TODAY’S S&P 500 SET-UP – September 22, 2014

As we look at today's setup for the S&P 500, the range is 19 points or 0.67% downside to 1997 and 0.28% upside to 2016.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.01 from 2.01

- VIX closed at 12.11 1 day percent change of 0.67%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Natl Activity, Aug. est. 0.33 (pr 0.39)

- 9am: ECB’s Draghi speaks in Brussels

- 10am: Existing Home Sales, Aug., est. 5.20m (prior 5.15m)

- 10:05am: Fed’s Dudley speaks in New York

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $23b 6M bills

- 7:30pm: Fed’s Kocherlakota speaks in Marquette, Mich.

GOVERNMENT:

- Senate, House out of session

- 8:15am: FDIC Chairman Martin Gruenberg speaks at American Banker Regulatory Symposium in Arlington, Va.

- 4pm: Treasury Sec. Jack Lew gives speech on economics of climate change at Hamilton Project-hosted event, followed by roundtable discussion with former Treasury Sec. Robert Rubin

- 4:15pm: Comptroller of the Currency Thomas Curry speaks at American Banker Regulatory Symposium in Arlington, Va.

WHAT TO WATCH:

- Siemens buys Dresser-Rand for $7.6b to expand in oil equipment

- Tesco starts probe after overstating profit guidance by ~$408m

- Alibaba’s bankers said to increase shr sale size to record $25b

- Apple iPhone 6 Plus outselling smaller model: Piper survey

- Apple iPhone weekend sales preview

- Deutsche Bank says currency trader dismissed on misreporting

- U.S. Treasury seeking to close tax address loophole, Lew says

- Blackstone halting efforts to find deals in Russia: FT

- Google selects HTC to make 9-inch Nexus tablet: WSJ

- Emirates airline plans U.S. expansion as widebody fleet grows

- Insider buying dries up defying $275b of buybacks

- Clorox said to reject takeover offer with 20% premium: NYPost

- Mitsubishi Corp. offers to buy Norway’s Cermaq for $1.4b

- Total to cut costs, sell assets after lowering output forecast

- SK buys shale gas asset from Continental Resources: MoneyToday

- German union calls strikes at Amazon warehouses: Reuters

- China Finance Chief Lou say eco growth faces downward pressure

- UN’s Ban joins 310,000-strong march for climate action

EARNINGS:

- AutoZone (AZO) 7am, $11.26

- Neogen (NEOG) 8:45am, $0.23

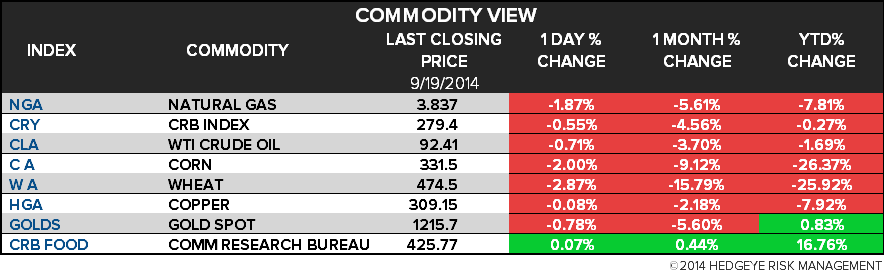

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Leads Industrial Metals Lower on Outlook for Slower China

- Commodities Extend Declines to Five-Year Low in ‘Capitulation’

- Hedge Funds Make Record Bet on Lower U.S. Diesel Prices: Energy

- Gold Is Little Changed Near Eight-Month Low as Silver Declines

- Corn Declines With Soybeans to 2010 Lows on Increasing Supplies

- Brent Crude Declines on Concern China Growth Slowing; WTI Drops

- Indonesian Police Probe Clears 82 Tin Containers for Exports

- Iron Ore Futures Decline Below $80/MT to Record Low in Singapore

- Rubber Production Seen Declining by Consortium of Top Exporters

- Merkel’s Taste for Coal to Upset $130 Billion Green Drive

- Al-Amoudi to Invest $500 Million in Ethiopian Coffee, Oranges

- U.K. Royal Mint Starts Online Trading Site for Gold Coins

- Libya Crude Oil Production at 700k B/D, NOC Spokesman Says

- Gasoline Pump Prices Seen Falling After Slump to 7-Month Low

- Gold Bulls Extend Longest 2014 Exit as Prices Drop: Commodities

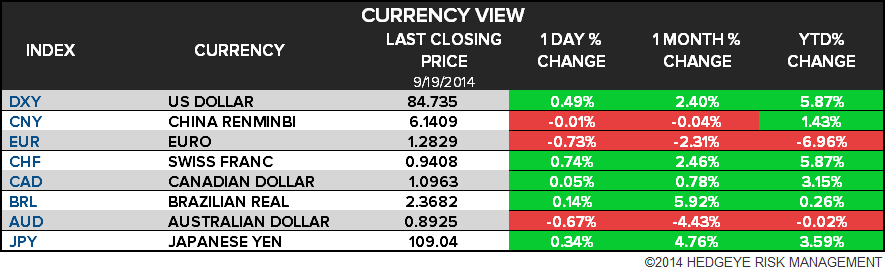

CURRENCIES

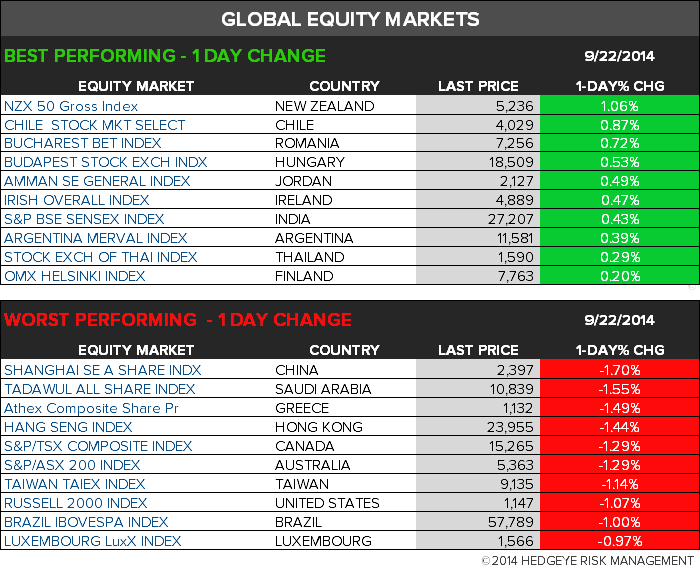

GLOBAL PERFORMANCE

EUROPEAN MARKETS

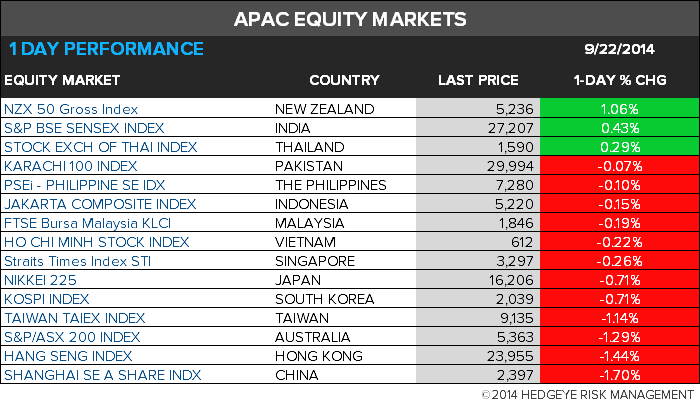

ASIAN MARKETS

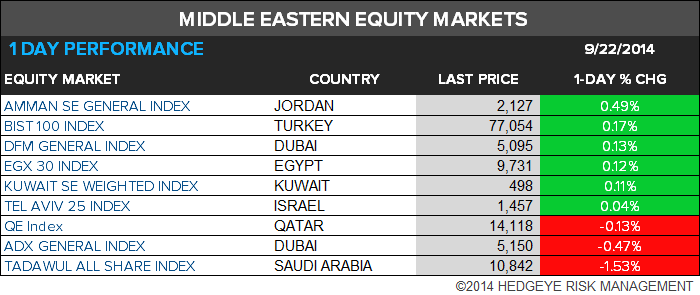

MIDDLE EAST

The Hedgeye Macro Team