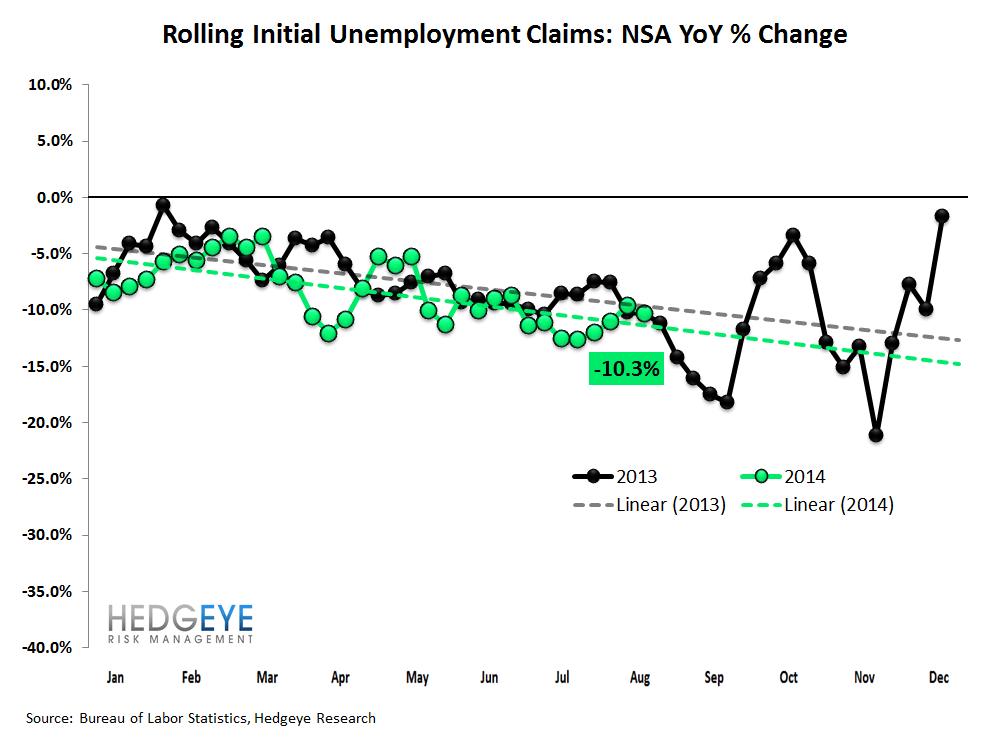

Claims Data Shows Steady Y/Y Improvement

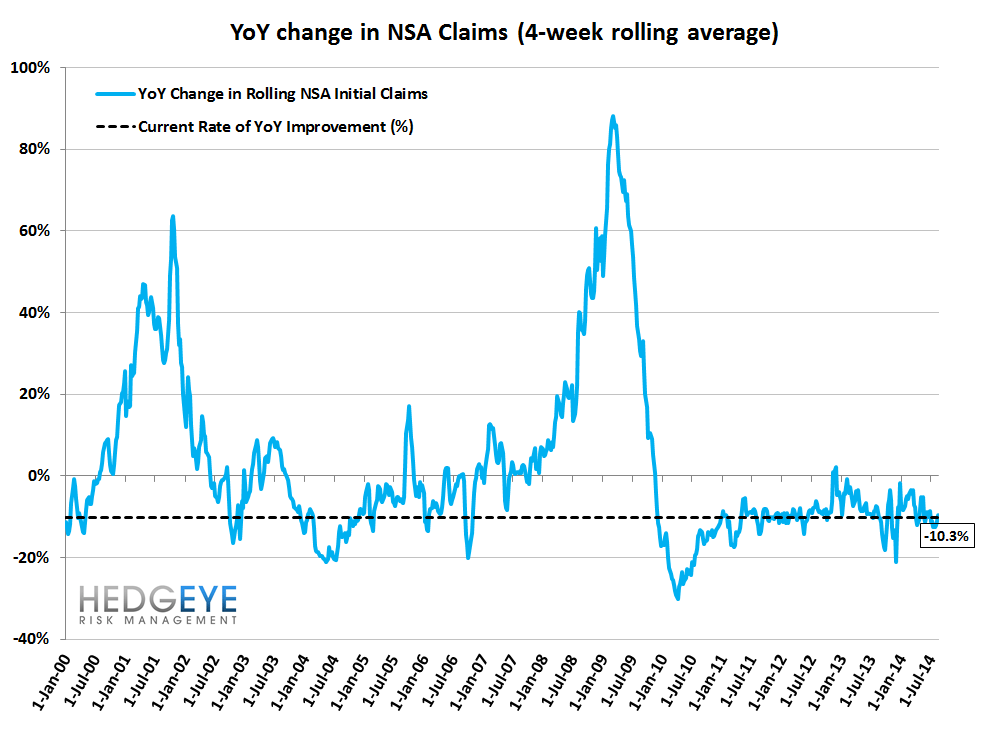

The last couple weeks have seen little change in trend from the initial jobless claims data. Overall, the number of people losing their jobs continues to decline at a rate of roughly 10% year-over-year. this has been the trend now for the last ~14 weeks. This week's print showed a 10.3% y/y improvement, which was slightly better than last week's 9.6% improvement and down a bit from the 11% improvement two weeks ago.

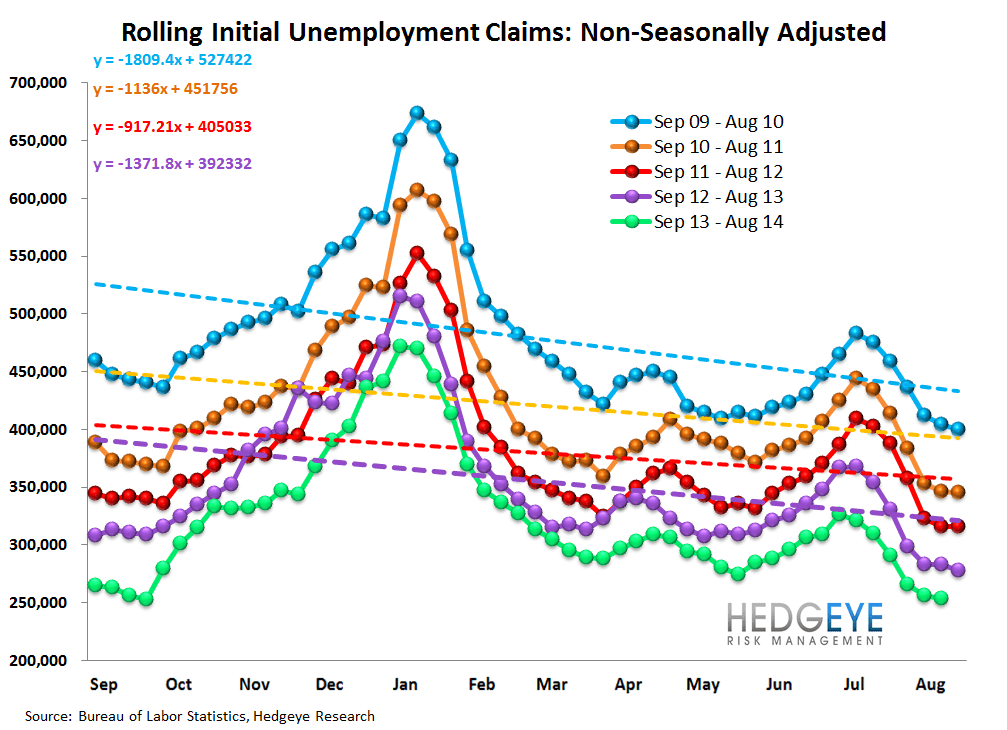

As we've highlighted recently, when initial claims (rolling, SA) have reached the level they're currently at the broader market index (S&P 500) has gone on to advance for another 12-18 months - at least, this has been the case in the last few cycles. As Mark Twain famously said, history never repeats, but it does rhyme.

The Data

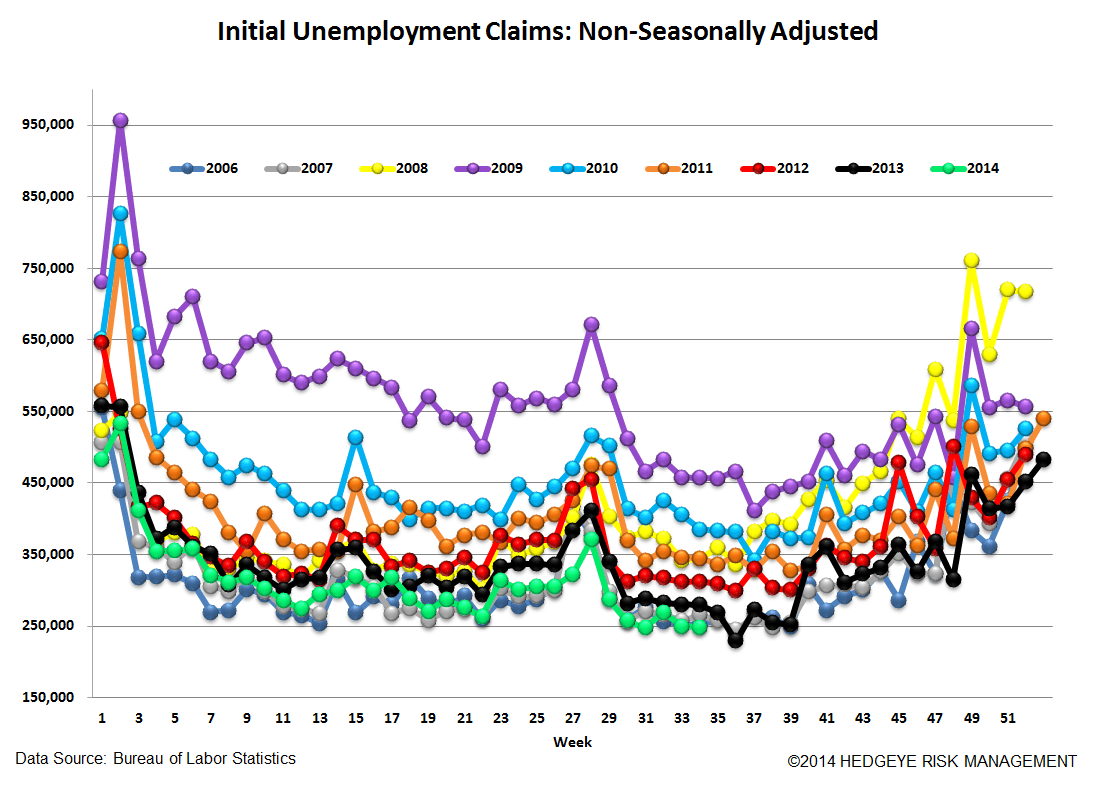

Prior to revision, initial jobless claims fell 0k to 298k from 298k WoW, as the prior week's number was revised up by 1k to 299k.

The headline (unrevised) number shows claims were lower by 1k WoW.

Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -1.25k WoW to 299.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -10.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -9.6%

Yield Spreads

The 2-10 spread fell -11 basis points WoW to 185 bps. 3Q14TD, the 2-10 spread is averaging 201 bps, which is lower by -20 bps relative to 2Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT