This note was originally published at 8am on September 12, 2014 for Hedgeye subscribers.

“A monster, a hydra-headed monster…”

-Andrew Jackson

That’s what President Andrew Jackson called the Bank of The United States as he took office in 1829 – a “hydra headed monster equipped with horns, hoofs, and a tail so dangerous that it impaired the morals of our people, corrupted our statesmen, and threatened our liberty.” (Hamilton’s Curse, pg 69)

And that’s what I am going to call Ben Bernanke’s legacy as of this morning – the Hydra-Headed Fed. After doing what he allegedly did at a super secret Morgan Stanley lunch yesterday, that is exactly what this man deserves – someone calling him out on a new and tangible market risk that he just created.

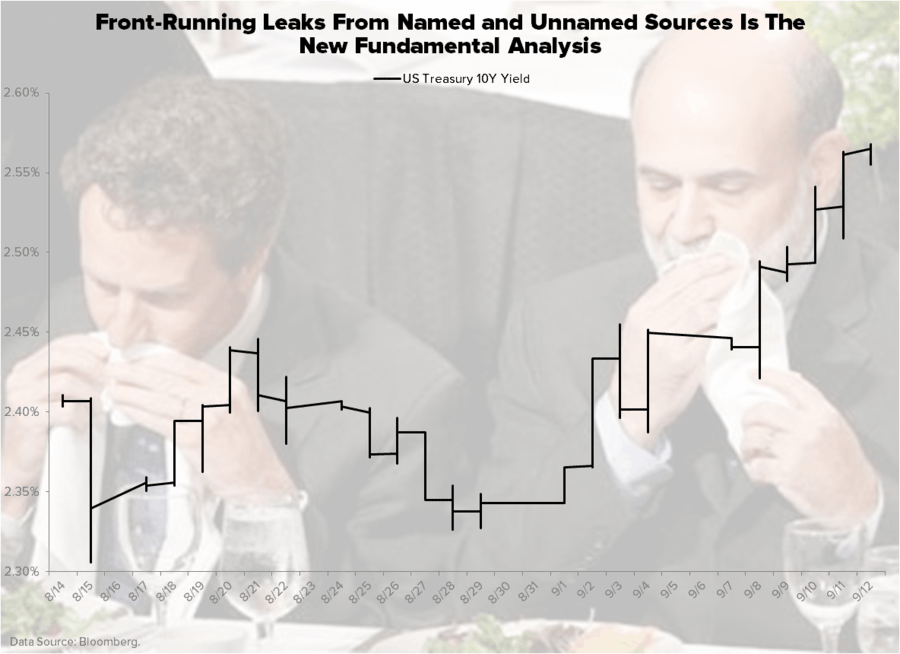

Again, allegedly (because I wasn’t there), Bernanke recklessly told a group of investors that US GDP growth was going to surprise to the upside (i.e. be better than 3% consensus) and that he could not believe the 10yr was still trading under 3%. In Fed whisper speak, that’s code for Janet is going to get more hawkish (look at the intraday chart, post lunch) … but is she?

Back to the Global Macro Grind…

Notwithstanding the fact that Bernanke was getting paid bank to whisper these sweet nothings into the ears of those with a seat at the almighty’s table, is this what the “transparent” and “accountable” Fed wants? Is Bernanke on the same page as Janet? Or, fully loaded with Draghi talking up the drugs in Europe, is this hydra-headed-un-elected beast out of communication control?

If you don’t think this matters, think again. And think of it in risk terms (i.e. what happens if something like the opposite happens at the Fed meeting next week). What happens if and when Janet Yellen says, ‘hey, I want to be “data dependent” and the recent employment and housing data slowed’?

In real-time market risk management terms what Bernanke’s comment does is:

- Widens the immediate-term risk range of the 10yr to 2.33-2.58%

- Ups the probability of accelerating bond market volatility

- Confirms the recent breakout in foreign currency volatility

In other words, the Hydra-Headed Fed is going to perpetuate the one thing Bernanke trumpeted (both in 2007 and now) as his great success – eviscerating market volatilities.

If you don’t follow it as closely as some of us do, the context of this moment in US central planning history is as critical as it gets. You have to go all the way back to when the Jeffersonians crushed Hamiltonian big government guys (200 years ago) to get what I think The People are really going to get right if the Fed, ECB, and BOJ create the next crisis.

They are going to get that these Policies to Inflate didn’t work.

For the economy, that is…

Now if you ask some of the perma bull economists out there how the economy is doing, it’s just peachy. Yesterday, I think Nancy Lazar wrote that US “consumer confidence is breaking out to the upside.” Maybe Wall Street consumer confidence is… but, please, do not confuse that with the real America’s confidence in negative purchasing power and real wage growth.

By the Federal Reserve’s own admission (they published this research last week), 2/3 of Americans never left being in a recession. Median incomes declined -5% for the bottom 60% of Americans over the 2010-2013 period as the cost of living in the US has ripped to all-time highs.

Oh, but gas prices are going to fall (then rise)… right…

Again, this is where the Hydra-headed monster of market expectations really matters – it’s called correlation risk:

- When Fed heads use communication tools to talk up rate hikes (like Bernanke just did) USD and rates rise

- When USD and rates are rising, at the same time, commodities, oil, Gold, etc. go down

- The machines (quants) then chase macro correlations, and macro markets get overbought/oversold

After the biggest weekly rate of change move for the currency market since 1997 (not a good reference date for globally interconnected macro risks!), on a 6 week duration, here’s the macro market’s current correlation to USD:

- Euro vs USD = -0.99

- Silver vs USD = -0.93

- Gold vs USD = -0.90

- Brent Oil vs USD = -0.74

- SPX vs USD = +0.72

That’s why I use the word “recklessly” to describe what Bernanke did yesterday. If Yellen doesn’t talk up the US Dollar and Rates (which Americans should love by the way), the entire macro trade dominating markets right now can easily (and quickly) reverse.

Is this normal? Is this acceptable? Was this the America we all like to think of as “free market capitalism”?

If there ever was a day to be scared of the monster of expectations that both the Fed and Old Wall has created, this is probably it.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.33-2.58%

SPX 1984-1999

RUT 1154-1181

USD 83.66-84.91

EUR/USD 1.28-1.30

WTIC Oil 91.64-95.36

Gold 1234-1281

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer