A review of the 1H numbers

CALL TO ACTION

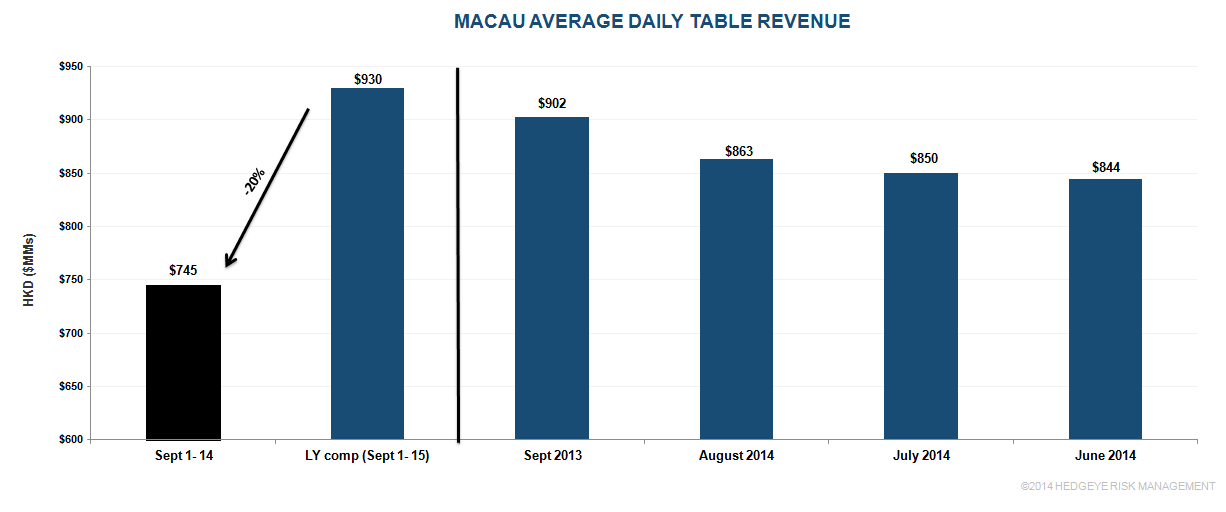

We see no reason to buy any Macau related stocks with the possible exception of Galaxy Entertainment. Even Galaxy looks more suitable as a long hedge, with upcoming higher labor costs this year. For the first 2 weeks of September, average daily table revenues (ADTR) fell 20% from the comparable period in 2013. The weakness resides in both VIP and Mass and while hold percentage was likely low for the casino operators in the aggregate, lower than expected volumes were also to blame. We are currently projecting a YoY full month GGR decline of 14-18%. Q3 2014, Q4 2014, and 2015 estimates look like they need to go lower for most of the Macau operators.

THE MARKET DATA

ADTR of HK$745 million over the first 14 days of September was the lowest since the 1st week of July. Unless there is a miraculous recovery, full month gross gaming revenues (GGR) should fall in the mid to high teens which would represent the largest YoY decline since 1H 2009.

The dismal results look broad based: VIP and Mass volumes were weak and overall hold percentage was likely low. On a YoY basis, we would expect ADTR in 2H of September to look better than 1H. However, play levels are seasonally soft heading into Golden Week so on an absolute basis, 2H may mirror 1H ADTR. The only glimmer of hope is that forward bookings seem to portend a decent Golden Week – only if full rooms convert into strong gaming play levels.

MARKET SHARES

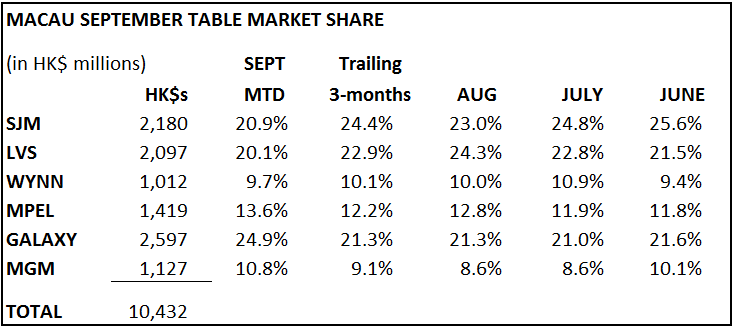

In terms of market share, Galaxy is the standout with MGM and MPEL also producing above trend. LVS is finally holding unlucky and that portfolio of properties dropped well below recent share levels. SJM is also lagging badly.

CONCLUSION

Our negative “Mass Decelerating”call – as first articulated in our 06/13/14 note – remains fully intact. In fact, the slowdown has been steeper than even we expected. We remain negative overall on the Macau stocks and would use Galaxy Entertainment as the long hedge. Estimates need to go lower across the board for Q3 and Q4 and with the possible exception of Galaxy (owing to an earlier opening of Phase 2), 2015 estimates look high. LVS in particular looks ripe for a meaningful earnings downgrade.