TODAY’S S&P 500 SET-UP – October 14, 2014

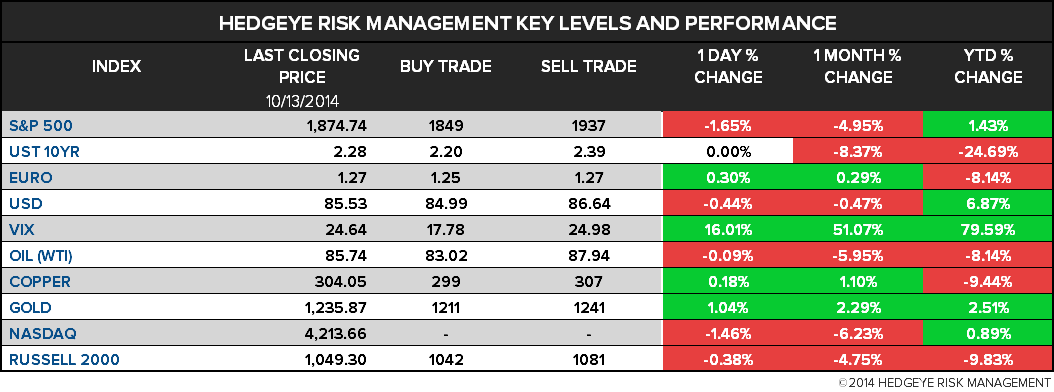

As we look at today's setup for the S&P 500, the range is 88 points or 1.37% downside to 1849 and 3.32% upside to 1937.

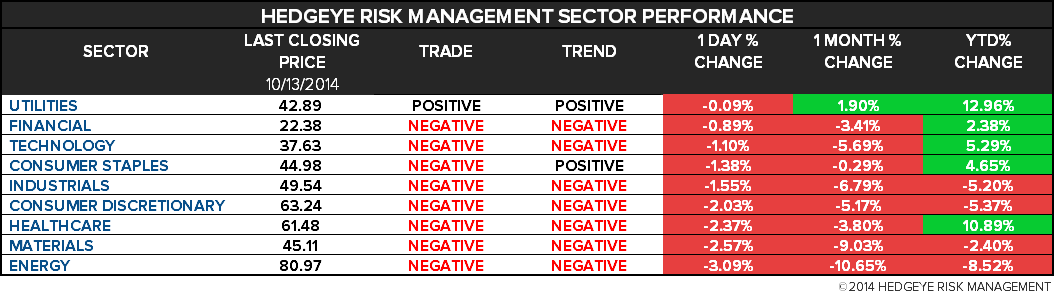

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.81 from 1.86

- VIX closed at 24.64 1 day percent change of 16.01%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: NFIB Small Business Optimism, Sept, est 95.8 (pr 96.1)

- 8:55am: Redbook weekly sales

- 11am: U.S. to announce plans to auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $27b 6M bills

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- Senate, House out of session

- Supreme Court may release list of cases it plans to consider

- Sec. of State John Kerry meets with Russian Foreign Minister Sergei Lavrov in Paris

- Obama at meeting with >20 foreign defense chiefs/ Joint Chiefs of Staff Chairman Martin Dempsey at Andrews

- 9am: Mexican Secretary of Economy Ildefonso Guajardo speaks at Woodrow Wilson Center

- 9:30am: Kaiser Family Foundation releases 50-state Medicaid budget survey, holds briefing

- U.S. ELECTION WRAP: Debates in Ky, Ark; Ebola; SD Polls, Ads

WHAT TO WATCH:

- JPMorgan 3Q Profit Misses, Rev Beats; Down 1% Pre-Mkt

- Too-Big-to-Fail Banks Face Capital Gap of Up to $870b

- Repo Traders Face FSB Collateral Rule in Shadow Bank Crackdown

- Google Expands U.S. Shopping Service in Challenge to Amazon.com

- BlackRock Confident on 5% Growth Target on Shift From Cash

- EMC Acquiring Cloud Startup Cloudscaling to Boost Storage Sales

- Billionaire Niel’s Iliad Surges After Dropping T-Mobile US Bid

- Scrapped Deals at 6-Yr High as Iliad Walks Away From T-Mobile

- Gazprom 2Q Profit Rises Less Than Forecast; Revenue Increases

- SABMiller Sales Trail Estimates Amid Weaker Volumes in Asia

- Chevron Delays $12b Deep Water Drilling Project: Jakarta Post

- Samsung Electronics to Make Facebook Exclusive Phone: Daily

- Apple Won’t Introduce Retina Macbook Air on Oct. 16: Re/code

- Bumble Bee Said to Attract Bids From Thai Union, Mitsubishi

- CVC Said to Near Accord to Buy Finnish Insulation Maker Paroc

- Oil Demand Growth This Year Seen Weakest Since 2009 by IEA

- German Investor Confidence Falls as Growth Prospects Weaken

AM EARNS:

- Citigroup (C) 8am, $1.12 - Preview

- Domino’s Pizza (DPZ) 7:30am, $0.61

- JB Hunt (JBHT), 8:30am, $0.84 (tentative)

- Johnson & Johnson (JNJ) 7:45am, $1.44 - Preview

- Wells Fargo (WFC) 8am, $1.02 - Preview

- Wolverine World Wide (WWW) 6:30am, $0.59

PM EARNS:

- Bank of the Ozarks (OZRK) 5pm, $0.39

- CSX (CSX) 4:01pm, $0.48

- Intel (INTC) 4:01pm, $0.65 - Preview

- Linear Technology (LLTC) 5:01pm, $0.59

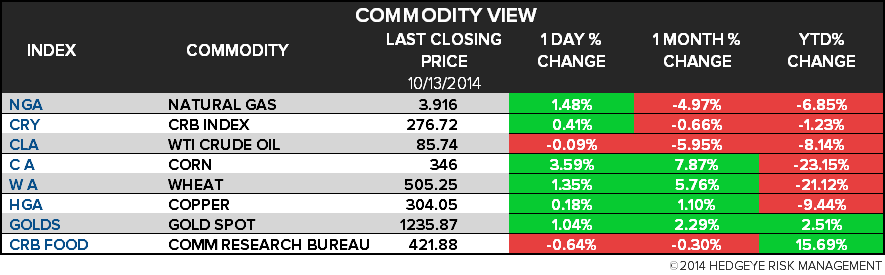

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Extends Drop From 22-Month Low as Demand Slows; Brent Falls

- Oil Demand Growth This Year Seen Weakest Since 2009 (Correct)

- Giant Battery Unit Aims at Wind Storage Holy Grail: Commodities

- Rice Crop Seen Shrinking by FAO on Weather, End of Thai Subsidy

- Tin’s Price Tumble Seen Slashing Shipments From Indonesia by 30%

- Cocoa Rebounds After Drop Yesterday; Arabica Coffee Also Gains

- Gold Trades Near 4-Week High as Investors Weigh Oil to Economy

- Gold Rises Near 4-Week High as Investors Weigh Economy to Oil

- Copper Users in Europe Likely to Seek Lower Premiums: Macquarie

- Rubber Growers Agree to Avoid Selling at Low Prices: IRCo

- Indian Steel Demand Said to Expand at Slowest Pace in Decade

- Rubber Climbs Most Since May After Top Producers Price Pledge

- Thai Gold Exchange May Offer Kilobar Trade Next Year, Jitti Says

- Rebar Falls Most in 2 Weeks as Exports Surge Amid Overcapacity

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

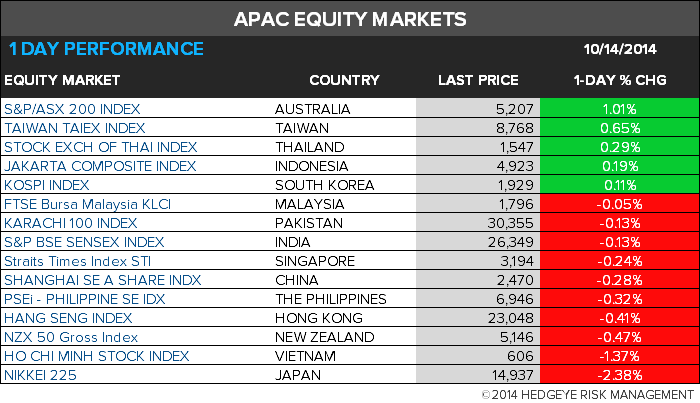

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team