We discussed the burgeoning divergence between actual consumption and capacity for consumption yesterday >> FIVE-FECTA: CONSUMER CREDIT GROWTH ACCELERATES (AGAIN) IN JULY

Today’s small business confidence and labor turnover data reflected sequential deceleration in employment, agreeing with the sequential declines reported in the ADP and NFP releases for August.

Meanwhile, measures of labor slack continue to point toward ongoing, albeit slow, tightening in labor market conditions – lending some incremental support to the emergent view of supply-side barriers to hurdling secular stagnation.

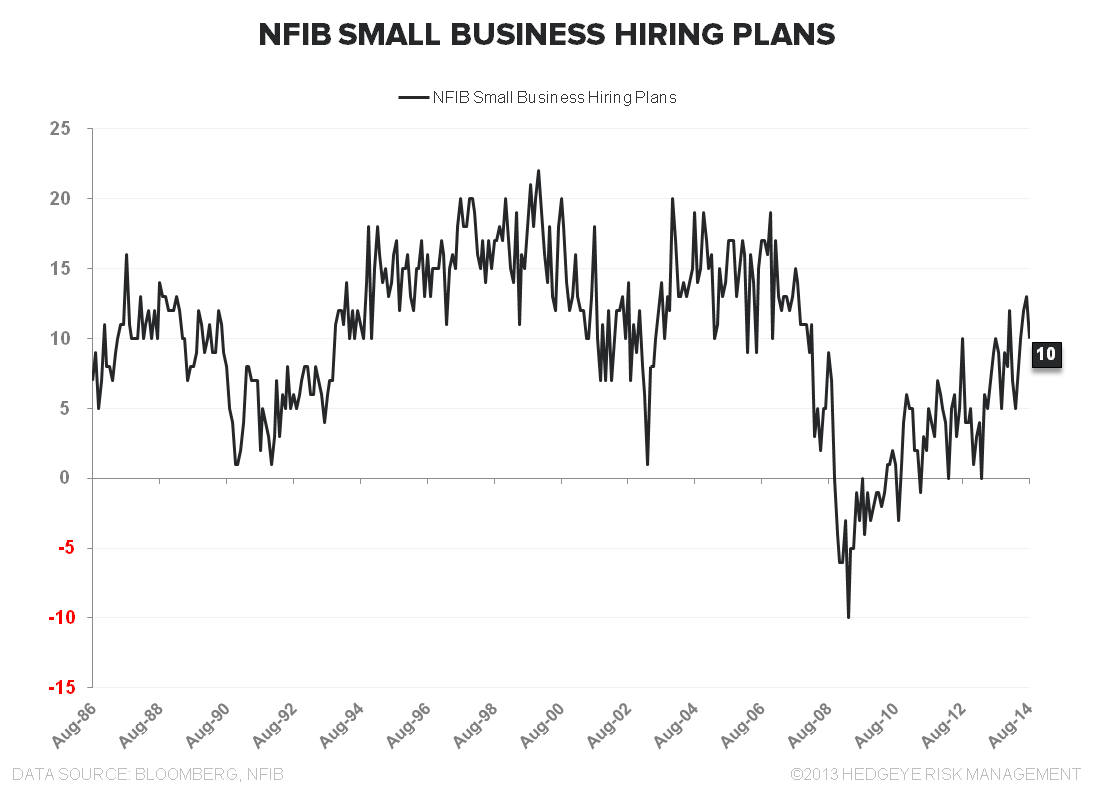

NFIB/Employment: Headline Small Business Confidence increased for a second consecutive month, rising +0.4pts in August. Job Openings and Outlook for General Business Conditions led the upside but Hiring Plans and Sales Expectations dropped -3 and -4 pts, respectively.

Private payroll growth continues to run ~2%+, which matches peak growth in the last cycle and may be as good as it gets given the demographic and labor supply headwinds and the secular slowdown in employment growth over the last 30 years.

(Declining) SLACK: Both the Jobs Hard to Fill and the Compensation Indices rose to new cycle highs in August (NFIB data) while Total Job Openings, Total Hires, and Quits moderated sequentially but held at 13 year highs in July (JOLTS data).

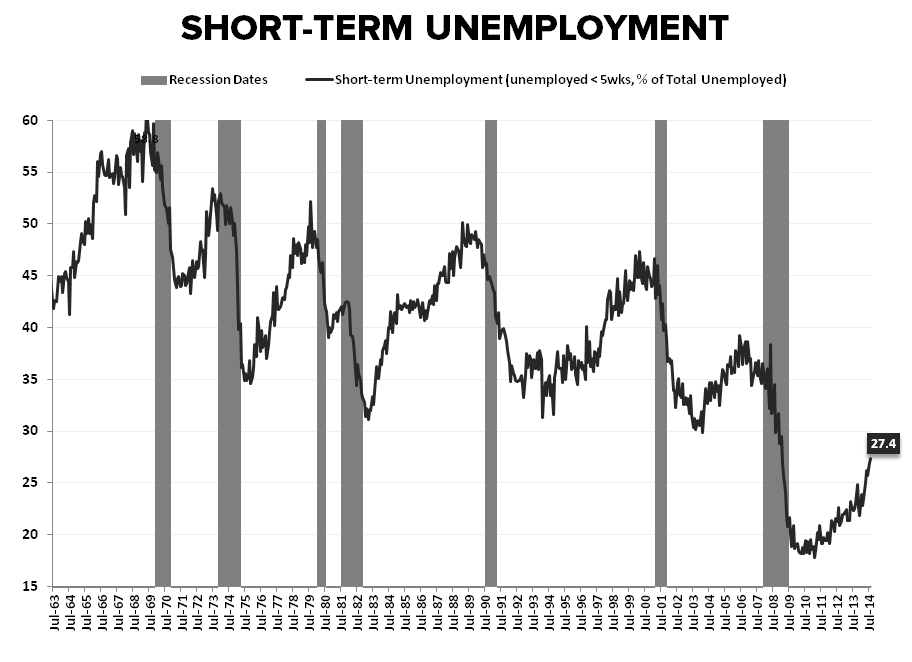

Further, the share of short-term unemployed continued to rise in August while labor supply (total available workers per job opening) remains just north of pre-recession averages.

In short, while signs of moderate sectoral shift and employment hysteresis remain, the labor market remains moderately tighter than the FED officialdom gives lip service to.

Whether the acceleration in hourly earnings for nonsupervisory and production employees to a 4-year high of +2.5% in August is evidence of that tightening being passed through in the form of accelerating wage inflation remains TBD.

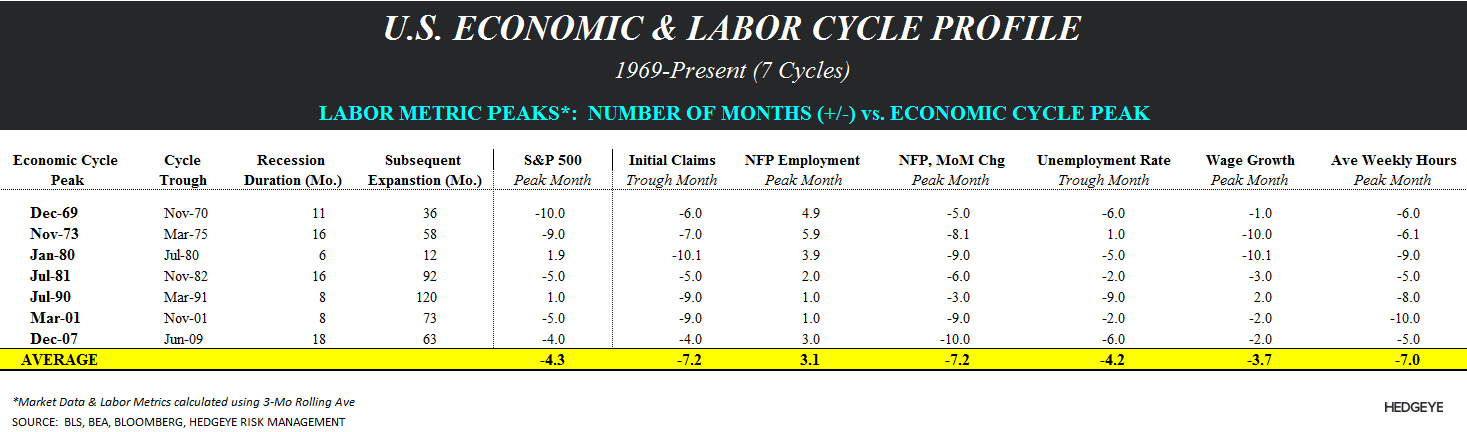

Cycle Accounting: Historically, over the last half century, initial claims and peak monthly NFP gains have led the peak in equities and the peak in the economic cycle by 3 months and 7 months, respectively.

Whether the recent trough in claims in early August or the Apr-June NFP gains represented peak improvement in those measures remains to be seen, but it’s worth monitoring given the fairly consistent temporal sequence in the labor --> equity market --> economy over the last half century.

Christian B. Drake

@HedgeyeUSA