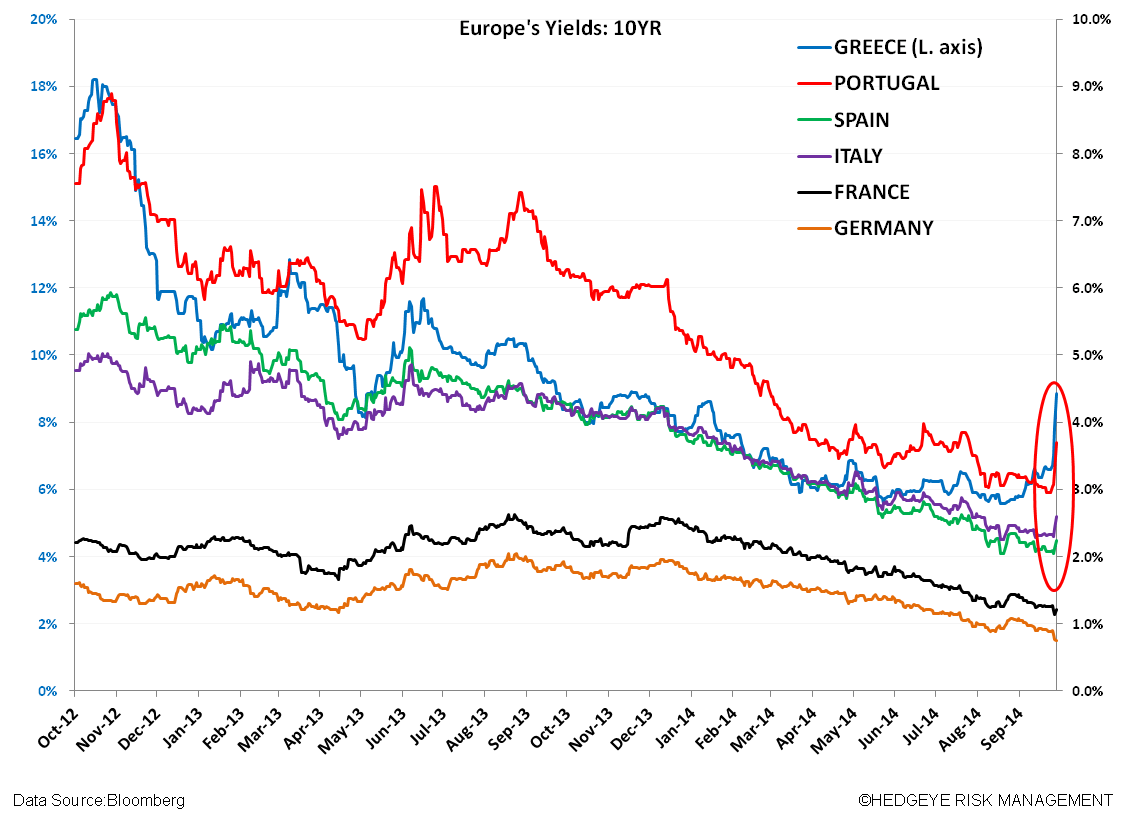

There’s a recent swift inflection in Eurozone peripheral yields and select Eurozone equity markets roll into crash phase! #PrepareYourself

Despite the steady improvement (decline) in sovereign periphery bond yields on a year Y/Y basis, the inflection taking place on a D/D and W/W basis is significant. Here’s a look at the 10YR yields:

- Greece 8.91% (+105bps D/D ; +229bps W/W)

- Portugal 3.67% (+38bps D/D; +71bps W/W)

- Italy 2.59% (+17bps D/D ; +28bps W/W)

- Spain 2.22% (+10bps D/D; +14bps W/W)

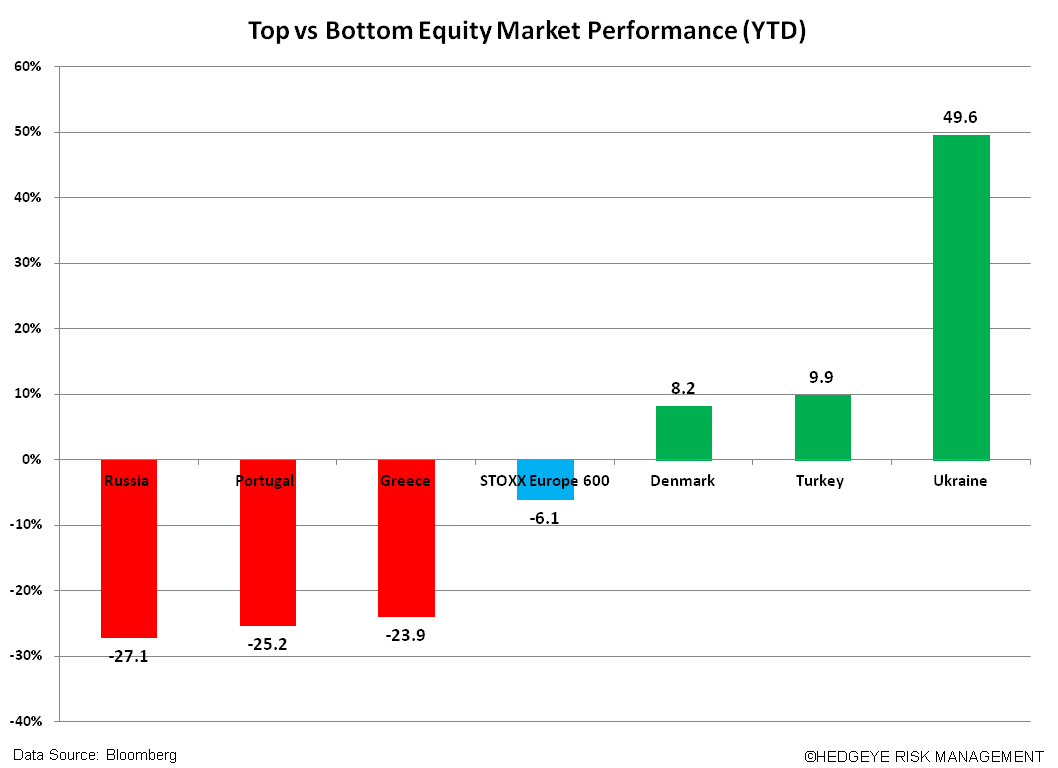

And Portuguese and Greek equity markets are down YTD -25.2% and -23.9%.

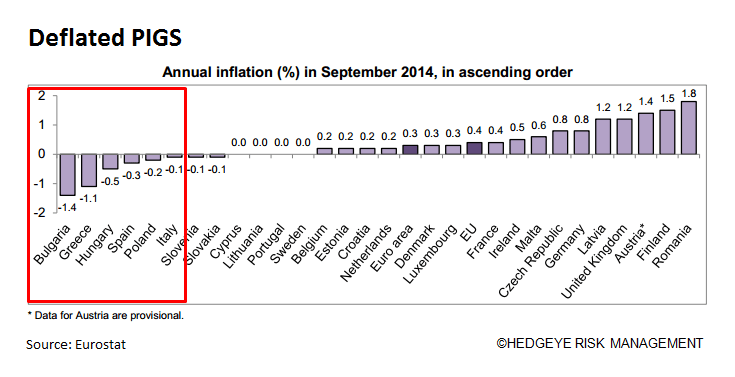

Why the shift? As we expressed in our Q4 Macro Themes playbook, not only is global growth getting a lot worse, but specifically in our #EuropeSlowing theme we stress that Draghi’s Drugs will not arrest deflation (currently at 0.3% Y/Y) nor produce sustainable economic growth.

A second theme we continue to hammer home is that US economy has entered #Quad4, which is characterized by slowing growth and decelerating inflation.

And our last theme, #Bubbles, demonstrates that we see a significant number of market bubbles (including the SPX). Our call is “they don’t bounce”, or said another way, we’re recommending a 0% exposure (or short position if applicable) to the equity market, and not buy-in points.

Add on in recent weeks:

- Global growth forecasts were taken down by the IMF (and by numerous individual countries/governments)

- Persistent geopolitical risks (ISIS, Ukraine, and Hong Kong)

- Ebola outbreak concerns

And there’s plenty of “juice” to send risk premiums higher. Specifically in Europe, we’re seeing a confluence of factors that are sending the risk trade (not growth trade) higher.

- Greece: Political uncertainty – Greek PM Samaras reiterated his belief that Greece would hold a general election in 2016, even though his government faces the prospect of losing the presidential vote in February

- Greece: Financial uncertainty – There’s backlash and investor uncertainty over Greece’s claim to be purely market funded. We believe the country will need to ask for another credit line from the EU when EU funds run out this year (note: Greece is still taking funding from IMF through 2016)

- Italy: Joins France on sending Austerity is Dead message with Italian PM Renzi presenting an expansionary, tax-cutting 2015 budget that ignores the concerns from the European Commission on meeting its original deficit reduction target.

If we’re right that Draghi won’t be able to bend gravity to arrest deflation and produce sustainable economic growth, we’d expect sovereign yields from the Eurozone’s weaker member states to move higher commensurate with a higher risk profile. We expect the stronger deflation in peripheral countries to persist and extend the time period to higher growth levels.

We direct you to recent work including Just Ugly Charts #EuropeSlowing and #EuropeSlowing – Austerity Is Dead? for more on our investment position, outlook on ECB policy, and country-specific commentary.

Matthew Hedrick

Associate