HEDGEYE TV

Quarterly Macro Themes Q&A

Here’s the question and answer portion from Thursday’s Macro Themes call. Hedgeye CEO Keith McCullough answers questions on a host of topics including #Quad4, #Bubbles and more.

One-Minute Video | McCullough: We Haven’t Seen This Bearish Market Signal In Over 18 Months

In this brief excerpt from Thursday's Morning Macro Call, Hedgeye CEO Keith McCullough warns investors that the Russell 2000 and S&P 500 are both bearish trend and tail in our model for the first time in at least 18 months.

ONE-MINUTE VIDEO | McCullough: ‘Quad 4’ Matters A Lot More to Your Portfolio than a 50-Day Moving Monkey

In this brief excerpt from Tuesday's Morning Macro Call, Hedgeye CEO Keith McCullough discusses the recent move into Quad 4 in our proprietary model and why it matters to markets ahead of Hedgeye’s Q4 Macro Themes call this Thursday.

CARTOON

Deflation (Got #Quad4 Yet?)

Our models are forecasting a continued slowing in the pace of domestic economic growth, as well as a further deceleration in inflation here in Q4. The confluence of these two events is likely to perpetuate a rise in volatility across asset classes as broad-based expectations for a robust economic recovery and tighter monetary policy are met with bearish data that is counter to the consensus narrative.

Sweet Success?

Hedgeye reiterates its long bond call (in $TLT terms), and to stay away from small caps.

Tweedledee & Tweedledum

CHART

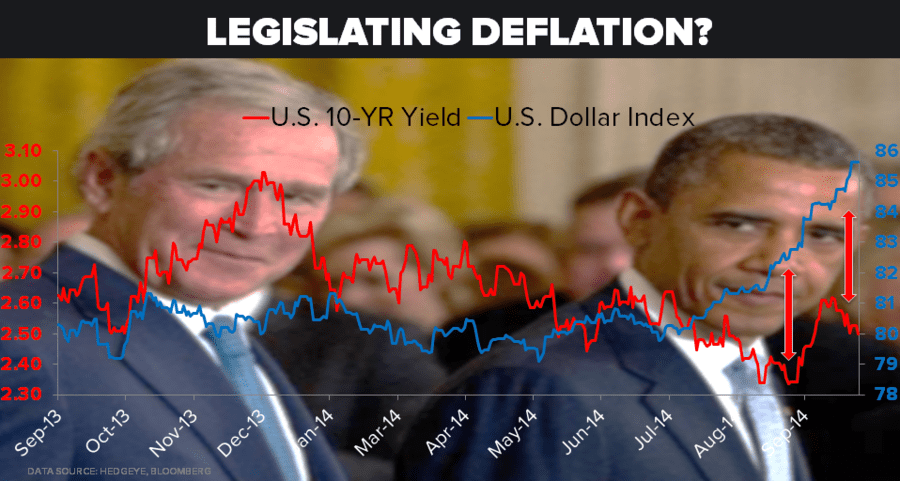

Legislating Deflation? (10YR Yield vs. U.S. Dollar Index)

#Quad4 [U.S. Growth and Inflation (In Rate of Change Terms) Slowing at Same Time]

Need. Moarr. Drugs. $DXY

Mario Draghi’s Drugs proved to be impotent in yesterday’s real-time market voting session. Germany’s DAX closed down -2% on the day. That puts every major European Equity market index in bearish TREND signal mode @Hedgeye.

POLL OF THE DAY

Tech Bubble: Who's Right Peter Thiel or Keith McCullough?

Entrepreneur Peter Thiel made headlines Monday telling Fox Business anchor Deidre Bolton that we are not in a tech bubble. Thiel said, “I’m investing in tech stocks to hide from the government bond bubble.” Hedgeye CEO Keith McCullough replied in a tweet to @peterthiel, “I’m hiding in the Long Bond so that I can be short the Tech Bubble.” So, who's right?