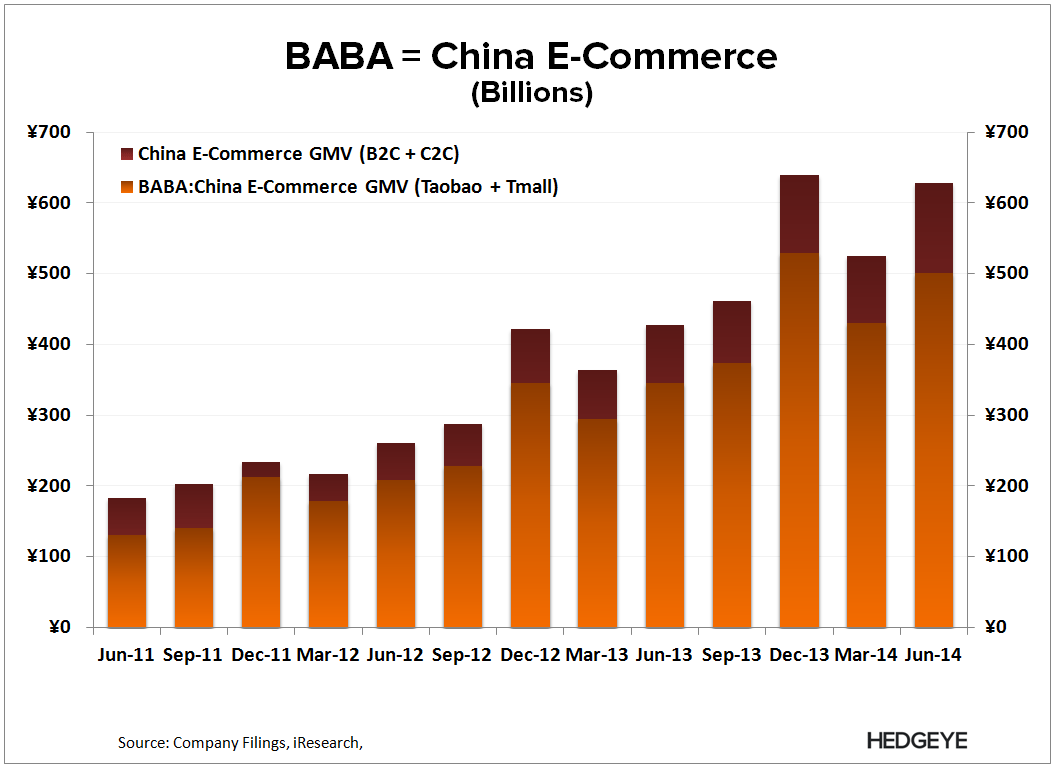

- TOO LARGE TO CONTROL ITS OWN DESTINY: BABA is essentially China’s E-commerce market, with over 80% of all E-commerce GMV, and over 75% of traffic flowing through its sites. Without room for share gains, which historically have been tenuous, BABA will become increasingly dependent on the China Growth Story to drive its business moving forward.

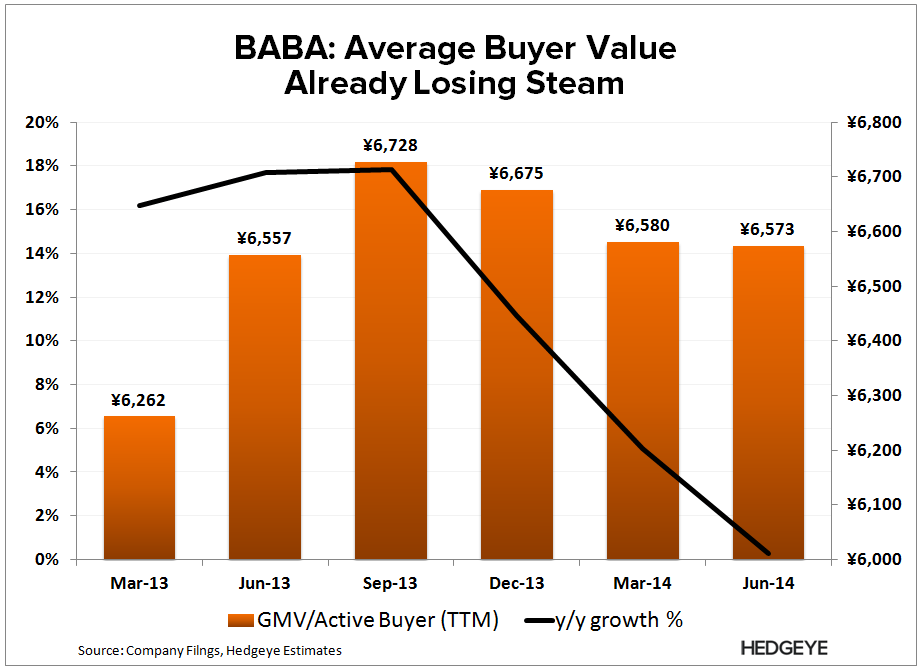

- CHINA CAN’T GROWTH FAST ENOUGH: While BABA cites this as an opportunity, there is a reason why China lags many major economies in terms of both e-commerce and internet penetration: the Chinese consumer is relatively weaker in terms of both incomes and discretionary spend. There is naturally room for new user growth, but it will come with a declining yield since these users have less to spend, which means the average GMV (Gross Merchandise Value) of the BABA consumer is facing decline.

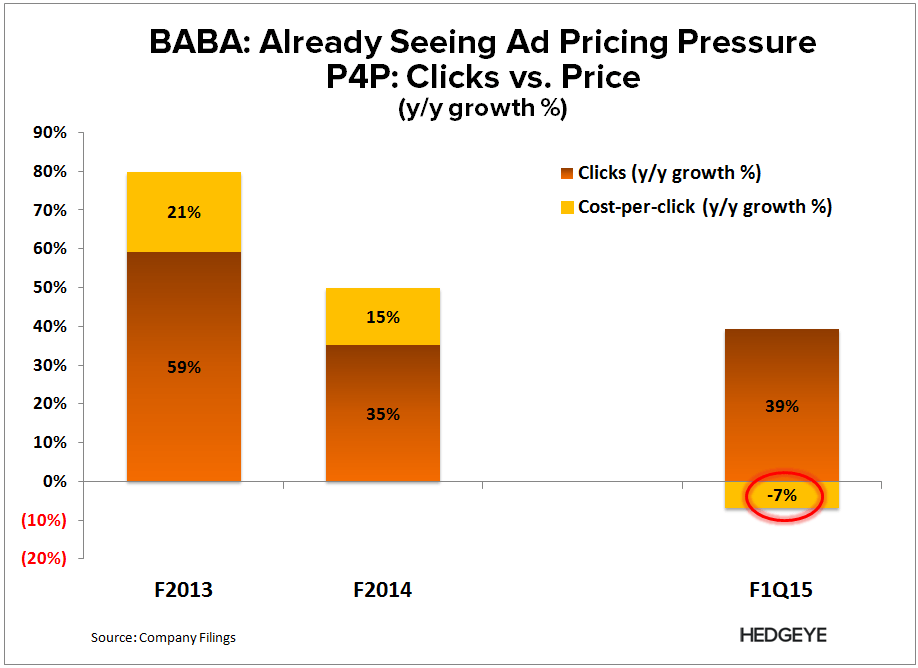

- GROWTH WILL COME AT A PRICE: Roughly 60% of BABA’s revenues come from vendors marketing to BABA consumers; over 75% of which from P4P (Pay for Performance) ads that require user engagement (clicks) to generate revenue for BABA. If the average GMV/Active Buyer is facing decline, then the average buyer (and their ad clicks) are worth less to BABA’s vendors. We’re expecting pricing pressure across its Marketing segment, which we’re already seeing signs of today due to the rise of mobile (low-cost vehicle to internet access in China). Further, if the mix of mobile users continues to grow, then it may also mean less ad inventory since BABA currently isn’t offering a comparable number of ads (vs. desktop).

- NEAR VS. LONG-TERM OUTLOOK: Feasible vs. Lofty Consensus Estimates (40% and 35% revenue growth in F2015 and F2016, respectively). A strong 1Q15 (up 46% y/y) makes F2015 estimates within reason, but we’re not expecting much upside. F2016 is a different story; the question is whether growth in Commission Revenue (~25% of total) can compensate for our expectations for a marked slowdown in growth in Marketing Revenues (~60% of total). Commissions have a very strong tailwind from GMV (transactions) mix shift of to branded products on Tmall (where BABA collects commissions), while Marketing revenue is facing headwinds across a number of fronts (see #2 & 3 above). We’re expecting F2015 and F2016 revenues of ¥73.0B and ¥94.5B vs. consensus of ¥73.7B and ¥99.6B, respectively.

- WHY WE’RE ON THE SIDELINES: First, we don’t have a catalyst in sight near-term (we don’t even have an event yet). Second, our view here is longer-term, and we’re not as bearish on F2015 as we are F2016 and thereafter. The stock currently trades at ~20x forward revenue, which means this is a sentiment story. That makes the stock highly sensitive to immaterial news flow outside a fundamental catalyst, which once again we don’t have near-term, making BABA a dangerous short near term.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet