Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point.

Today's Focus: September NAHB HMI (Builder Confidence Survey) & MBA Mortgage Applications

September NAHB HMI (Builder Confidence Survey)

This month (September), the NAHB’s HMI, which measures builder confidence, rose to 59, a gain of four points from August’s print of 55 (which was not subject to any revision), marking the highest reading since November 2005 and the third month above the improvement demarcation line of 50 on the Index.

- Sub-Indices: All 3 sub-indices increased MoM for a 4th consecutive month with Current Sales (+5pts) leading the gain alongside a +2pt rise in 6M Expectations and a +5pt rise in Current Traffic.

- Regional: Builder Confidence gained across all regions with the exception of the Midwest which saw a modest sequential decline following the largest MoM increase ever ( +13pts) for the region last month. The 3-month moving average (the NAHB’s preferred, smoothed view) again improved in September across each regional series.

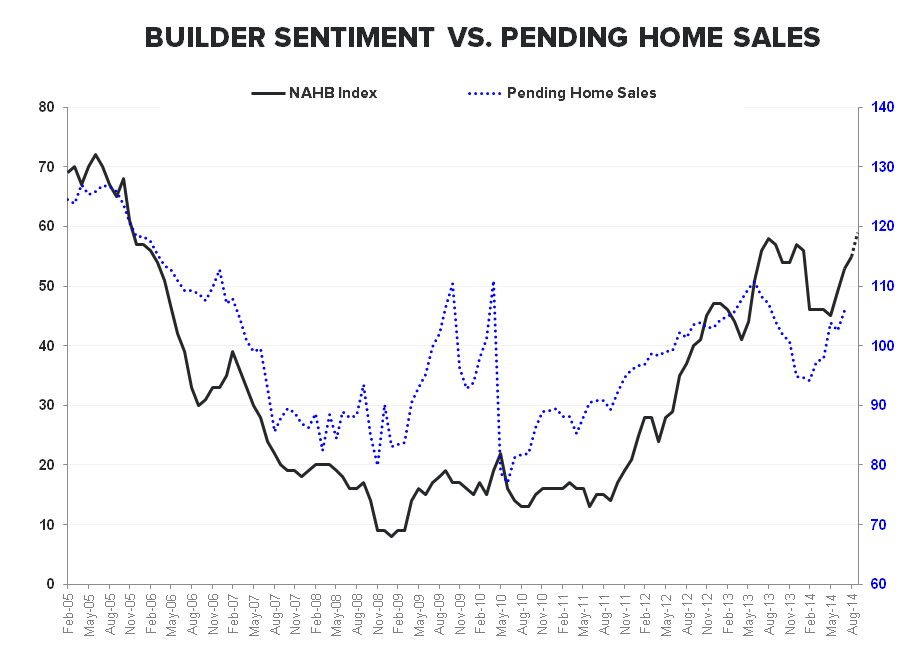

Confidence vs Actual Construction: Builder confidence and Pending Home Sales have shown some reconvergence in recent months while the divergence between builder sentiment and new single family home construction continues to expand.

Earnings reports and management commentary out of the public homebuilders has been mixed with TOL indicating that strong buyer traffic is seeing relatively low conversion to sales. Meanwhile, LEN numbers showed a solid performance on both current sales and forward outlook. The TOL commentary accords, at least in part, with the disconnect observed between builder sentiment and actual new construction activity.

We’ll get the housing starts/permits data for August tomorrow, but with SF starts middling YTD and permits up just +6K in July, the upside for single family construction over the balance of 2H still appears somewhat constrained.

NAHB Chairman Kevin Kelly had this to say on the September reading:

“Since early summer, builders in many markets across the nation have been reporting that buyer interest and traffic have picked up, which is a positive sign that the housing market is moving in the right direction.

NAHB's Chief Economist, David Crowe, added this:

"While a firming job market is helping to unleash pent-up demand for new homes and contributing to a gradual, upward trend in builder confidence, we are still not seeing much activity from first-time home buyers. Other factors impeding the pace of the housing recovery include persistently tight credit conditions for consumers and rising costs for materials, lots and labor."

MBA Mortgage Applications

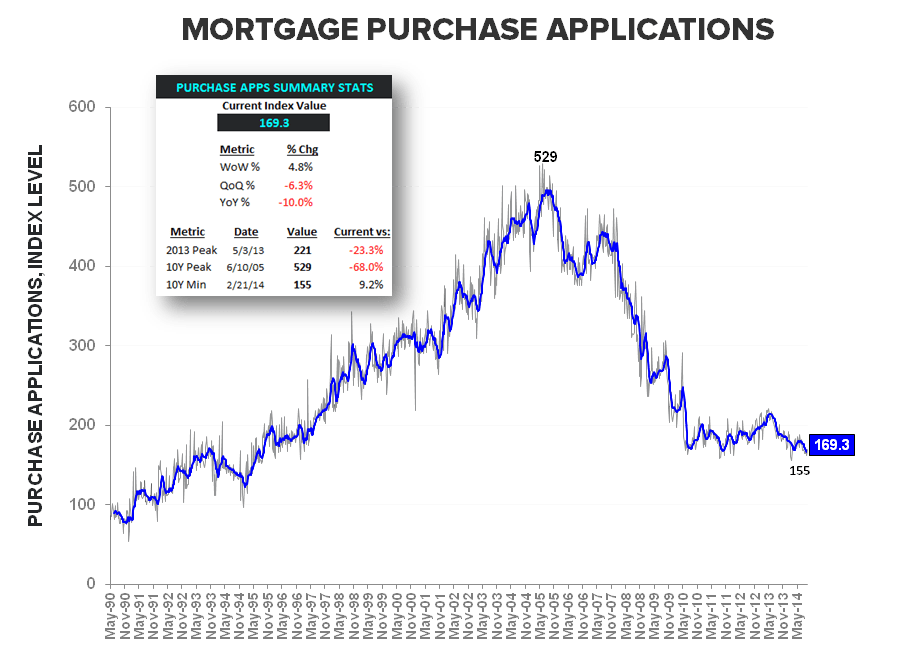

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended September 12th.

- Headline and Purchase Apps re-traced the holiday week decline with the composite index rising +7.8% to 353 from 327 – after falling from 353 to 327 during the week including Labor Day.

- Purchase Application volume rose +4.8% sequentially to 169.3 on the index; the 1st rise in three weeks and the highest level since the first week of July. Purchase activity remains down -10% YoY and is tracking at -6.3% QoQ with the quarterly average holding at the lowest level since 2Q of 1995.

- Refi activity rose +10.3% WoW although the YoY rate of improvement deteriorated to -23% from -17% prior as rates on the 30Y FRM rose a sizeable +9bps WoW to 4.36%

About the NAHB HMI:

The Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The monthly survey has been conducted for 30 years. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. The HMI is a weighted average of separate diffusion indices for these three key single-family series. The HMI can range from 0 to 100, where a value over 50 implies conditions are, on average, improving, a value below 50 implies conditions are worsening, and an index value of 50 indicates that the housing market is neither improving nor worsening.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake