QUAD #4: We’ve been highlighting the emergent entry into Quad #4 (characterized by disinflation and decelerating growth) in our GIP model with regular frequency for over two months now. We walked through the model in extended detail and our preferred positioning most recently here >> THE MARKET THINKS WE'RE IN QUAD#4...DO YOU?

In short, you want to be long/OW the stuff that is working today (Bonds, Cash, large cap defensive yield) and short/UW its converse (high beta, small cap illiquidity and early cycle leverage)

QUAD #4...GLOBALLY: While we typically apply the model on a country by country basis, it generalizes to any regional or global aggregate. In fact, the price consequences of a global shift into quad #4 are that much more acute.

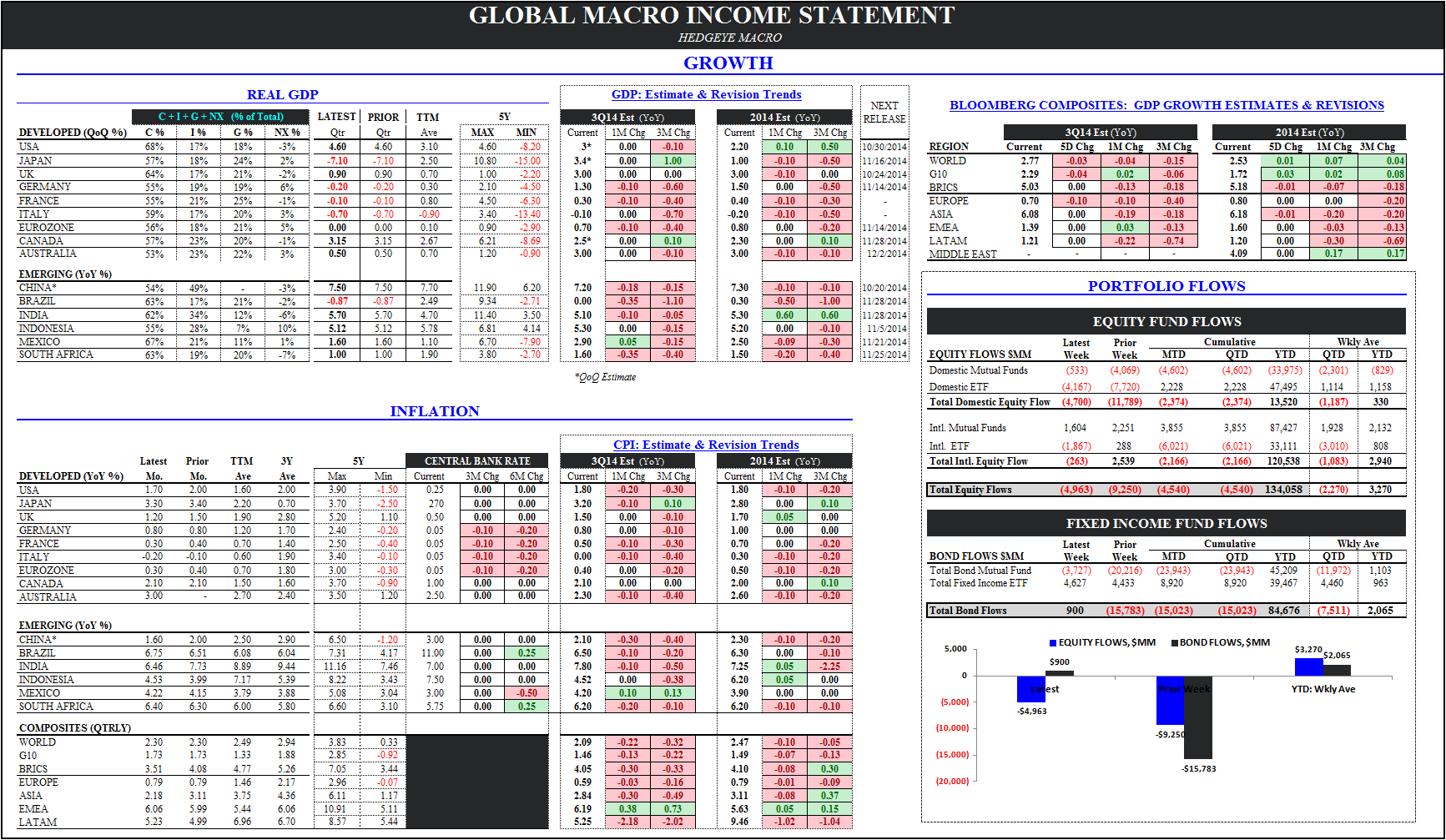

Looking across our global macro monitor – which tracks global growth & inflation trends - growth and inflation estimate revision trends over the last quarter across both developed and EM markets have been almost universally negative.

Note: the table size/font is probably hard to read but simply observing the overwhelming prevalence of red (ie. negative growth/inflation estimate revisions trends) across countries/regions is sufficient for internalizing the prevailing global trend.

DOMESTICALLY: In discussing the September jobs report we summarized the shifting variables under the Fed's policy calculus in this way:

ROW Growth Slowing + Global Disinflation Predominating + Domestic Wage Growth Decelerating + LFPR declining + Housing Slowing vs. Strong Initial Claims + Solid NFP Gains + Declining Unemployment Rate + Accelerating Aggregate Income Growth

In brief, the domestic labor market (& mfg) and aggregate income growth continue to crest while wage growth and housing continue to flag, EU/Japan remain in discrete deceleration, EM economies suffer under strong dollar pressure and disinflation predominates.

The left hand side of the equation has already pushed the Fed towards rhetorical dovishness. To the extent global quad #4 trends worsen, we import incremental disinflation and/or that ROW weakness spills over into the domestic macroeconomy, we can expect more of the same in terms of reactionary policy response.

Unless this-time-is-different, relative exceptionalism (ie. sustained de-coupling) wins the day, it’s unlikely the US goes escape velocity in isolation.

Indeed, inflation expectations continue to collapse, rate hike expectations are getting pushed out and, from a rate of change perspective, the domestic macro data has, on balance, been slowing.

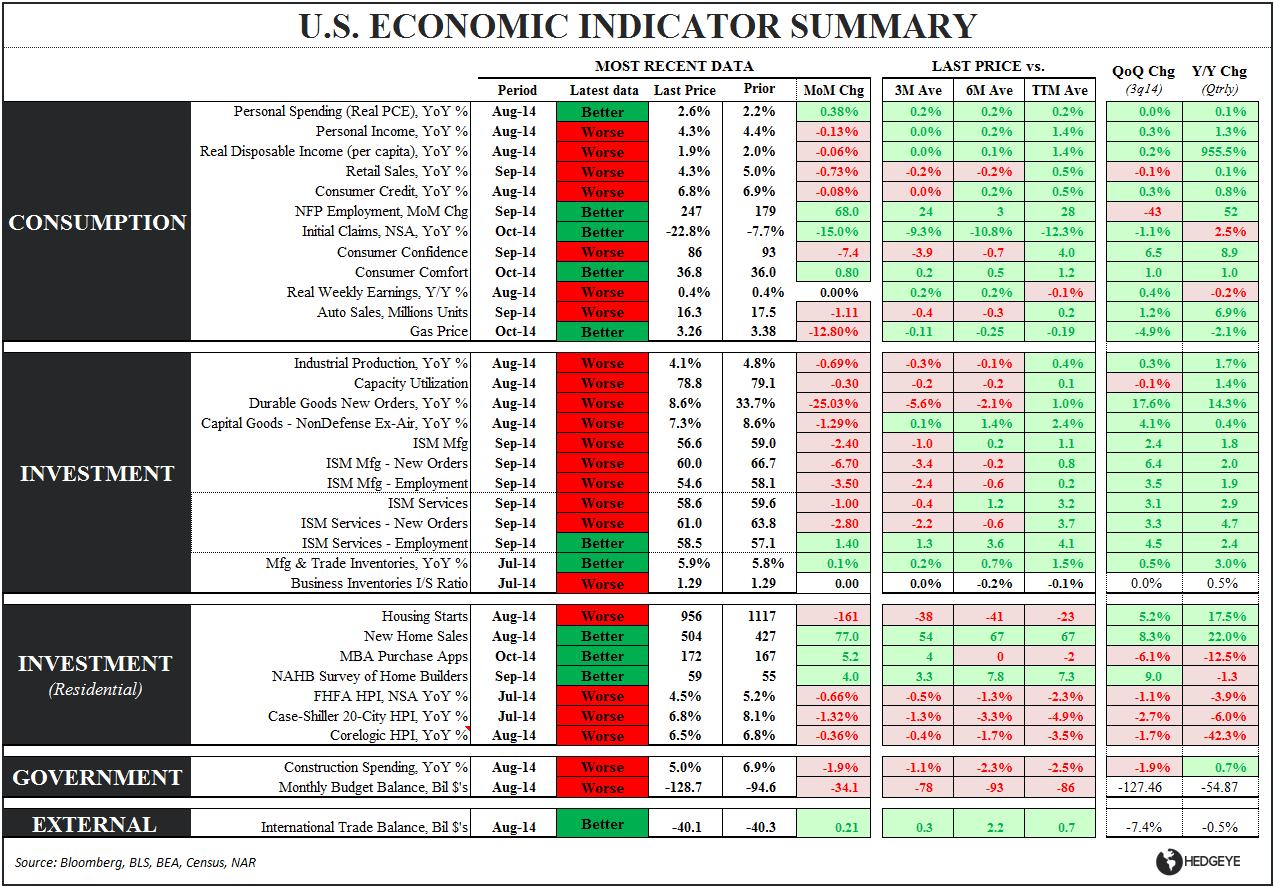

0 for 4 TODAY: We had a quadfecta of disappointing data this morning with Retail Sales, PPI, Empire Manufacturing & Mortgage Purchase Applications all deteriorating sequentially.

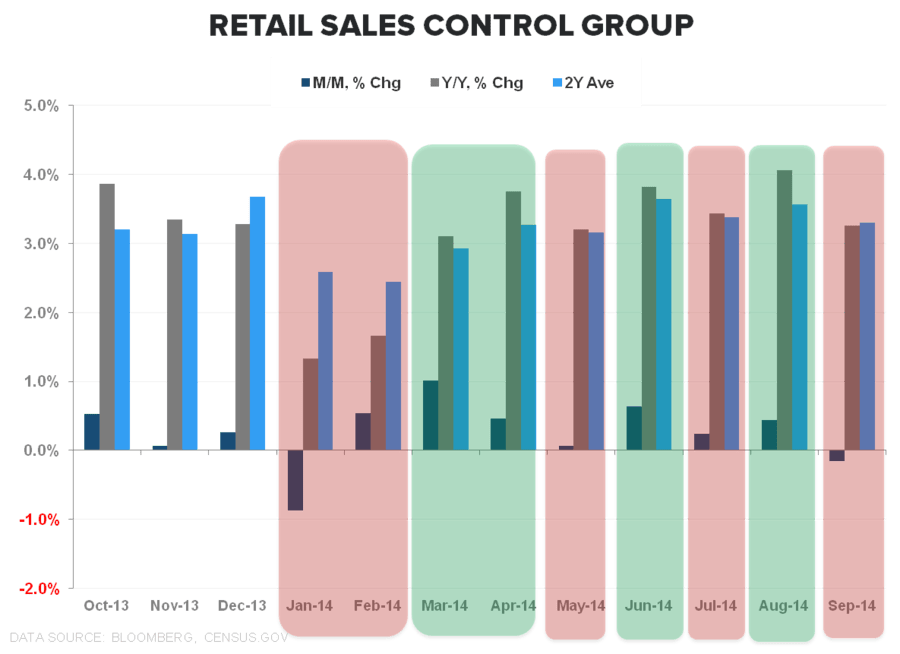

- Retail Sales: The (expected) decline in auto sales and lower gas prices drove the bulk of the decline in Headline Retail sales with weakness in furniture and building materials sales exacerbating the drop. Across the control group, declines in Food, Clothing and e-sales led the first M/M drop since January with the 1Y and 2Y ave growth rates decelerating as well. Growth has been noteably choppy YTD (2nd chart below) and household income growth remains strong but the broad deceleration (11 of 13 industries reported decelerating growth) is noteworthy.

- Mortgage Purchase Demand declined a modest -0.7% W/W after last week’s bounce above the 170-level on the index. 4Q is currently tracking +2.5% Q/Q with the YoY improving to -4.1% in the latest week. Comps continue to ease significantly against 4Q13 and into 1Q next year as we lap the collective shock of rising rates, QM implementation, and FHA loan limit reductions.

- Refinance activity rose +10.6% W/W, on the back last week’s 5% rise, as rates retreated a full -10bps to 4.20%. After dropping -13bps in the last two weeks, rates are now back at their lowest level YTD and the lowest level since June of last year.

- PPI: Food and Energy/Gas led the -0.1% M/M decline in PPI-FD in September with both core and headline decelerating -20bps sequentially to +1.6% YoY. The deceleration was not particularly surprising given the broad and expedited commodity price declines, but it does offer further. confirmatory evidence of our entre into quad 4.

Christian B. Drake

@HedgeyeUSA